Maximizing Wealth with Private Placement Life Insurance: A Comparison to Taxable Accounts

Rajiv Rebello

Author

February 11, 2025

Author

When it comes to optimizing investment strategies, one of the most powerful vehicles that ultra-high-net-worth (UHNW) individuals often use is a Private Placement Life Insurance (PPLI) policy. While many investors are familiar with taxable accounts, the world of PPLI offers significant advantages in terms of tax deferral and flexibility. These benefits make PPLI a particularly attractive option for those looking to minimize tax liabilities while enhancing wealth accumulation over time.

Despite these advantages, the decision to use PPLI instead of a taxable account requires careful consideration of various factors, including tax rates, investment objectives, and the investor’s specific financial situation. In this post, we’ll explore the fundamental differences between investing in a taxable account and using PPLI, and we’ll walk through a detailed case study to highlight how PPLI can outperform taxable accounts under certain conditions. We will also analyse how these differences can affect long-term wealth accumulation, giving you the insights needed to make an informed decision on whether PPLI is the right choice for your investment strategy.

Private Placement Life Insurance (PPLI) is a sophisticated investment vehicle designed primarily for ultra-high-net-worth individuals (typically those with a net worth of $10 million or more). This financial tool allows clients to invest in a wide range of assets while benefiting from key advantages, most notably tax-free growth on their investments.

PPLI can be thought of as a “Super Roth” for UHNW clients. In other words, clients contribute cash—or in sophisticated cases in-kind private equity interests—and the future growth in those assets is tax-free.

Unlike traditional life insurance policies, PPLI allows policyholders to create a customized portfolio within the policy. This means they can select from a broad spectrum of investments, including hedge funds, private equity, and other alternative assets, which are typically inaccessible through standard life insurance products.

The biggest advantage of PPLI is that the growth of these investments is free from both income tax and estate tax. This can significantly enhance wealth accumulation over time, especially for those looking to preserve wealth for future generations.

In addition to its tax advantages, PPLI can also offer creditor protection, making it an attractive option for clients in high-risk professions or those seeking to shield assets from potential litigation. To learn more about PPLI and its benefits, check out our previous blog post on the topic here.

In the following case study, we’ll take a closer look at how PPLI compares to a taxable account over time, illustrating how its unique advantages can lead to better financial outcomes under certain conditions.

For our case study, we’ll consider a 45-year-old male investor in average health living in California. This investor contributes $2,000,000 in cash for the first four years (a total of $8M). This cash is allocated to a 60/40 portfolio of stocks and bonds with an overall 8% net expected return.

The investor is subject to the following tax-rate assumptions: 37% for equity gains and 50% for ordinary income.

The PPLI policy expenses include:

Over the first four years, the investor makes the initial cash contributions, while in the later years no additional contributions are made. The PPLI structure allows for tax-free growth, meaning that the investments are not subject to taxes on dividends, capital gains, or interest income.

While the investor also benefits from estate tax protection, we will not be included the value of this estate protection in our analysis.

With these assumptions in place, we now compare two different investment scenarios:

By comparing these two scenarios, we can see how the unique tax advantages of PPLI can lead to better financial outcomes over time, particularly for high-net-worth individuals looking to maximize their wealth accumulation while minimizing tax liabilities.

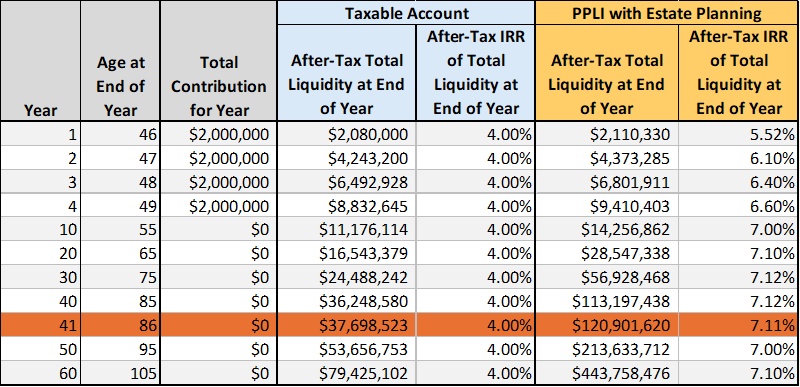

The case study results highlight key metrics for both the taxable account and PPLI, including after-tax liquidity, death benefit, and internal rate of return (IRR) over a 60-year period. The table and chart below provide a comparison of these results:

Investing in the same portfolio via PPLI instead of a taxable account results in 98% more wealth at life expectancy (41 years) |

The table and chart above show us the immense value PPLI can have over investing in this portfolio via a taxable account.

Choosing to invest the $8M in that same portfolio within a PPLI vehicle has immediate benefits starting in year 1 with the gap widening significantly over time. By the time the investor reaches their life expectancy (age 86), the PPLI investor’s total value has increased even further, reaching a remarkable $120.9 million in the PPLI vehicle, compared to the taxable account’s value of $61 million.

Ultimately this amounts to a 7.11% after-tax IRR at life expectancy when the client invests in the portfolio via PPLI as opposed to a 5.27% after-tax IRR at life expectancy if the client were to invest in that same portfolio via a taxable account.

Note that the above analysis does not include the drag of estate taxes which would result in the taxable account showing significantly lower values than what is being shown currently in the taxable account. The use of a PPLI vehicle, on the other hand, helps protect clients from these estate taxes as well.

Contact us by filling the form, and we’ll get back to you soon!

Contact UsIn the previous case study we looked at putting the entire client portfolio within a PPLI vehicle versus a taxable account. However, remember that in a 60/40 portfolio, 60% of the portfolio is in equities which are relatively tax-efficient since the majority of the returns are unrealized gains that can be deferred until assets are actually sold. Furthermore, long-term capital gains rates are typically lower than ordinary income tax rates. In our client case, for example, the client pays only 37% on long-term capital gains, but 50% on ordinary income or short-term capital gains.

So an important question to ask here is:

In this example, we still assume that the client puts in $8M into the PPLI vehicle earning a gross 8%. But in this example, we’re going to assume that 100% of the assets are taxed yearly at 50% ordinary income rates—as opposed to some of the portfolio being taxed at long-term capital gains rates.

The value add can be seen in the table and chart below.

Investing in 100% bond portfolio via PPLI instead of a taxable account results in 221% more wealth at life expectancy (41 years). |

Choosing to invest the $8M only the most tax-inefficient part of the portfolio within a PPLI vehicle maximizes the value of the PPLI vehicle. By the time the investor reaches their life expectancy in 41 years (at age 86), the PPLI vehicle has added over $83M of after-tax value over investing this part of the portfolio in a taxable account ($120.9 million versus $37.7 million).

Ultimately this amounts to a 7.11% after-tax IRR at life expectancy when the client invests this part of the portfolio via PPLI as opposed to a 4.00% after-tax IRR at life expectancy if the client were to invest in that same part of the portfolio via a taxable account.

This is a gain of over 300 basis points.

This case study highlights the substantial advantages of Private Placement Life Insurance (PPLI) over taxable accounts, particularly for high-net-worth individuals and the tax-inefficient parts of their portfolio (hedge funds, alternative assets, private credit, etc). The more tax-inefficient the asset is, the more value PPLI can have for the client as an investing vehicle.

The key benefit of PPLI is its tax-free feature, which allows for greater compounding of returns over time, driving enhanced wealth accumulation. Additionally, PPLI offers estate tax protection and a robust death benefit, making it an attractive option for long-term investors focused on wealth preservation and transfer.

Author

Discover how Private Placement Life Insurance transforms charitable remainder trust strategies into powerful wealth replacement tools. Learn tax-efficient approaches that maximize charitable benefits while preserving family wealth for high-net-worth families.

This blog post explores essential PPLI due diligence steps, covering carrier evaluation, regulatory considerations, investment platforms, tax compliance, and advisor expertise to help high-net-worth individuals make informed decisions before implementing this specialized insurance solution.

Discover how PPLI enhances business succession planning through key person insurance and buy-sell funding. Learn private placement life insurance strategies for business owners.

0 Comments