Colva Resources

Articles/Press

ALM | Think Advisor Blog

How to Craft ‘Super Roths’ for Wealthy Clients

VettaFi Advisor Perspectives Blog

The Problem with Open-Ended Life-Settlement Funds

VettaFi Advisor Perspectives Blog

No-Commission Annuities as a Substitute for Low-Yielding, Investment -Grade Bonds

Kitces Nerd’s Eye View Blog

Universal Life Funding Strategies: Optimizing Death Benefit vs Cash Surrender

Value IRRs

Brochures

Media Kit: Colva Actuarial Services

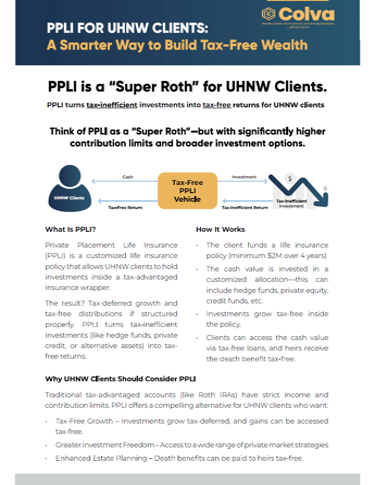

PPLI for UHNW Clients

PPLI for RIAs

PPLI for Estate Attorneys

Whitepapers

Whitepapers

The Power of Guaranteed Income

Why replacing bonds with guaranteed lifetime income annuities can transform your retirement plan

Whitepapers

Increasing After-Tax, After-Advisory Fee Retirement Income for UHNW Clients

The private placement life insurance solution many fee-only RIAs and family offices are missing

Whitepapers

Investing in Long-Term Bonds without Interest Rate Risk

The No-Commission Annuity Solution for Improving After-Tax, After-Advisory Fee Bond Returns

Whitepapers

Investing In Life Settlements

Specialized Expertise to Provide Investors Access to Exclusive Uncorrelated Returns

Videos

Plan for Retirement – Increase risk adjusted portfolio returns and minimize taxes

Implementing Better Retirement Strategies

Do I Need a Financial Advisor?

Frequently Asked Questions

How can Colva help RIAs?

Colva helps RIAs offer their clients fiduciary life insurance, annuity, and alternative investment solutions using our specialized actuarial and insurance expertise to identify the best solutions for the clients.

Furthermore, a lot of our solutions are no-commission solutions. This means that instead of clients taking money away from the RIA to invest in these solutions, our no-commission solutions allow the RIA to get the same fee on the assets in our solutions as they would if they were managing the client’s assets outside the solution in a taxable account. So with our solutions the client ends up receiving a better after-tax solution, and the RIA receives the same fee they were otherwise receiving. It’s a win-win for both parties.

Why should RIAs start implementing no-commission solutions?

No-commission solutions are better for the client because they have limited expenses in comparison to their high-commission counterparts. In an age of fee-compression, if RIAs aren’t offering the best solutions to their clients these clients will take their business and assets under management elsewhere.

Furthermore, RIAs can charge the same fee on the no-commission solutions as they can if the client kept their money in a taxable account. The difference is that the client gets a better after-tax solution.

How can no-commission solutions help attract high net worth clients and generate revenue for my RIA?

High net-worth clients are subject to high ordinary income taxes on the gains in their bond portfolio. By structuring solutions that either defer these gains—or make them tax-free—RIAs can create financial planning strategies geared to attracting their most desired clients.

Standard industry practice is to refer my client to three outside parties for their life insurance and annuity needs. Why is this bad?

While providing 3 different names might remove liability for the RIA, is this really in the best interest of the client? Will these outside parties take a fiduciary interest and try to maximize the value the client is receiving or will they try and maximize their commission? By taking an advisory position over the process—like the RIA does with the client’s other investments—the RIA can ensure that the client is getting the best deal possible. Furthermore, if clients utilize high-commission solutions the client is essentially taking money that could be better invested with the RIA (and earn the RIA revenue) and investing it in a worse solution in which the RIA does not receive compensation.

What are the most obvious or common misconceptions and objections that RIAs think of when it comes to talking about life insurance, annuity, or alternative investment solutions?

Fiduciary fee-only RIAs have a negative stigma—and rightfully so—when it comes to life insurance and annuity solutions for their clients. The reason for this is that so many products in the past were high-commission/high-expense products that ended up really hurting the client. Most fiduciary financial advisors have had to get a client out of a bad annuity and insurance solution at some point in their career. Due to these bad-experiences, most fiduciary fee-only advisors stay away from incorporating life insurance and annuity solutions into their financial practice.

But this is a mistake that hurts clients simply because if their fiduciary fee-only financial advisor isn’t providing fiduciary life insurance and annuity solutions to their clients, these clients will continue to seek out poor products from non-fiduciary life insurance agents.

By incorporating no-commission life insurance and annuity products into their financial practices, fee-only advisors can actually provide clients with higher after-tax returns than if they were to merely invest client assets in taxable accounts.

What is a current financial planning problem RIAs might be facing that no-commission solutions might be able to help them with?

How are you handling bond allocations for high-net worth clients near retirement that are subject to high ordinary income taxation on these bond gains (as well as interest rate risk and sequence of return risk)?

For such clients, tax-deferral and tax-free solutions can be essential. No-commission life insurance and annuity solutions can address this.

Why should RIAs use Colva and not one of its competitors?

There are only a few firms in the space that offer no-commission solutions. The ones that currently do, only offer a handful of carriers. With Colva’s partnership with The BluePrint Insurance Services, we have access to 94% of the carriers in the market, so we can structure solutions that best meet the clients needs—instead of being limited to only a handful of carriers.

Furthermore, as an actuarial servicing company we have the ability to show RIAs how to properly minimize premiums and costs. We can also model different client portfolios to show them how our portfolio solutions better protect their downside—or increase their upside—and allow them to grow their wealth on an after-tax basis.