PPLI: Tax-Efficient Investing for UHNW Clients

Rajiv Rebello

Author

January 31, 2025

Author

Summary:

In a rising interest rate and high tax-rate environment, current investment and estate planning strategies are no longer sufficient to meet client needs.

Private placement life insurance (PPLI) allows RIAs, CPAs, portfolio managers, estate attorneys, and trust officials the ability to create investment and estate strategies that minimize tax drag and offer better risk-adjusted portfolio solutions for their Ultra-High Net Worth (UHNW) clients.

Using private placement life insurance allows UHNW clients and their advisors the ability to essentially create a “Super Roth” retirement and estate investment strategy that allows for a more optimal risk-adjusted and tax-efficient portfolio solution that protects clients from current and future tax increases.

For RIAs and portfolio managers, PPLI allows these advisors to charge their fee from within the vehicle instead of from an after-tax account. This helps minimize the drag of the advisor’s fee on returns. In this article we will take a look at why bond allocations in a rising interest rate and high tax rate environment are not sufficient to create optimal risk-adjusted portfolio solutions and how PPLI can be utilized to create both portfolio alpha and “tax alpha”.

Are Your Current Strategies Failing Your UHNW Clients?

Book a CallCurrent modern portfolio theory rests on the idea that a portfolio can be constructed that maximizes the return of a portfolio for a given amount of risk. The basic idea is that creating a portfolio of two or more asset classes that are ideally negatively correlated can help to optimize the return of the entire portfolio for a given amount of risk.

This is where the idea of the 60% stock portfolio and 40% bond portfolio originated. Researchers found that this was the optimal portfolio to optimize the return of a portfolio for a given amount of risk. However, this efficient frontier model has two key flaws:

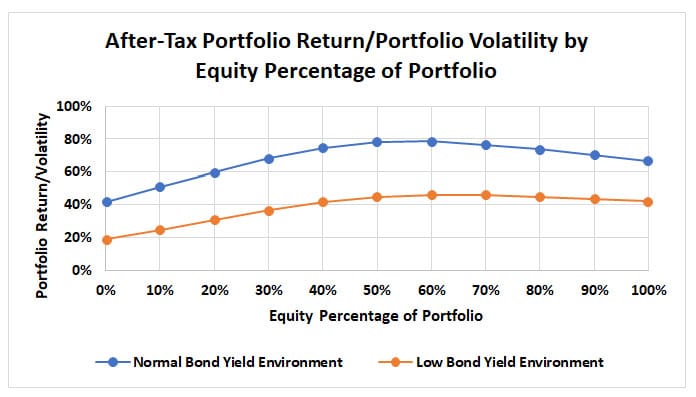

In a normal bond yield environment the 60% equity and 40% bond portfolio can optimize the portfolio’s return relative to the underlying risk. However, in a low-yield environment this is not the optimal allocation due to the low yields and higher taxation of bonds. In fact, in a low bond yield environment investors can increase the equity allocation of a portfolio to 100% in order to increase the return of the portfolio without significantly hurting the return-to-risk ratio.

When equities have higher expected returns than debt, increasing the allocation of a portfolio to equities increases the mean expected return of the portfolio. But doing so also increases the expected volatility of the portfolio. As such, the efficient frontier helps us to determine the optimal equity allocation of a portfolio that maximizes the return of the portfolio relative to the volatility or risk being taken. That’s why in a normal bond yield environment, increasing the equity allocation of a portfolio beyond a certain point results in the return of a portfolio relative to its underlying risk decreasing as evidenced by the “Normal Bond Yield Environment” line (blue line). We can see that in a “normal bond yield” environment that optimal equity allocation to maximize the return/risk ratio is about 60% equity allocation (the remaining 40% is allocated to bonds).

However, in a low bond yield environment (orange line), increasing the equity allocation results in greater expected return with minimal costs to volatility especially since low bond yields are taxed at a higher rate than equity earnings. Increasing the equity allocation from 60% to 100% results in a barely noticeable decrease in the return/risk ratio in a low bond yield environment.

Modeling assumptions:

It’s not difficult to understand how low bond yields and the higher taxation of bonds make allocating to bonds not worthwhile for investors in this current environment—particularly in states like California with high state income taxes. But a quick numerical example can help illustrate the impact.

After-tax returns of Stock and Bond Investments

| (A) | (B) | (C ) = (A) * (1-B) | |

|---|---|---|---|

| Gross Return | Tax-Rate | After-Tax Return | |

| Stocks | 10% | 37.1% | 6.290% |

| Bonds | 2% | 54.1% | 0.918% |

On an after-tax basis, low-yielding, highly taxable bonds add very little to the overall portfolio return.

Assumptions:

Marginal Long-term capital gains tax-rate (stocks): 20% federal + 13.3% CA state + 3.8% Medicare Surcharge = 37.1%

Marginal Ordinary income tax-rate (bonds): 37% federal + 13.3% CA state + 3.8% Medicare surcharge = 54.1%

For an RIA that’s looking to allocate clients to a bond portfolio, such an allocation can actually create negative net returns for the client after taxes, RIA fees, and inflation are taken into account.

Real returns of Stock and Bond Investments after taxes, fees, and inflation

| (A) | (B) | (1-B) | (D) | (E) | (F) | (G) | (D)-(E ) -(F)-(G) | |

|---|---|---|---|---|---|---|---|---|

| Gross Return | Tax-Rate | After-Tax Return Before Fees | Wealth Manager Fee | Fund Manager Fee | Platform Fee | Cost of Inflation | Net Client Return after taxes, fees & inflation | |

| Stocks | 10% | 37.1% | 6.290% | 1% | 0.50% | 0.20% | 2.25% | 2.34% |

| Bonds | 2% | 54.1% | 0.918% | 1% | 0.25% | 0.20% | 2.25% | -2.78% |

After taxes, fees, and inflation, allocations to bond investments offer negative real rates of return in a low yield environment.

Over the past year, inflation has remained a key concern, prompting the Federal Reserve to maintain a higher-for-longer interest rate stance. After a series of aggressive rate hikes in 2022 and 2023, the Fed has signaled a cautious approach in 2025, with discussions around potential rate cuts depending on economic conditions.

For clients that currently are heavily invested in bonds, an increase in interest rates poses heavy losses for these investments that may take years or decades to recover from.

Effect on bond prices of raising interest rates by 1%

| Bond Term (Years) | Immediate Loss of Market Value of Bond Prices on 1% Increase in Rates from 2% to 3% | Years of investing at higher coupon rate (3%) to recoup initial upfront loss in value | Years of investing at higher coupon rate (3%) to get back to original 2% yield |

|---|---|---|---|

| 10 | -8.53% | 4 | 10 |

| 20 | -14.88% | 6 | 17 |

| 30 | -19.60% | 8 | 23 |

In a low-interest rate environment, bond prices are more sensitive to an increase in rates. As the table above shows, a 1% increase in rates from 2% to 3% creates a large upfront loss that can take clients an extremely long-time to recover from.

In addition to rising interest rates, which make low-yielding bonds even less appealing, it appears that both Democratic and Republican parties will have their own reasons for increasing income and/or estate taxes on the wealthy. High taxes on bond gains further reduce the viability of fixed income for wealthy clients in creating diversified portfolio solutions. Democratic and fiscally conservative agendas point to increasing taxes on the wealthy.

On the left, Democrats have increasingly pointed out income inequality and the gap in wealth between the richest Americans and the middle class in their talking points and have increasingly aimed to cut loopholes that previously allowed the wealthy to reduce or eliminate their taxes.

The original Biden tax-proposal included a number of elements aimed at increasing taxes on the wealthy:

While none of these elements were ultimately passed, the Democratic agenda was clear: Increasing taxes on the wealthy is a key priority that they are unlikely to walk away from in the near future.

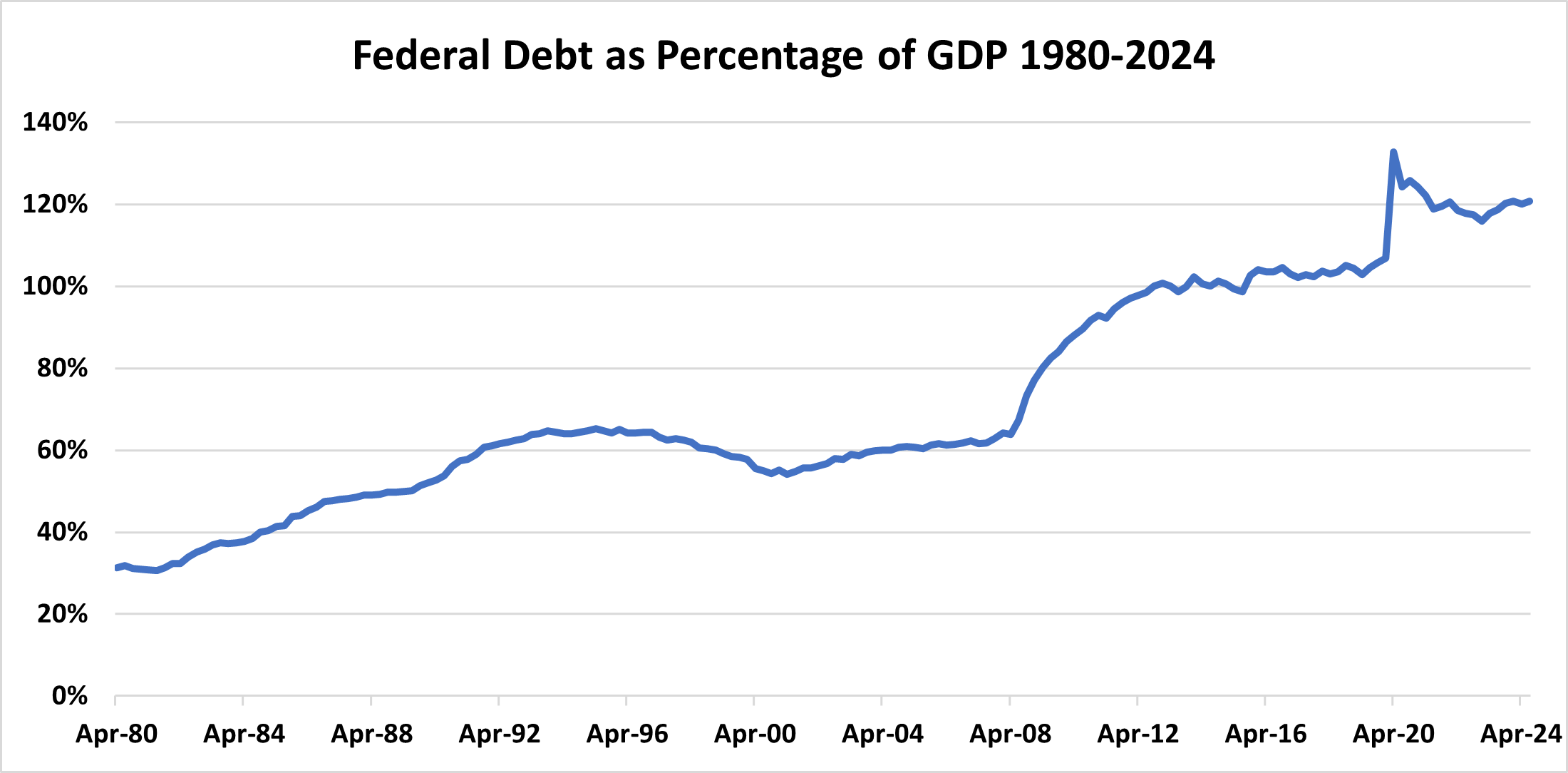

Although increasing taxes on the wealthy is a current refrain of the democratic party, rising debt to GDP levels in the wake of large COVID spending bills point to a need for higher taxes (as well as reduced spending) from a purely fiscally conservative position as well. Given that raising marginal tax-rates is anathema to the right due its perceived effects on private investment into the economy, it’s more likely that the right will agree to reduce estate tax exemptions in order to compromise with the left. Given that estate tax exemptions are set to sunset in 2026 anyways, it’s unlikely that future generations will be able to transfer as much generational wealth tax-free as they have in recent years due to increasing pressure to address both federal debt levels as well as wealth inequality in the U.S.

Federal debt as a percentage of GDP has steadily increased since the global financial crisis of 2008 including a large uptick in 2020 due to Covid-19 spending bills. While low interest rates have lessened the impact of the debt on the economy, debt as percentage of GDP is projected to continue to increase in the future necessitating the need for increased taxes on the wealthy in the future—most likely in the form of higher estate taxes.

While low-yields and rising interest and taxes on the wealthy pose a notable problem for the wealthy individuals, they also provide an opportunity for advisors to these clients to create niche solutions for these issues that other advisors aren’t creating.

If you’re an advisor to HNW or UHNW clients, there are two key ways to address these issues:

As we discussed earlier, low-yielding bonds no longer provide the same diversification benefits to equity risk that they did in a higher interest rate environment. In fact, in a rising interest rate environment bonds can pose more risk than benefit.

In order to provide better diversification and higher risk-adjusted returns, portfolio strategies need to look at other strategies that have lower/negative correlation to market risk in the equity markets and/or higher risk-adjusted returns in comparison to bonds.

For example, alternative strategies like life settlements, reinsurance, volatility strategies, etc can help offset equity risk in the portfolio while also helping the portfolio provide higher risk-adjusted returns.

In a high tax-rate environment the ability to create solutions that protect clients’ investment strategies from both current and future tax laws can provide immense value and allow advisors to craft their own niche amongst the ultra wealthy.

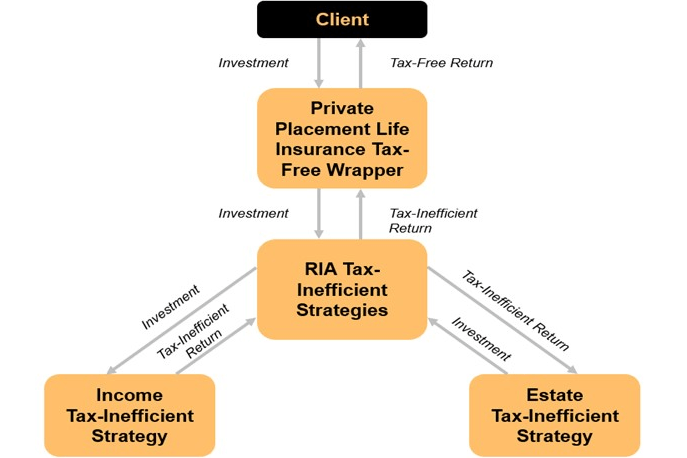

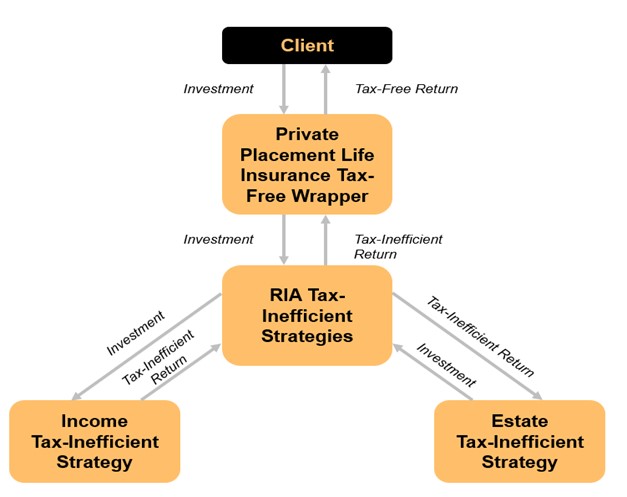

Private placement life insurance (PPLI) is a vehicle that helps advisors to UHNW clients address both of these issues by creating better risk-adjusted portfolio solutions in which the gains are free from both income and estate taxes.

Private placement variable universal life (PPVUL) insurance, also known as just private placement life insurance (PPLI), is a customized version of variable universal life insurance (VUL) that allows policyowners and their financial advisors a significantly reduced expense structure and more flexibility in how the underlying investment strategy is chosen and who it is managed by. This allows clients to chose their own RIAs to manage their investment strategy and have all the principal and gains be tax-free and outside of the client’s estate.

Essentially the PPLI vehicle serves as a “Super Roth” retirement strategy by which to invest millions of dollars of assets that will be both tax-free and outside of the client’s estate. Investment managers can then invest this money at their discretion. Ideally the best strategy for these assets are ones that would be income tax-inefficient or estate tax-inefficient if invested in outside the PPLI policy.

Making Investing in Tax-Inefficient Assets Tax-Free through PPLI

PPLI allows RIAs to invest the parts of their clients’ portfolio that are tax-inefficient into a structure that makes the gains free from both income tax and estate taxes.

Income tax-inefficient strategies are taxed at high ordinary income or short-term capital gains rates and often lack the ability of tax-deferral. Some income tax-inefficient strategies are high yield debt strategies, long/short strategies, high portfolio turnover strategies, volatility strategies, hedge fund strategies, and life settlements. Also equity strategies can be tax-inefficient for clients living in states that charge high state income taxes on capital gains (California, Hawaii, New Jersey, Oregon, etc.).

Estate tax-inefficient strategies are assets that are expected to experience rapid growth in the future and could subject the client to an estate problem (especially with the future reduced exemption limits). These strategies include venture capital strategies, individual stock strategies, and art investing.

| Income Tax-Inefficient Asset Examples | Estate Tax-Inefficient Asset Examples |

|---|---|

| High Yield Debt | Venture Capital |

| Hedge Funds | Growth Stocks |

| Long/Short and High Turnover Strategies | Closely held business interests |

| Alternative Assets | |

| Life Settlements | |

| Equity strategies for clients in states with high capital gains tax rates |

Ready to Explore PPLI?

Book a CallGrantor trust strategies like grantor annuity trusts (GRATs) or Intentionally Defective Grantor Trusts (IDGTs) are popular estate planning tools as they allow clients the ability to move assets outside of their estate and have them grow free from the estate tax. However, the downside with this approach is that even though all the investment growth is outside of the estate, the realized taxable gains are fully taxable to the grantor. Furthermore, assets in grantor trusts don’t qualify for step-up in basis. So when the grantor does die, any unrealized gains on the assets in the grantor trusts creates a large tax-liability for the beneficiaries. In order to counter this, clients using IDGTs must utilize swap powers to swap out the low basis assets in the IDGT with high basis assets outside of the IDGT. The downside with these swap powers is that if the client waits too long to use the swap powers and the client dies beforehand, then all the grantor trust assets are fully taxable. Also, in order to use the swap powers the client has to have an equal amount of assets outside the IDGT as they do inside the IDGT. For those that have gifted the majority of their wealth to the IDGT in the first place, this might not be a realistic possibility.

A PPLI vehicle, on the other hand, allows all the investment gains to be outside of the estate and tax-free for both the client and the client’s beneficiaries without worrying about swap power issues. Furthermore, even if step-up in basis is repealed in the future—like the Democratic proposal attempted to repeal in 2022—this will not affect the assets in the PPLI vehicle. So using PPLI in combination or in place of grantor trust strategies like GRATs or IDGTs creates a more comprehensive investment and estate planning solution for RIAs, estate attorneys, and their clients.

| Estate Planning Strategy | Benefits | Downsides |

|---|---|---|

| Grantor Trust Strategies (GRATs, IDGTs) | -Assets grow outside of the estate -Can get discounted valuation on transfer of assets into trust (IDGTs) -Can take taxable loan for liquidity | -Investment growth is taxable to the grantor -Assets don’t qualify for step-up in basis on death. Have to use swap privilege (IDGT only) |

| PPLI | -Assets grow outside of the estate and tax-free to client -Can get discounted valuation on in-kind transfers (offshore only) –Tax-free loan for liquidity | -Have to manage insurance risk/expenses |

Similar to a Roth IRA, UHNW clients can use the PPLI vehicle to accumulate tax-free growth for retirement or to pass on wealth tax-free to their beneficiaries—or a combination of both.

If the client wishes to fully exit the vehicle instead of taking a tax-free loan, they are free to do so at any time. Similar to a Roth IRA, they can take out their principal with no taxes or penalties or surrender charges. While there are no surrender charges on the gains either, there are insurance expenses and ordinary income taxes owed on the gains. These insurance expenses are high in the early years as a percentage of the assets in the vehicle but low in the later years. If the client exits early, these insurance expenses will eat up a good portion of the game that they could have readily accessed in the later years without loss.

For those looking to exit early, the PPLI vehicle allows clients the ability to take out up to 90% of the principal and gains tax-free. Therefore, it’s better to use the tax-free loan option to take out 90% of the total principal and gains tax-free than to just exit early and have the gains be subject to ordinary income taxation. In order to gain the most benefit from the tax-free PPLI vehicle clients should aim to keep the assets in the vehicle for at least 10 years before removing the assets via liquidation or a tax-free loan.

PPLI (also known as PPVUL) is just a customized version of traditional VUL product offered at most large life insurance carriers. However, PPLI has significant advantages over traditional VUL products for two key reasons: significantly lower expenses and a larger spectrum of tax-inefficient strategies to invest in.

The PPLI market is able to offer significantly lower expenses due to the fact that it benefits from economies of scale and that it eschews large upfront commissions in place of a small trail commission for the life of the policy. Wealthier clients invest significantly more in assets into a PPLI policy than they do into a traditional VUL policy. This means that the product has more built-in economies of scale available to it and the insurance company can have a smaller expense ratio on a larger base of assets and be just as profitable as the traditional VUL policy which charges a larger expense ratio on a smaller base of assets.

Another reason why PPLI products have lower expense ratios is that PPLI products replace the large upfront commission (which is often 80%-100% of the first year premium) with a small trail commission. Changing this commission structure means that actuaries don’t have to build in large expense and surrender charges within the policy to recover the large upfront commission which results in a PPLI product with significantly less drag on returns than traditional VUL products. Also, wealthier individuals tend to have better access to healthcare, which means that insureds in PPLI products are typically living longer than the general insurance population and have lower expected mortality costs for the insurance carrier providing the coverage.

Another huge advantage of PPLI over traditional VUL products is the investment flexibility and availability of investment options. Most investment options available within a traditional VUL product are equity investments which are already tax-efficient and qualify for step-up in basis—so the need to put these assets into a tax-protected vehicle is limited unless the client lives in a state with high state income taxes. PPLI on the other hand allows clients to work with their own investment advisors to craft a strategy that is specific to them that would maximize the tax-benefit to the client. This includes a variety of alternative asset investments that would otherwise be tax-inefficient if invested outside the PPLI vehicle.

Comparison of illustrative expenses in a VUL vs PPLI policy

| Category | Illustrative $9M VUL policy | Illustrative $9M PPLI policy |

|---|---|---|

| Upfront commission | 80%-100% of 1st year premium | 0.15% of AUM |

| Trail commission | 2%-3% of premiums | 0.15%-0.2% of AUM |

| Premium loads | 8%-18% of premiums | 0.08%-3.5% of premium loads |

| Administrative charge | $20k-$40k/year | 0%-0.15% of AUM |

| M&E charge | 0.2%-0.4% | 0.2%-0.3% |

| Surrender charge | 15-20 year schedule | None |

| Cost of Insurance charges | Higher due to worse health of less wealthy population | Lower due to better health of wealthy population |

| Outside Portfolio Manager Fee | 0.66% | 0% |

| RIA Advisory Fee | 0% | 0.75%-1% |

| Investment option availability | Limited, mainly tax-efficient equity funds | At RIA’s discretion, includes tax-efficient and alternative strategies |

PPLI policies have lower insurance expenses and more investment flexibility than traditional VUL policies.

PPLI Costs vs Income Tax and Estate Tax Rates

| Category | Top Federal Tax Rate | Top CA State Income Tax Rate | Medicare Surcharge | Plan Cost/ Expenses | Total Tax/Cost |

|---|---|---|---|---|---|

| Ordinary Income | 37% | 13.30% | 3.80% | 0% | 54.10% |

| Long term Capital Gains | 20% | 13.30% | 3.80% | 0% | 37.10% |

| Estate Tax | 40% | 0% | 0% | 0% | 40% |

| PPLI | 0% | 0% | 0% | 5%-20% | 5%-20% |

When properly managed, the insurance costs and expenses of the PPLI vehicle are significantly cheaper than marginal ordinary income, long-term capital gains, or estate tax rates for those clients in the highest brackets

PPLI is a solution that is only available to clients who are qualified purchasers ($5M or more in investments) who are willing to commit at least a total of $1M to $2M to the vehicle over 4 years. Clients who are qualified purchasers should also have one or more the following attributes:

One of the main benefits of PPLI is to protect clients who either currently have an estate tax issue or may have one in the future if estate tax limits change.

In the wake of low bond yields and rising interest rates, alternative assets can provide greater portfolio alpha. However, alternative strategies are often not tax-efficient. The PPLI vehicle allows clients who want greater access to these solutions to invest in them in a tax-efficient manner.

Traditionally equity strategies have been taxed at lower long-term capital gains. However, some states charge high state income taxes on these long-term capital gains. For clients in living in such states, it can be valuable to use the PPLI investment to manage equity strategies that are tax-inefficient.

| State | Top Marginal Bracket on Capital Gains Rates |

|---|---|

| California | 13.3% |

| New Jersey | 10.75% |

| Oregon | 9.9% |

| Minnesota | 9.85% |

| New York | 8.82% |

| Vermont | 8.75% |

| Iowa | 8.53% |

| Arizona | 8.00% |

| Wisconsin | 7.65% |

Equity investments and long-term capital gains are usually tax-efficient. However, states that charge a high tax-rate on capital gains investments result in these investments becoming tax-inefficient for wealthy clients living in these states.

Like any investment plan, clients need to dump in as much as possible for as long as possible and to minimize investment expenses in order to maximize investment growth. However, life insurance policies limit the ability for clients to dump-in large amounts of money based on the insured’s age. If the client is too young, then they are limited in their ability to contribute to the vehicle to begin with. However, if the insured is too old when they acquire the policy the high insurance expenses associated with the age of the insured can eat up a lot of the tax-benefits of the policy—especially if the investment strategy has poor returns at the same time.

While PPLI can provide greater tax-advantaged portfolio and estate solutions, it comes in exchange for having to manage additional risk—namely insurance risk. As such, there are a couple of key areas that clients need to be aware of before committing to the vehicle:

Clients and their advisors need to treat the PPLI investment vehicle the same way they would for a Roth IRA and understand that just like a Roth IRA, this is a long-term investment vehicle. While a Roth IRA and a PPLI vehicle both allow clients to take out their principal at any time without a penalty, taking out gains early results in charges being assessed on the gains. With a Roth IRA clients will pay a 10% penalty and then have to pay ordinary income taxes on the gain. With a PPLI vehicle, clients will have insurance expenses deducted from their gains and then have to pay ordinary income taxes on the remainder of the gains. The amount of insurance expenses will depend on how early the client exits the investment. The earlier they liquidate, the larger the insurance expense deduction is. Typically the break-even point here is between 7-10 years. In other words, if the client exits a PPLI investment before 7-10 years, then they would have been better off having invested directly in the underlying assets via a taxable account then through the PPLI structure. Also, as we discussed before, instead of liquidating the investment completely and having to endure these deductions, clients can typically take up to 90% of the principal and gains out via a tax-free loan. This is a much better alternative than liquidating 100% of the investment.

Most retirement plans come only with contribution and investment risk. In other words, if the client doesn’t contribute enough to the retirement account then there won’t be enough investment growth over time to provide them with the retirement income they need. However, with insurance policies this risk is exponentially magnified. If clients stop contributing to their PPLI vehicle then insurance expenses will eat up the investment gains. Conversely, if clients properly fund the vehicle then the insurance expenses will eat up only a small portion of the gains. This is why the goal of the policy is not to maximize the death benefit, but to minimize the death benefit and maximize the contributions to the vehicle. For those interested in more information, I’ve previously written about the importance of minimizing the insurance charges in order to maximize the CSV IRR and the reasons behind this.

Failure to properly contribute to a life insurance policy is one of the main reasons why life insurance policies underperform policy owner expectations. This underperformance is often entirely blamed on the insurance policy when in reality a large amount of the blame belongs on the policy owner and his or her advisors for failing to understand and actively manage the risks. These same risks also need to be managed when the underlying investment strategy underperforms and exposes the policy to more insurance risk. The policyowner and the advisors need to be proactive about reducing the death benefit, utilizing loan provisions, and taking less investment risk as the client ages and the cost of insurance charges increase.

An often neglected area in the set-up of both regular and PPLI life insurance policies is choosing the right state from which to have the policy issued in. Different states assess different premium load expenses on the premiums being paid into the policy. These premium load expenses can be as low as 0.08% of the premium paid into the policy to as high as 3.5% of all premiums being paid into the policy. South Dakota currently has some of the lowest premium state taxes with a 2.5% premium load up to $100,000 in a given year and only 0.08% above that. This means that clients are better off dumping large amounts of premium into a policy in one year as opposed to spreading it out evenly over a number of years.

Note that insureds do not need to live in South Dakota in order to have a policy issued in South Dakota. The trust or LLC that owns the policy needs to be located in South Dakota.

There are two types of life insurance carriers that offer PPLI: carriers that are based outside of the United States (offshore carriers) and carriers that are based in the United States (onshore carriers). Onshore and offshore companies have different pros and cons.

Onshore companies typically have lower cost of insurance charges, M&E charges, and better loan provisions, but have less flexibility when it comes to investment strategies. Offshore companies on the other hand, are more open to allowing more niche and alternative investment strategies, but have higher cost of insurance and M&E charges and less attractive loan provisions. Some offshore companies can also skirt the intent of the law—even if they abide by the letter of the law—by allowing discounted valuation practices on in-kind securities. While this is currently allowed in grantor trust strategies, utilizing these strategies in PPLI may be contested by the IRS. As such, whenever considering utilizing offshore life insurance companies for complex estate planning strategies like this, it’s important to work with an established estate attorney who can offer a statement of opinion or get a definitive private letter ruling from the IRS.

In the wake of low bond yields and rising interest and tax rates, using PPLI as an investment and estate planning vehicle allows RIAs, CPAs, and estate attorneys who provide services to UHNW clients to provide more holistic tax-efficient portfolio and estate planning solutions to their clients—which ultimately will help both retain and attract more UHNW clients.

Wealth managers using PPLI for their UHNW clients will be able to create better risk-adjusted and diversified portfolio solutions for their clients—all while charging their fee on a pre-tax basis instead of the more expensive after-tax basis.

Estate attorneys that choose to use PPLI in combination or in place of their existing Grantor Annuity Trust (GRAT) or Intentionally Defective Grantor Trust (IDGT) strategies will able to create more tax-efficient investment and estate strategies for their clients. Portfolio managers that manage tax-inefficient alternative asset strategies will be able to make their investment strategies more attractive to potential investors by encouraging them to invest in their strategy through the PPLI vehicle.

Improving after-tax, after-advisory fee returns by charging RIA fee on a pre-tax basis

| (A) | (B) | (C) = | (D) | (E)= *(C) | (F) | (G)= | |

|---|---|---|---|---|---|---|---|

| Choice of Fee Deduction | Gross Yield | Pre-Tax AUM fee | Taxable Gain on Yield | Tax-Rate on Taxable Yield | Client After-Tax Yield | After-Tax RIA AUM fee | Client After-Tax, After-Advisory Fee Bond Yield |

| Charging RIA fee after-taxes | 8.00% | 0.00% | 8.00% | 50.00% | 4.00% | 1.00% | 3.00% |

| Charging RIA fee pre-tax | 8.00% | 1.00% | 7.00% | 50.00% | 3.50% | 0.00% | 3.50% |

By charging their fee on a pre-tax basis from a retirement account instead of from an after-tax cash account, RIAs and portfolio managers can help clients reduce their taxable gain which of course reduces the taxes clients pay. This allows clients to keep more of the gross return of the investment on an after-tax and after-fee basis.

In the example above, the client gets to keep 50 basis points more of the gross return (14.2% more on a percentage basis) if the RIA is able to charge their fee for managing the assets on a pre-tax basis.

While PPLI is only available for qualified clients, traditional life insurance structures can be used for HNW clients who are not qualified purchasers to address the same fixed income issues in a rising interest rate and rising tax environment. For more information on how life insurance solutions can improve after-tax, after-advisory fee solutions for the fixed income portion of a client’s portfolio, feel free to read the articles below.

| Strategy | Fixed Income Solution | Retirement Account Similarity | Expected Rate of Return | Minimum Holding Period |

|---|---|---|---|---|

| No-commission annuities | Tax-deferred long-term bonds without interest rate risk | Traditional IRA | 2.25%-4% (tax-deferred) | 5-7 years |

| Whole Life Insurance | Tax-free long-term bonds without interest rate risk and with equity dividends | Roth IRA | 4.5%-5% (tax-free) | 15-20 years+ |

| Indexed Universal Life Insurance | Tax-free equity returns with cap and floor | Roth IRA | 4%-7% (tax-free) | 20 years+ |

| Life Settlements | Uncorrelated alternative asset in place of long-term bonds | None/Roth IRA with PPLI | 9%-11% (taxable) 9%-11%(tax-free with PPLI) | ~10 years |

Ready to transform your UHNW practices with PPLI?

Contact us to learn more.

Author

Learn how to evaluate PPLI carriers by balancing financial strength ratings against investment platform flexibility. Compare fee structures and long-term costs to select the optimal Private Placement Life Insurance carrier for your wealth strategy.

Determining the right death benefit level for your Private Placement Life Insurance (PPLI) policy is one of the most critical decisions that will impact your policy’s performance, costs, and overall effectiveness. This comprehensive guide explores how to balance regulatory requirements, estate planning needs, family protection goals, and investment capacity optimization to find the optimal death benefit level for your unique circumstances.

Master essential best practices for PPLI investment committee governance. Learn to establish effective oversight structures, develop robust policies, and implement risk management frameworks that maximize wealth preservation while ensuring regulatory compliance.

0 Comments