Investing in Tax-Free Bonds with Whole Life Insurance

Rajiv Rebello

Author

February 18, 2022

Author

For clients in high tax brackets, direct investment into taxable bonds are often not a sufficient diversification tool to offset against equity risk due to the low yields, high taxation, and sensitivity to loss in a rising interest rate environment. As of 4/17/2023, the yield to maturity on AGG is currently at 4.40%. For HNW clients in the top ordinary income tax-bracket that pay as much as 50% of their bond gains in state and federal taxes, that’s only 2.2% on an after-tax basis–and that’s before accounting for inflation. This after-tax return is reduced even further if these clients are paying an advisor to manage their money.

With such a low after-tax, after-inflation return, how can clients benefit from the safety of bond investments? If clients seek additional yield in investing in longer-term bonds as opposed to the intermediate AGG, then they put themselves at more risk of heavy losses in the future if interest rates rise. In a low-interest rate environment, bonds of all durations—but especially long-term bonds—are increasingly sensitive to interest rate changes. Trying to liquidate bond investments after an interest rate increase to buy higher yielding bonds can take years, or decades to recoup the upfront loss.

Figure 1: Loss in Price of Bonds After a 1% Increase in Rates

| Bond Term (Years) | Immediate Loss of Market Value of Bond Prices on 1% Increase in Rates from 2% to 3% | Years of investing at higher coupon rate (3%) to recoup initial upfront loss in value | Years of investing at higher coupon rate (3%) to get back to original 2% yield |

|---|---|---|---|

| 10 | -8.53% | 4 | 10 |

| 20 | -14.88% | 6 | 17 |

| 30 | -19.60% | 8 | 23 |

In a low-yield environment, bond prices are increasingly sensitive to an increase in the interest rate. Longer term bonds are more sensitive than shorter term bonds. If a client is currently invested in 2% yielding bonds and rates increase by 1%, it could take years to recoup the initial upfront loss and over a decade to get back to the original yield they were expecting to earn before the increase in interest rates.

Whole life insurance is a form of permanent insurance that combines long-term bond investing without interest rate risk and with equity dividend participation. When clients pay premiums into a whole life insurance policy, the life insurance company subtracts insurance expenses from the premium amount and then invests the rest into the insurance company’s general account portfolio which are primarily investment grade long-term bonds. At the end of the year the insurance company then credits the client’s cash value account with the interest earned on the client’s net premium. If interest rates rise over the course of the year causing a loss on the market value of the bonds in the general account portfolio, the insurance company does not pass this loss on to the client. This is of significant advantage to the client over investing in these same long-term bonds directly. Furthermore, in the later years of the investment the insurance company shares its profits with the clients through crediting dividends to the client’s investment account.

Investing in long-term bonds through whole life insurance can provide numerous advantages to RIAs and their clients:

The main reason financial professionals don’t increase allocation away from short-term bonds and towards long-term bonds in order to increase the return on their portfolio is their fear of losses if interest rates rise. Whole life insurance allows them to invest in long-term bonds to increase portfolio returns without taking on interest rate risk.

While bonds have been utilized to create better risk-adjusted portfolios and offset equity risk, bond yields are subject to significantly higher ordinary income tax-rates in comparison to equity gains which are taxed at lower capital gains rates. Furthermore, while taxes on equity gains can be deferred until the assets are sold, bond holders must pay taxes on their coupon gains every year. This yearly tax drag on bond yields make bonds significantly less tax-efficient than investing in equity markets—particularly in a low yield environment. The high taxation on bond yields reduces the portfolio diversification benefits of investing in bonds to begin with. Investing in long-term bonds through whole life insurance allows the yearly coupon payments to escape taxation which makes the investment in long-term bonds a better portfolio diversification tool than investing in the same bonds in a taxable account.

When equity markets crash, clients’ investment in bond markets constitute a larger percentage of the overall portfolio due to the now lower valuation of the equity portfolio. In order to keep the percentage of the portfolio invested in equity markets the same as before the crash, financial advisors will typically sell a portion of the bond portfolio and buy equity assets at these lower valuations. This rebalancing exposes clients to additional taxation if the market value of the bonds have increased since they were originally acquired (i.e. if interest rates have decreased). If the opposite is true and interest rates have increased since the bonds were purchased (thereby causing a loss on the market value of the bonds), then clients will have to sell the bonds at a loss as was shown in Figure 1 above.

Whole life insurance allows clients the ability to take a tax-free loan backed by the collateral value of the bonds backing the policy without having to sell the assets at a loss or pay taxes on the gains. What’s equally valuable is that the collateral value of the bonds backing the policy is not subject to interest rate risk. So in a rising interest rate environment, the client’s ability to take out loans is not affected. This ability to pull both principal and gains out without taxation or absorbing a loss due to interest rate risk provides a significant value add over having to rebalance the portfolio exclusively through a taxable account. While taking a loan from the whole life policy will lower future returns of the policy, this will be notably less than having to paying taxes on the gains or taking an upfront loss on the sale of lower yielding bonds.

As with any strategy that involves higher expected returns, there are a number of risks that need to be mitigated in order to realize those higher returns otherwise the client will have been better off investing in bonds directly:

Due to the commissionable expenses, the early year returns in a whole life policy are poor. If the client exits too early via complete surrender or through a withdrawal/loan, the high early year expenses will eat into any tax-advantages they otherwise would have benefitted from

Unlike traditional bond investments in which you can purchase a bond investment on day one and not have to make ongoing capital commitments without repercussions, utilizing whole life insurance requires clients to allocate capital to the structure on a yearly basis for at least ten years. Failure to do this will significantly lower returns.

In the context of investing, whole life insurance should be looked at similar to a retirement plan. In other words, if clients don’t actively contribute to their retirement plan they’re not going to gain the tax-benefits of the plan and won’t have nearly as much when they retire as they thought when they originally signed up for the plan. What’s worse, if clients don’t actively invest in the plan on a yearly basis, then they could lose their entire investment completely. But for those who understand the risks, and are committed to a long-term investment plan, whole life insurance—when constructed properly—can provide significant after-tax benefits in relation to investing in either short-term or long-term bonds directly.

One of the most common mistakes clients make when purchasing whole life insurance is that they try to use it for both life insurance and investment. Doing this minimizes the value of either benefit. Term insurance will always provide more insurance death benefit for the cost than whole life insurance. If the goal is death benefit protection, term insurance should be used. Whole life insurance should be used for its tax-advantaged investment benefits.

In order to maximize the investment component of whole life insurance, clients need to minimize the commissionable part of the product. This means minimizing the death benefit portion of whole life. As we discussed in a previous article, life insurance agents typically receive 100% of the first-year premium paid into a permanent life insurance product. Life insurance companies need to recoup this expense somehow. This means that the cash value growth on parts of the product that are highly commissionable are limited.

In order to allow better cash value growth, many life insurance companies allow for clients to grow their cash value through additional contributions to the policy known as paid-up additions. These paid-up additions have significantly less commission associated with it (typically 3%-7%) so the cash value growth per dollar invested is significantly higher. So investors looking to maximize after-tax cash value growth need to focus on minimizing the investment paid into the base whole life insurance policy and maximizing the investment paid into the paid-up additions portion of the policy. This means focusing on reducing the death benefit acquired for a given dollar of premium.

Reducing the death benefit of the whole life policy for a given amount of premium allows for significantly more cash value growth in comparison to maximally funding the base policy or putting the same amount of money into a taxable long-term bond strategy.

| Strategy | DB Acquired | First Year Commission | 10 Year After-Tax Return | 20 Year After-Tax Return | 30 Year After-Tax Return |

|---|---|---|---|---|---|

| Short-Term Bond Investment | $0 | $0 | 1.08% | 1.08% | 1.08% |

| Long-Term Bond Investment | $0 | $0 | 1.78% | 1.78% | 1.78% |

| Maximize DB WL Plan | $692,425 | $15,995 | -1.94% | 2.62% | 3.46% |

| Minimize DB WL Plan with PUAs | $250,000 | $3,616 | 3.00% | 4.30% | 4.52% |

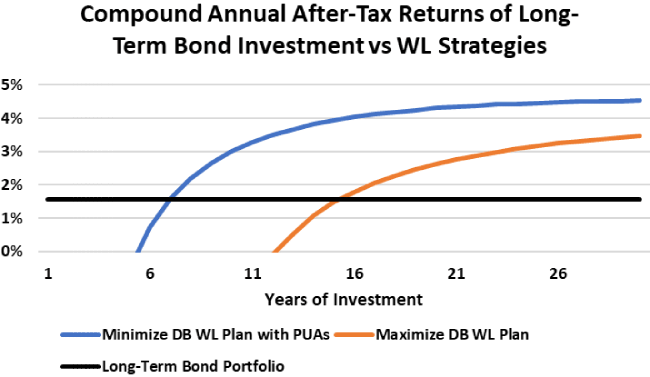

The above table compares the after-tax returns at the end of 10, 20, and 30 years of four bond investment strategies in which the client invests $15,995 every year into each of the strategies. As the table demonstrates, the whole life strategy that minimizes the death benefit and maximizes the PUAs maximizes the after-tax return at the end of each of these time periods.

Assumptions:

As the table above shows, minimizing the death benefit of whole life insurance for a given amount of premium by using PUAs provides a greater after-tax return than any of the other strategies. However, the table above also shows that the investment strategy that uses whole life but maximizes the death benefit for a given amount of premium has the worst after-tax return after ten years of any of the four strategies. This is why it’s important to structure whole life in order to minimize the commissionable death benefit expenses.

The reason for the large disparity in after-tax returns of the two whole life strategies is that the whole life strategy that minimizes the death benefit by using PUAs has significantly higher cash value growth which contributes to higher return profile in comparison to the whole life strategy that looks to maximize the death benefit through the base policy. However, since the early year expenses of both whole life strategies are high, it takes a number of years for both of these strategies to beat the after-tax bond strategy as evidenced by the graph below.

Whole life insurance can provide greater after-tax long-term bond returns than investing directly in long-term bonds. However, since early year expenses in the whole life policy are high, clients who use the whole life strategy need to commit to the strategy for a number of years in order to beat investing in long-term bonds directly. Clients using WL also need to focus on minimizing the death benefit in the policy and maximizing the PUAs. Since the PUA WL strategy has better cash value growth than the Maximize DB WL strategy, it only takes 7 years for the compound annual return of the PUA strategy to outperform the long-term bond strategy whereas the breakeven point for the Maximize DB WL strategy is 16 years.

Note that prior to the breakeven point for both WL strategies, the return is often negative due to the high early year expenses. This is why those investing in bonds through a WL strategy need to invest for the long-term.

The graph above shows the key components of investing in a whole life investment strategy versus a taxable long-term bond strategy:

In order to compensate for paying the agent 100% of the first year premium, the insurance company needs to recoup this by limiting the cash value growth in the early years of the product. This way if the policy owner cancels the policy in the early years then they insurance company gets to keep the difference in interest they earned from the underlying bond portfolio versus what they credited the policy owner. Keep in mind that nearly 50% of whole life insurance policy owners will cancel the policy in the first ten years which allows for the life insurance company to recoup the initial expenses they spent in paying the agent in the first year.

One of the reasons that whole life insurance returns are so great in the later years of the policy is because the life insurance company starts to issue dividends to the policyowner based on the profitability of the whole life product. The life insurance company makes profits through two key ways:

As the above graph shows, the WL strategy that maximizes PUAs and minimizes the base death benefit of the policy provides significantly higher returns and a shorter break-even period than the WL strategy that just maximizes the base death benefit of the policy.

While the early years of the whole life product are a loss for the insurance company (mainly because of the large expenses paid in the first year to the agent to sell the policy), over time the life insurance company makes profits from both the interest rate spread and the mortality spread. In the later years of the policy the life insurance company starts to share this profitability with the policyowners who have kept the policy by issuing dividends. These dividends start to become material around years 7-10 and increase every year after that. In fact, in years 11-20 clients in a whole life policy are typically earning 4.7%-4.9% year after year tax-free on their investment due to these large dividend payments. However, since less than 50% of policyowners will have kept the policy by then, for the life insurance company it’s not much of a loss for the insurance company to share profitability with the ones that remain at that time.

One of the key benefits of whole life insurance is that policyowners can borrow against the cash value through a tax-free loan. For high net worth individuals in high marginal tax-brackets, borrowing against their cash value is a significantly better option than liquidating their taxable bond investments and paying taxes on the gains. So if equity markets crash, clients can take a tax-free loan against the cash value of their policies and use that to buy equities that are now at reduced prices. Also if interest rates go up, clients can take money out of their WL policy to invest in higher earning strategies without having to take a loss on their investment as they would if they were investing directly in bonds.

It’s worth noting here that significant cash value doesn’t build up until the later years of the policy when this ability to take money out becomes viable. In the early years, clients will have to use their existing taxable or qualified accounts to rebalance their portfolios. Also while clients can take out ~80% of their principal and gains via tax-free loans and withdrawals, doing so will hurt their future returns. The reason for this is that taking money out of the whole life policy essentially restarts the “low return” part of the investment profile and the client will have to wait 7-10 years to get back to the “high return” part of the investment profile.

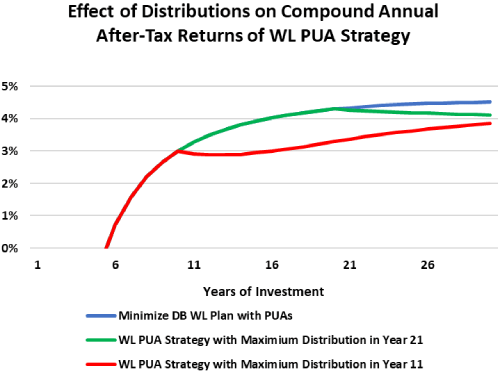

Whole life insurance allows clients to take up to 80% of the principal and gains from the policy out tax-free. However, doing so hurts future returns in the policy as it essentially restarts the “low return” part of the investment profile. In order to minimize the drag on future returns, clients should wait to take distributions until after 15-20 years.

The above table shows the effect of taking distributions in year 11 versus year 21 in comparison to the PUA strategy without distributions.

For HNW clients who are limited to contributing to tax-free accounts like Roth IRAs that also provide tax-free growth, WL insurance can provide a great way to improve the after-tax returns of the bond portion of the client’s portfolio without interest rate risk and with none of the insurance/COI risk that is prominent in universal life policies. As long as clients are committed to contributing the annual premium to the whole life insurance policy and keeping it for the long-term, clients can achieve significantly higher returns by investing in long-term bonds through a whole life policy than through investing in short-term or long-term bonds directly via a taxable account.

Author

Discover how Private Placement Life Insurance transforms charitable remainder trust strategies into powerful wealth replacement tools. Learn tax-efficient approaches that maximize charitable benefits while preserving family wealth for high-net-worth families.

This blog post explores essential PPLI due diligence steps, covering carrier evaluation, regulatory considerations, investment platforms, tax compliance, and advisor expertise to help high-net-worth individuals make informed decisions before implementing this specialized insurance solution.

Discover how PPLI enhances business succession planning through key person insurance and buy-sell funding. Learn private placement life insurance strategies for business owners.

0 Comments