Increasing After-Tax Wealth for Ultra High Net Worth Clients w/ PPLI

Rajiv Rebello

Author

November 20, 2023

Author

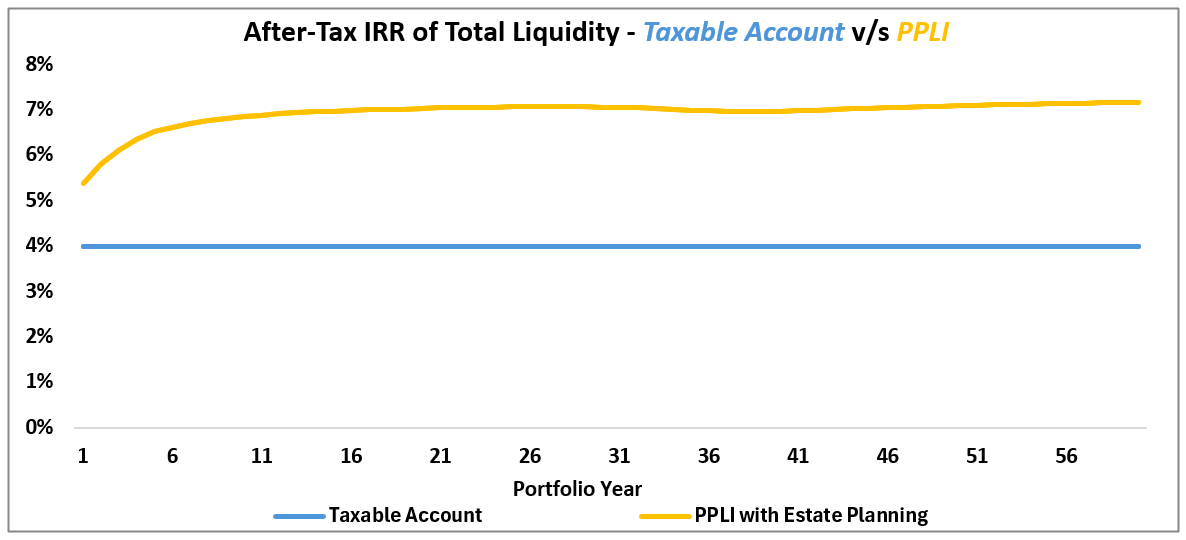

By placing tax-inefficient investments within a tax-free wrapper like PPLI and taking their money out via tax-free loans, UHNW clients can improve after-tax returns by nearly 300 basis points or more over the long-term compared to investing those assets within a taxable account (blue line). |

For ultra high net worth (UHNW) clients, many of their investment strategies become tax-inefficient due to their high income earning status. This includes traditionally tax-efficient long-term capital gains strategies for clients living in states with high state incomes on those capital gains or equity heavy strategies that involve frequent rebalancing.

Furthermore, since UHNW clients are in high tax-brackets, bond allocations lack the ability to provide diversification benefits and offset equity risk for UHNW clients due to both the low yields on these bonds and the high taxes owed on the limited gains.

With the estate tax limits set to sunset in 2026 from roughly $26M to approximately $14M, many more UHNW clients will need tax-efficient and asset-protected vehicles for their assets. Therefore, the ability to turn tax-inefficient equity and bond strategies into tax-efficient strategies can be one way for RIAs to add “tax alpha” to the portfolios of UHNW clients in order to make-up for the drag of low yields and high taxes on client portfolios. Unfortunately, like most HNW clients, UHNW clients are limited in their ability to convert their taxable portfolios to tax-advantaged retirement accounts that could help with this problem.

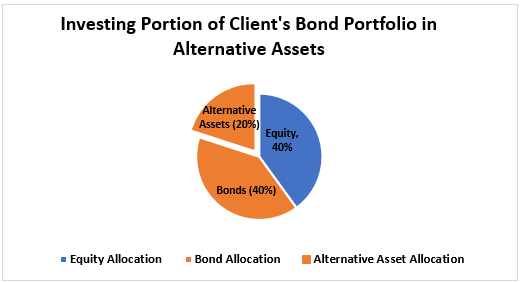

A potential solution for clients and their financial advisors is to replace a part of the low-yielding, tax-inefficient bond portfolio with higher yielding alternative asset allocations that have low correlation to equity markets. Low-correlation alternative assets can offer the diversification that bonds can provide for clients in lower tax-brackets and high yield environments.

But even if these assets are uncorrelated, a client switching asset allocations away from traditional equity and bond strategy to alternative asset allocations comes with downsides for both clients and their financial advisors. The main downside for high net worth clients is that many alternative assets are taxed at ordinary income tax rates that are higher than the long-term capital gains rates their equity portfolios were being taxed at.

Private Placement Life Insurance (PPLI), when structured properly, offers tax-efficient solutions for UHNW clients and their advisors to turn tax-inefficient strategies into tax-efficient strategies on large amounts of income for their tax-inefficient equity, bond, and alternative asset strategies. Clients benefit from tax-free investment strategies that would otherwise be highly taxable, and advisors get to keep these assets under management and continue to earn their regular asset under management fee on the assets in the tax-protected vehicle.

In addition, the ability for the advisor to charge his or her financial planning fee on higher-yielding, tax-free, uncorrelated alternative asset on a pre-tax basis offers significant advantages than charging that same fee on highly taxable investment strategies on an after-tax basis.

As we’ll see later in this blog, by moving tax-inefficient assets into a tax-free vehicle like PPLI, UHNW clients can improve their after-tax returns by nearly 300 basis points or more.

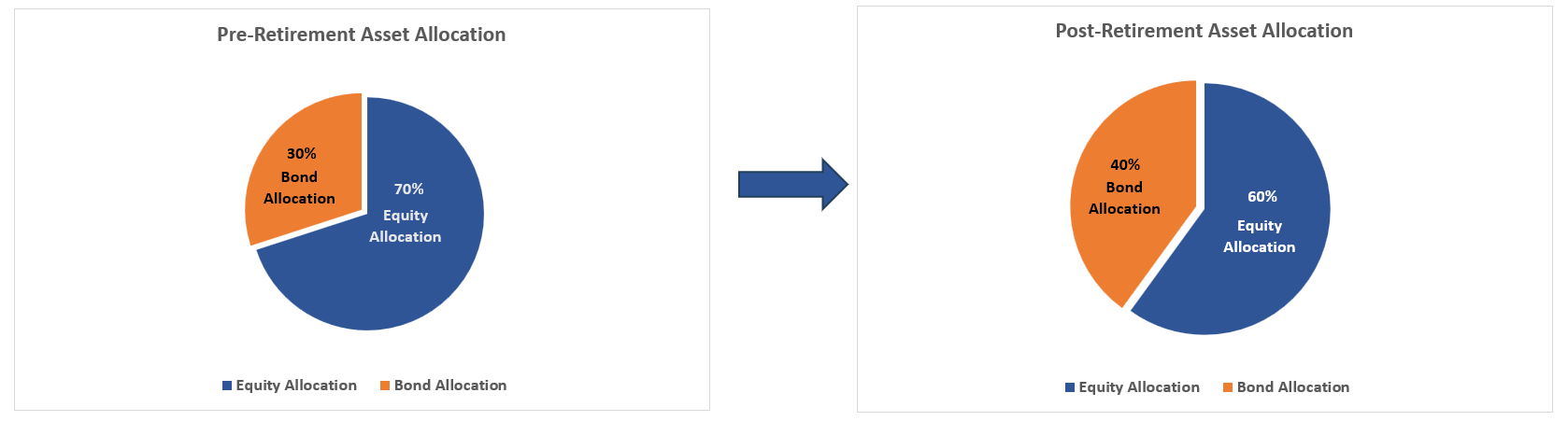

In an increasingly volatile equity market, clients nearing retirement often switch their asset allocations from a larger equity allocation to a larger bond allocation. Unfortunately, this comes at a high cost for high net worth clients. Not only do clients lose pre-tax return by switching from the higher earning equity allocations to the lower earning bond positions, they also pay a significantly higher ordinary income tax rate on the lower earning bond assets relative to the lower long-term capital gains tax rate they were paying on their equity positions. Furthermore, these bond allocations are subject to significant interest rate risk if interest rates rise.

As clients near retirement, they typically shift their asset allocations from a majority equity position like a 70%/30% equity to bond split to a larger bond allocation (like a 60% equity to 40% bond split) to protect from volatility in the equity markets. For a high net worth client this means giving up a high yielding asset for a lower yielding one and paying a significantly higher tax rate on the lower yielding asset as well. As a result, clients and their managers are constantly in search for high yielding uncorrelated assets to invest in instead of low-yielding, highly taxable bonds. |

A solution for this quandary is often to switch allocations to a larger alternative asset allocation instead of a larger bond allocation. Alternative assets can offer an expected return equal to or greater than equity markets. The downside of using alternative assets, however, is that often they can be just as volatile—if not more so—than equity investments while also being subject to higher short-term capital gains or ordinary income taxation. Furthermore, for financial advisors of these clients the result of a client pulling money out of an equity allocation that the advisor manages for the client into an alternative asset strategy that advisor doesn’t manage, is a loss of AUM fees on those assets the client is moving away from the advisor.

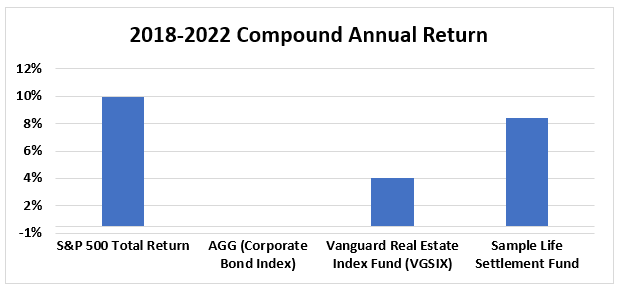

During the past 5 years, investors in equity markets like the S&P 500 have benefited from a strong bull run. For clients nearing retirement, the thought of moving their money to low-yielding bond funds (like the AGG) is unappealing—especially given the high tax rates they would pay on their bond gains instead of the significantly lower long-term capital gains rates they were used to paying on their equity gains. Alternative assets like real estate funds or life settlement funds can be attractive options given their high returns. Alternative assets like life settlements that have a low-correlation or are uncorrelated to traditional equity or bond markets are particularly appetizing as an alternative to a low-yielding bond market. |

For clients nearing retirement, pulling money out of their low yielding, tax-inefficient bond portfolio subject to interest rate risk and investing in alternative assets might make economic sense for the client. But if the client is pulling money out of their bond portfolio that their financial advisor manages and investing in alternative assets that are not under their advisors’ management, this means a loss of revenue for the advisor. |

What clients and their advisors need is the ability to invest in alternative assets—or even tax-inefficient equity investments—in a more tax-efficient structure which allows their financial advisors to still collect their asset under management fee. Utilizing the tax-benefits of variable life insurance through private placement variable universal life insurance is the most optimized way to accomplish these goals for both the client and their advisor.

Even if RIAs are able to manage alternative asset allocations for their clients, they’re still forced to charge clients their AUM fee on an after-tax basis instead of a pre-tax basis. Charging clients advisory fees on an after-tax basis further reduces the client’s net returns.

at End of Year | Return | Tax Return (But before RIA fee) | Return for Client (After taxes and RIA fees) | |

|---|---|---|---|---|

| 1 | 56 | 8.00% | 4.00% | 3.25% |

| 5 | 60 | 8.00% | 4.00% | 3.25% |

| 10 | 65 | 8.00% | 4.00% | 3.25% |

| 15 | 70 | 8.00% | 4.00% | 3.25% |

| 20 | 75 | 8.00% | 4.00% | 3.25% |

| 25 | 80 | 8.00% | 4.00% | 3.25% |

| 30 | 85 | 8.00% | 4.00% | 3.25% |

In the above example, a high net worth client at a 50% marginal tax rate decides to invest in tax-inefficient alternative assets at an 8% return. Taxes reduce the client’s net return by 50% and then the client has to pay the RIA’s 0.75% fee on the after-tax money further reducing the client’s net return. |

at End of Year | Return | Return (After Pre- Tax RIA fee) | Return for Client (After taxes and RIA fees) | |

|---|---|---|---|---|

| 1 | 56 | 8.00% | 7.25% | 3.625% |

| 5 | 60 | 8.00% | 7.25% | 3.625% |

| 10 | 65 | 8.00% | 7.25% | 3.625% |

| 15 | 70 | 8.00% | 7.25% | 3.625% |

| 20 | 75 | 8.00% | 7.25% | 3.625% |

| 25 | 80 | 8.00% | 7.25% | 3.625% |

| 30 | 85 | 8.00% | 7.25% | 3.625% |

In the above example, a high net worth client at a 50% marginal tax rate decides to invest in tax-inefficient alternative assets at an 8% return but is able to pay the RIA’s fee with pre-tax money. This reduces the taxable gain from 8% to 7.25% which means the client ends up paying the 50% tax rate on a lower amount. This results in a higher net after-tax return of 3.625% for the client than if the RIA’s fees were to be paid with after-tax money |

As the above example shows, any prudent financial advisor should always look at trying to put tax-inefficient assets (whether it be alternative assets, tax-inefficient equity strategies, or taxable bonds) into a structure where the RIA can charge their fee on a pre-tax basis instead of an after-tax basis.

for Long-Term Capital Gains in 2023 Year | |

|---|---|

| California | 13.30% |

| New Jersey | 10.75% |

| Washington D.C. | 10.75% |

| Oregon | 9.90% |

| Minnesota | 9.85% |

| Massachusetts | 9.00% |

| New York | 10.90% |

Certain states assess high marginal tax rates on long-term capital gains—in addition to the federal tax rate residents pay. This means that high earning individuals in these states can end up paying more than 30% of their capital gains in federal and state taxes which turns an otherwise tax-efficient asset into a tax-inefficient asset. Since the costs of a PPLI policy are typically less than 15% of the return, UHNW clients can achieve significant income tax savings by using a PPLI policy instead of investing through a taxable account. |

Long-term capital gains tax-rates are often seen as tax-efficient relative to ordinary income tax-rates. The top federal tax-rate on long-term capital gains in 2023 is 23.8% (20% top federal rate plus 3.8% Net Investment Income Tax). However, some states charge high state income taxes on these capital gains on top of the federal taxes. Therefore, clients in states with high taxes on long-term capital gains can end up paying 30% or more in taxes on these gains since they are paying the highest federal-tax rate (23.8%) plus whatever their state tax rate is on the gain. Since the costs of PPLI are typically under 15%, clients in such states can benefit materially from putting even equity strategies subject to long-term capital gains tax rates into a PPLI structure.

For decades now life insurance, particularly variable universal life (VUL), has offered high-net worth clients the coveted holy grail of investments: tax-free gains. While these products can offer life insurance protection and estate protection as a bonus, the key benefit for clients is that they can invest their money into a wide variety of investment options in the product and then pull out the vast majority of their principal and gains via a tax-free loan—while still having a residual death benefit that can be passed onto their beneficiaries tax-free and exempt from estate taxes.

Unfortunately though, traditional VUL policies have high commissions and expenses that often eat up a large amount of the tax savings the product provides. Unless the gross investment return within a traditional VUL policy is sufficiently high, the expenses within the product will often eat up most, if not all, of the potential tax-savings—particularly in the early years of the policy. In such cases the client would be better off investing directly in the underlying investments and paying the required tax on them. Furthermore, traditional VUL policies do not allow the RIA/family office to utilize its own investment strategy for their clients. This means that RIAs wanting to use VUL policies would be forced to put their clients into strategies created by other investment managers.

Private placement life insurance (PPLI) is a customized version of a variable universal life policy that drastically changes this dynamic. By ripping out the majority of the commissions and expenses in these PPLI products, high net-worth clients get significantly better after-tax results than they would achieve if they were to simply invest in the underlying assets directly.

VUL Policy | PPLI Policy | |

|---|---|---|

| Upfront Commission (Year 1) | 80%-100% of First Year Premium | 0%-1% of First Year Premium |

| Trial Commission (Year 2+) | 2-3% of Premiums | 0%-1% of Premiums |

| Premium Loads | 8%-18% | 0.08%-3.5% |

| Administrative Charge Per Year | ~$20,000- $48,950 | ~0.1-0.15% of AUM |

| Outside Portfolio Manager AUM Fee Per Year | 0.66% | 0% |

| RIA Advisory Fee | 0% | 0.25%-1.25% of AUM |

In exchange for a high premium contribution ($500k-$2M+), the PPLI policy is able to drastically reduce the commissions and expenses in comparison to the VUL policy. Furthermore, while the VUL policy requires that the client take their money away from their financial advisor and pay an outside portfolio manager to manage the assets, the PPLI product allows the financial advisor to create their own investment strategy and earn the same AUM fee on the assets in the tax-efficient PPLI structure that they would be earning if those assets were in a taxable account instead. |

Another key advantage that PPLI creates for financial advisors is that it allows the RIA the ability to create its own investment strategy and have the client invest in that strategy through the tax-efficient PPLI structure (the PPLI policy essentially serves as an insurance wrapper for the advisor’s own strategy) without paying an outside portfolio manager to manage the assets. This allows the advisor to charge the same AUM fee on the assets inside the tax-efficient PPLI structure as they would if the assets were kept inside a taxable account managed by the advisor.

A PPLI policy allows the advisor to keep the assets under the advisor’s control while benefitting from the tax-free nature of the life insurance policy. The advisor is able to earn the same asset-under-management fee on the assets in the PPLI structure as they would if they kept the assets in a taxable account. The difference is that the client is getting a better after-tax return by putting their tax-inefficient assets inside of a tax-free structure like the PPLI policy. In the long-run, putting tax-inefficient assets inside of a tax-free structure like the PPLI structure will accumulate larger assets for the client and a larger asset-under-management fee for the advisor. |

Furthermore, because of the immense tax-savings of the structure, even clients that invest in tax-efficient equity strategies can benefit from using a PPLI wrapper for their investments. Total costs for PPLI are typically under 15% of the gross return (often under 10% if the gross return is greater than an 8% IRR). As long as the client’s total tax rate on the assets in a taxable account is larger than the costs of the PPLI structure, clients are better investing in those assets through the PPLI structure than investing in them directly.

It’s no wonder then that when we look at the liquidity and IRRs of the PPLI product in contrast to investing in tax-inefficient assets directly, that the PPLI product provides significant advantages—while still allowing the RIA to charge an AUM fee on the assets.

| Taxable Account | Taxable Account | |||||

|---|---|---|---|---|---|---|

End of Year | Contribution for Year | Total Liquidity at End of Year | IRR of Total Liquidity at End of Year | Total Liquidity at End of Year | IRR of Total Liquidity at End of Year | |

| 56 | $2,000,000 | $2,080,000 | 4.00% | $2,107,553 | 5.38% | |

| 57 | $2,000,000 | $4,243,200 | 4.00% | $4,354,975 | 5.80% | |

| 58 | $2,000,000 | $6,492,928 | 4.00% | $6,763,015 | 6.11% | |

| 59 | $2,000,000 | $8,832,645 | 4.00% | $9,351,510 | 6.34% | |

| 60 | $0 | $9,185,951 | 4.00% | $10,004,258 | 6.52% | |

| 65 | $0 | $11,176,114 | 4.00% | $14,090,674 | 6.85% | |

| 75 | $0 | $16,543,379 | 4.00% | $28,211,372 | 7.03% | |

| 85 | $0 | $24,488,242 | 4.00% | $56,154,510 | 7.07% | |

| 95 | $0 | $36,248,580 | 4.00% | $107,232,001 | 6.97% | |

| 105 | $0 | $53,656,753 | 4.00% | $222,741,574 | 7.09% | |

By placing tax-inefficient investments within a tax-free wrapper like PPLI and withdrawing money via tax-free loans, UHNW clients can improve after-tax returns by over 300 basis points compared to investing those assets in a taxable account over the long term. The longer the client waits to take the tax-free loan, the better the IRR. This assumes a gross return of 8% and a tax-rate of 50%. |

As the above graph shows, using PPLI to invest in tax-inefficient assets helps improve the client’s after-tax IRR by nearly 300 basis points. The bulk of the advantage of the PPLI structure comes from being able to withdraw the principal and gains tax-free in the later years, rather than liquidating the gains early and paying taxes on them as would be required if the clients invested directly in the assets via a taxable account.

While PPLI can provide great after-tax advantages for high net worth clients and their advisors looking to invest in tax-inefficient alternative assets, there are some important considerations advisors should be aware of when evaluating the strategy:

1. Not all PPLI products are the same

Like any permanent life insurance product, not all PPLI products are the same. Some have higher cost of insurance (COI) rates, and limitations in their ability to take a tax-free loan than others. Others afford more preferential treatment to certain health conditions than others. Furthermore, different states/countries can have different premium load taxes. As such it’s important to research and do comparative analysis against different options available to the client.

2. Needs to be actively managed

Since the client is investing in assets with variable returns, it’s important that the advisor actively manage the policy. Since most PPLI products have high COI rates in the later years it’s important that the advisor is proactive in managing the policy in years in which the underlying assets have poor returns—particularly if the insured is in the later years. Doing so prevents the COI charges from getting astronomical and causing the policy to lapse.

3. Utilizing high-yielding tax-inefficient assets (preferably uncorrelated to equity markets)

One of the main problems with traditional VUL products is that they invest in underlying equities in which the client would typically be taxed at lower capital gains tax-rates if they invested in the assets outside the VUL structure. By investing in these types of assets within the insurance structure, the client is now exposed to insurance charges instead of tax-charges. Often times, the capital gains tax-rates are low enough such that benefits of investing in such assets within a tax-free structure does not offset the cost of the insurance and expense charges that the client will have to pay to put the assets in the structure.

Therefore, when choosing the assets to place within the structure the advisor really wants to focus on high yielding tax-inefficient assets in which the tax-benefits of investing through the structure significantly outweigh the insurance costs of doing so. Ideally the advisor also wants to focus on assets that are uncorrelated to the equity assets that the client will be investing through taxable accounts in order to try and help provide the portfolio diversification that bond allocations would play.

In a high tax environment, financial advisors can no longer settle for merely putting high net worth clients into taxable bond portfolios to offset equity risk as clients near retirement. Such allocations subject these clients to significantly lower gains, higher taxes, and interest rate risk. On top of that, an investment into taxable bonds means that high net worth clients will have to pay the advisor’s fee with after-tax money on already heavily reduced after-tax yields.

In such times, advisors really need to dig deep into their financial planning toolbox and determine how to account for the financial problems posed by highly taxable bond portfolios for their high net worth clients. One such way to provide the diversification that taxable bond portfolios used to provide is to use alternative assets (particularly uncorrelated assets) as a partial replacement for the taxable bond part of a client’s portfolio—or to put tax-inefficient client assets into a tax-free structure.

Tax-inefficient assets are often taxed at high ordinary income/short-term capital gains tax rates. Proper structuring of private placement life insurance allows clients the ability to invest in these assets tax-free within the structure while paying insurance costs that are significantly less than the taxes that would be owed if clients were to invest in these assets directly. It also allows for RIAs to implement their own strategies within the structure that they can then charge clients their advisory fee on a pre-tax basis which is significantly better than these clients taking their money away from the advisor and investing in these tax-inefficient assets directly.

Transform Your High-Net-Worth Clients’ Tax Strategy Today. Book a call to explore how private placement life insurance can enhance your advisory practice and deliver superior after-tax returns for your clients. Let’s discuss implementing tax-efficient solutions that maintain your advisory relationship while maximizing client outcomes.

Book a CallAuthor

Discover how Private Placement Life Insurance transforms charitable remainder trust strategies into powerful wealth replacement tools. Learn tax-efficient approaches that maximize charitable benefits while preserving family wealth for high-net-worth families.

This blog post explores essential PPLI due diligence steps, covering carrier evaluation, regulatory considerations, investment platforms, tax compliance, and advisor expertise to help high-net-worth individuals make informed decisions before implementing this specialized insurance solution.

Discover how PPLI enhances business succession planning through key person insurance and buy-sell funding. Learn private placement life insurance strategies for business owners.

0 Comments

Trackbacks/Pingbacks