Investing in Life Settlements: Greater Returns and Diversification

Rajiv Rebello

Author

February 21, 2022

Author

Summary: Investing in life settlements in place of low-yielding bonds can provide uncorrelated cashflows to help offset equity risk and create better portfolio diversification.

In previous articles we discussed how to use life insurance as a tax-efficient vehicle by which to invest in long-term bonds—with some equity participation via dividends (whole life) or options (indexed universal life)—as well as tax-inefficient investments (private placement life insurance). In this article we discuss why investing in the mortality element of life insurance policies through life settlements can be more attractive than using life insurance merely as a tax-efficient vehicle to invest in long-term bonds. Life settlements offer clients access to cashflows that are uncorrelated to market or interest rate risk with net expected returns in the 8%-11% range. In the wake of low bond yields and rising interest rates, life settlements can help portfolio managers create better risk-adjusted returns for their clients by taking a portion of the assets they would have allocated to bonds in a rising interest rate environment and allocating it to life settlements instead.

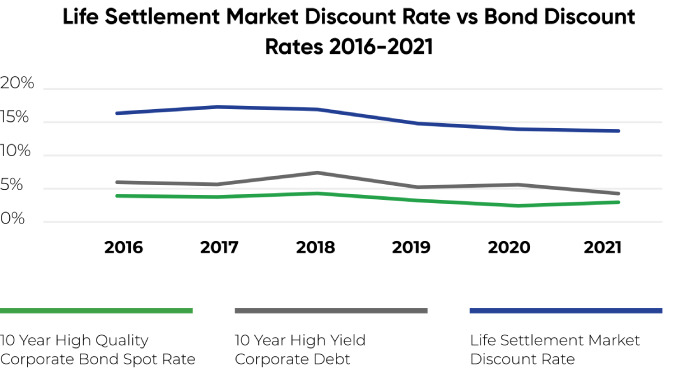

Life Settlements Offer Greater Opportunity for Higher Returns Than High Yield or High Quality Debt

In the current low yield and rising interest rate environment, life settlements can provide higher risk adjusted returns than either high yield or high quality debt.

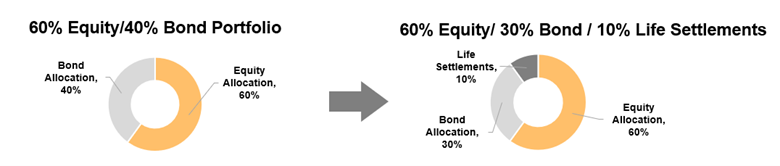

Improving Risk-Adjusted Portfolio Returns by Allocating Portion of Bond Portfolio to Life Settlements

By taking a portion of a client’s portfolio that would otherwise be allocated to bonds and allocating it to life settlements instead, RIAs can achieve higher risk-adjusted returns and better portfolio diversification.

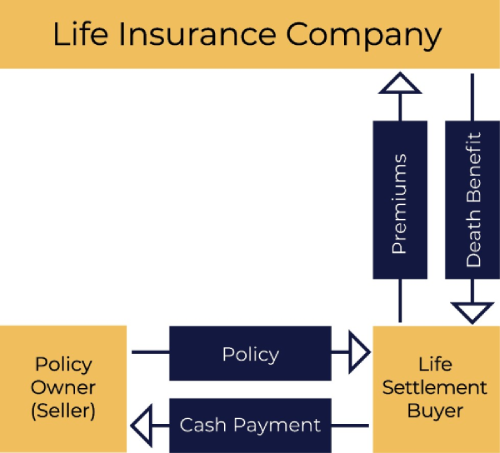

For those unfamiliar with life settlements, a life settlement is the sale of an in-force life insurance policy to a third party for an amount greater than what the insured could receive from simply canceling the policy. In return for providing the seller with a cash payment, the third-party purchaser (investor) owns the life policy, pays all premium payments going forward and eventually receives the entire death benefit at the time of the insured’s death.

A life settlement allows the current policy owner (seller) to exit his investment in an asset that he or she no longer needs or can no longer afford. For the buyer, the investment offers great risk-adjusted returns and cashflows that are not correlated to market or interest rate risk.

Life insurance is a necessary protection vehicle for individuals who have significant liabilities, but limited assets to pay for them. For example, young parents typically have mortgages and debt obligations but limited assets to pay for them in the event that a primary income earner were to pass away unexpectedly. A life insurance policy helps protect the family against this unforeseen event.

As these parents get older, however, their assets increase as they earn more at their jobs and save for retirement. Their liabilities also decrease as the mortgage gets paid down and children grow into adults and become financially independent. Older policy owners no longer need life insurance at that point, but have other life expenses that need to be paid while they’re still alive: healthcare, assisted living, etc.

As insureds get older, the cost of insurance on these policies also gets more expensive and often times seniors on fixed incomes can no longer afford to pay the premiums on these policies. Many life insurance policy owners simply cancel their policy if they no longer need or no longer can afford to pay premiums on the policy. In fact, Society of Actuary lapse studies show that almost 50% of permanent life insurance policies are canceled within the first 10 years. Since permanent life insurance policies often have surrender penalties for canceling that last as long as 20 years, policy owners who cancel their policy early will end up leaving with very little—if anything—of the original investment they made into the policy. Therefore, the ability to treat their insurance policy as an asset and sell it for more than what the policy owner could receive from merely canceling the policy is an incredible benefit for an aging population with increasing costs of living.

An investor in life settlements knows that aging insureds on life insurance policies are more likely to be less healthy now than when the policy was originally purchased. Professional investors and asset managers in life settlements confirm this decrease in health through independent third-party consultants that provide life expectancy reports. Furthermore, life settlement investors know that if they can find specialized actuarial and insurance expertise they can calculate the mortality arbitrage on the policy and determine how to pay significantly less in premiums than the previous policy owner was paying to keep the policy in force. These two factors make the purchase of an individual policy attractive as the life settlement investor typically pays a cash price for the policy at a discount rate (IRR) of 13%-16%.

An investor can expect to achieve two outcomes. The insured could pass away before the life expectancy (in which case the return would be higher than the 13%-16% the policy was priced at) or the insured could pass away after the life expectancy (in which case the return would be lower than the 13%-16% the policy was priced at).

However, the life settlement investor also knows that just buying one policy is extremely risky as the investor doesn’t know exactly when the return on investment will be realized. In order for these priced IRRs to materialize, and for the investment to be less volatile, investors have to acquire a decent number of policies at attractive prices using a combination of sourcing channels and insurance expertise that properly finds policies, evaluates the risk and then manages the risk post-acquisition. Hence, while the underlying return on the asset may be uncorrelated to traditional capital markets, this return is very much correlated to the expertise of the asset manager. Therefore, in order for investors to realize stable, high yielding returns in the space that exceed those of traditional equity/bond portfolios they must find highly specialized asset managers that truly understand the space and work on behalf of the investor.

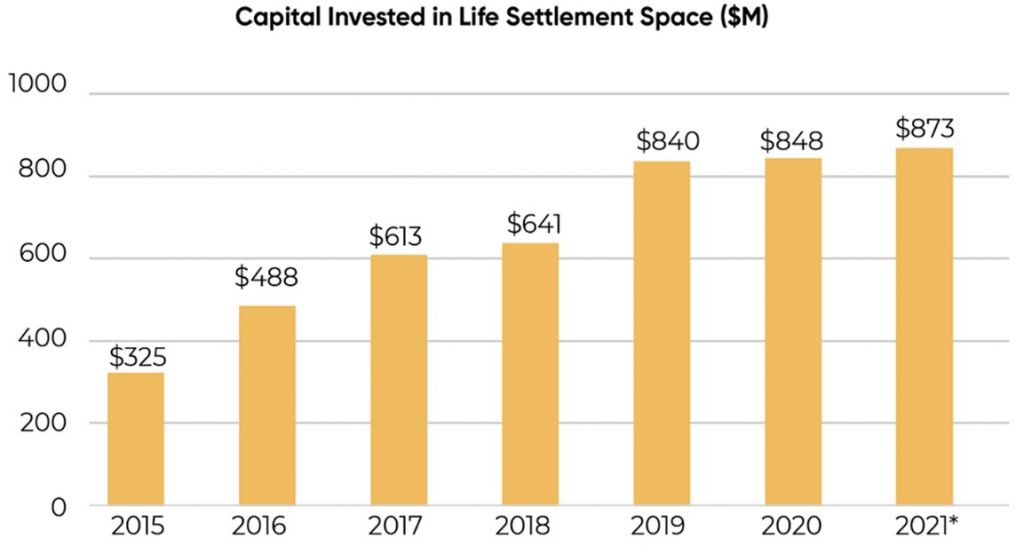

Given the large benefit that life settlements can add in a low-yield/rising interest rate environment it’s no surprise that investment in this asset class has significantly increased over the last few years with large and respected institutional investors like Apollo and BlackRock leading the way.

Over the last several years, large amounts of capital have surged in the secondary life settlement space as institutional investors seek the uncorrelated cashflows that these investments can provide. Even more capital has been deployed in the tertiary life settlement space where existing life settlement investors purchase policies from one another.

*2021 volume is estimated

While life settlements can provide greater risk-adjusted returns, that doesn’t mean that all life settlement funds are equal. As such, investors in life settlements should evaluate funds for the following attributes:

The core determinant of returns in the life settlement space are tied to the actuarial and insurance expertise of the fund manager. Just as you wouldn’t want to invest in a real estate fund with managers that have no direct experience in real estate, you wouldn’t want to invest in a life settlement fund that doesn’t have deep life insurance and actuarial expertise. This type of expertise allows funds to identify undervalued policies in the marketplace, and properly manage mortality, insurance, and tail risk.

Open-ended life settlement funds offer investors a greater ability to exit the investment early and typically come with lower investment minimums. However, in exchange for this liquidity, open-ended funds typically have higher fees, lower returns, and are largely dependent on subjective valuation practices.

Closed-end funds in comparison have significantly higher investment minimums and limited ability to exit the investment early. However, in exchange for this limited liquidity, investors in closed-end life settlement funds receive more investor friendly fee structures and transparency in the return profile.

To learn more about the pros and cons of investing in open-ended life settlement funds versus closed-end life settlement funds, read our article here: The Problem with Investing in Open-Ended Life Settlement Funds

Life Settlement funds are inherently tax-inefficient. That’s because the majority of the gains are taxed at ordinary income rates for investors—similar to how coupon rates from bonds are taxed. Due to the inherent tax-inefficiency of the asset class, it’s important that funds consider this in both the structuring of the fund as well as in the purchasing of policies within the fund in order to make the investment as tax-efficient as possible.

Only about 8% of the policies that would qualify for a life settlement transaction are actually sold in the life settlement market place. The main reason the other 92% are not sold is simply because those policy owners do not know that selling their policy on the life settlement is an option. Furthermore, the 8% of policies that are sold in the life settlement market are often sold through broker channels which can eat up 15% to 30% of the total offer for the policy.

By focusing on developing proper education and sourcing channels, life settlement fund managers can develop their own proprietary channels that will both increase supply and reduce transaction costs which will result in higher returns for their life settlement funds.

Author

Learn how to evaluate PPLI carriers by balancing financial strength ratings against investment platform flexibility. Compare fee structures and long-term costs to select the optimal Private Placement Life Insurance carrier for your wealth strategy.

Determining the right death benefit level for your Private Placement Life Insurance (PPLI) policy is one of the most critical decisions that will impact your policy’s performance, costs, and overall effectiveness. This comprehensive guide explores how to balance regulatory requirements, estate planning needs, family protection goals, and investment capacity optimization to find the optimal death benefit level for your unique circumstances.

Master essential best practices for PPLI investment committee governance. Learn to establish effective oversight structures, develop robust policies, and implement risk management frameworks that maximize wealth preservation while ensuring regulatory compliance.

0 Comments