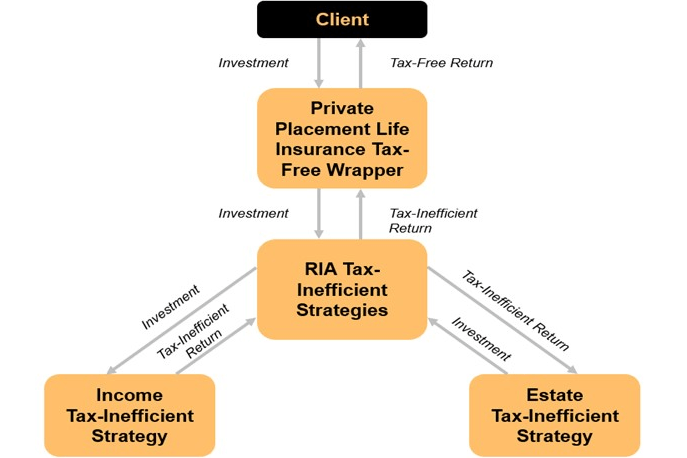

RIAs can utilize PPLI to shelter otherwise tax-inefficient assets from income and estate taxation.

RIAs can utilize PPLI to shelter otherwise tax-inefficient assets from income and estate taxation.

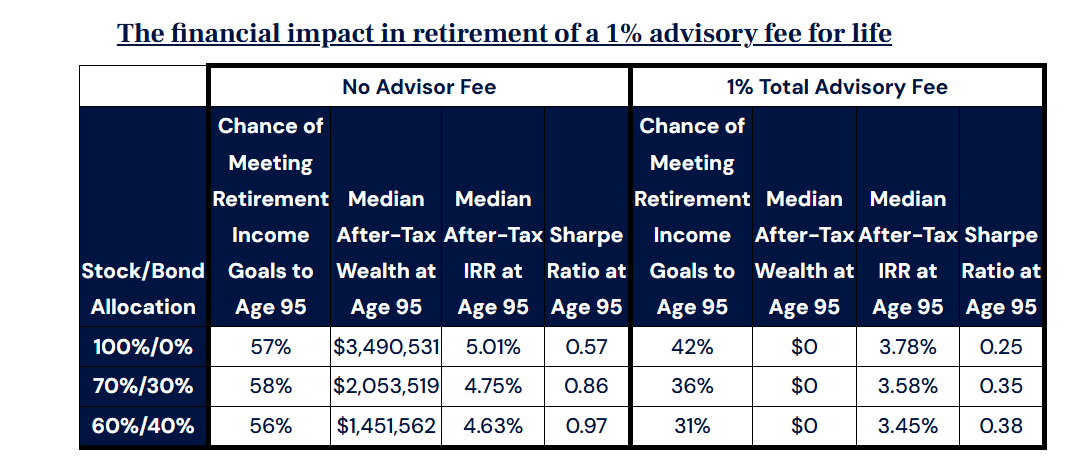

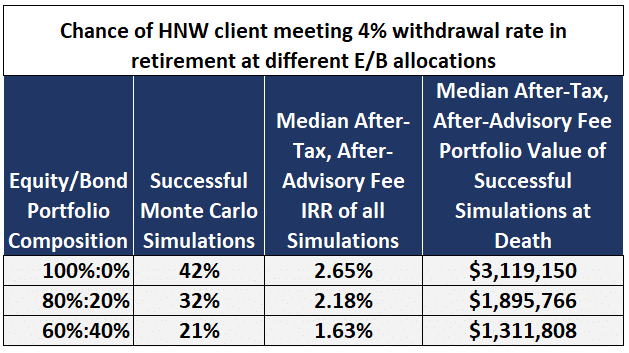

The choice to use an advisor in retirement is one that will cost clients and their beneficiaries millions of dollars in both fees and opportunity costs as we’ll show later in this article. If advisors are simply allocating clients to traditional stock-bond investment...

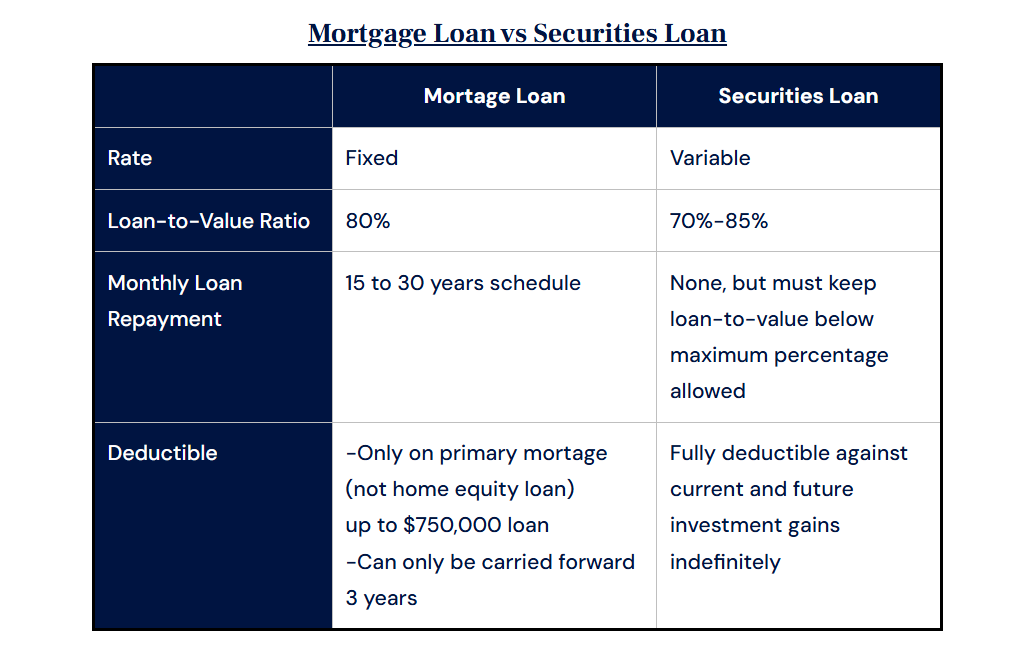

Anyone who has purchased a home is familiar with the concept of leverage. Most people when they purchase a home use 20% of their own money and borrow 80% from the bank. If the amount of appreciation on the home is more than the cost of the loan (and other costs of...

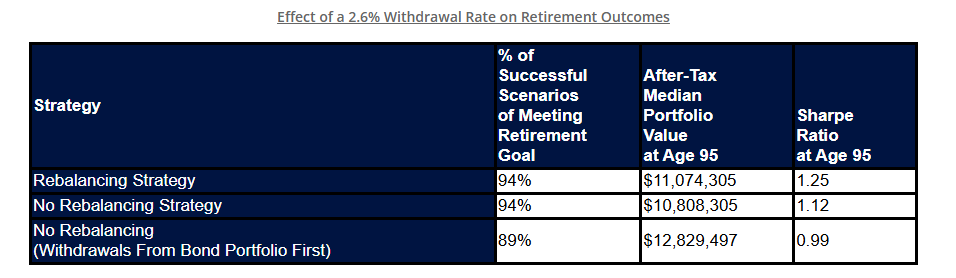

The traditional asset allocation glide path involves shifting client assets away from stocks and toward bonds as they near retirement. This approach reduces portfolio volatility and mitigates sequence of returns risk, potentially increasing the chance of meeting...

With interest rates at near 20 year highs, guaranteed lifetime income allows you the ability to lock-in these rates for the rest of your life while creating better retirement outcomesIf you own a home, then you’re probably wishing you had locked in a mortgage rate...

By using gifting strategies in place of contributing to a Roth IRA, high net worth clients can essentially replicate the benefits of a Roth IRA with larger contribution amounts and earlier withdrawal privileges.

In order for fee-only advisors to truly be fiduciaries they need to utilize life insurance products that are in the best interests of the clients.

How IUL policies allow portfolios to increase after-tax returns through increasing the equity allocation of the portfolio while minimizing volatility.

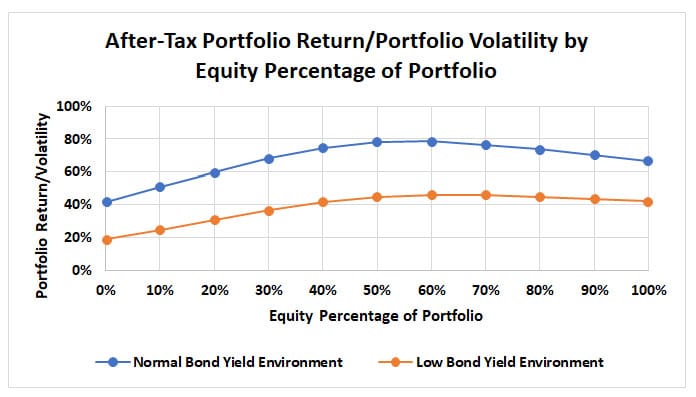

An overview of why low bond yields and a rising interest rate pose problems for portfolio diversification and how RIAs can utilize life insurance to achieve greater after-tax diversification and returns.

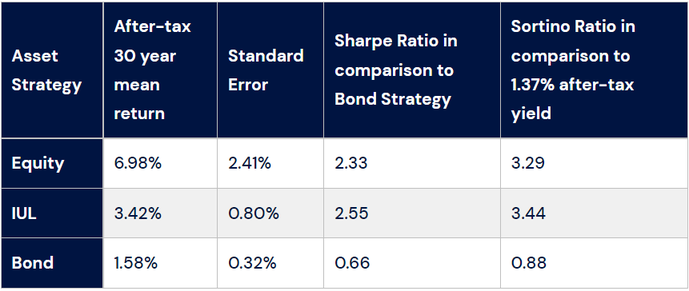

Financial advisors need to implement better retirement strategies in a low-yield environment or risk losing HNW clients A large bond allocation has long been the staple diversification tool for RIAs trying to manage market risk in their equity portfolios—especially...

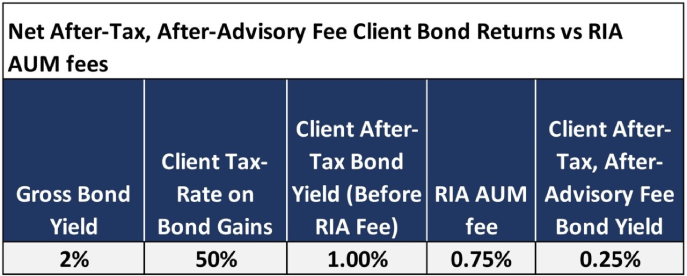

I’ve been working with financial advisors a lot recently on how to implement better after-tax, after-advisory fee strategies for the bond portion of their portfolios for clients who are in high marginal tax brackets (doctors, lawyers, business-owners, etc). In a...

I’ve been working with financial advisors a lot recently on how to implement better after-tax strategies for their doctor, lawyer, and business owner clients who are in high marginal tax brackets. Such strategies are especially important for clients who are near...