Whole Life Insurance as an Investment and Financial Planning Tool

Rajiv Rebello

Author

September 11, 2023

Author

For high income earners, a 4.5% after-tax return can be equivalent to an 8%+ pre-tax return. Whole life insurance can provide the same after-tax return of an investment with a higher pre-tax return-but without the higher investment risk.

There are usually only two types of people who talk about whole life insurance:

In this article, I’m going to use my expertise as an actuary to explain to you exactly how to use whole life insurance as a financial planning, investment, and retirement tool and why it has a plethora of benefits that you can’t find elsewhere.

I’m also going to explain why most people get burned by whole life insurance and how that actually benefits policyowners who understand how to properly use it for their financial planning goals.

Here are the key elements of whole life insurance you’ll be learning in this article:

The primary investment, retirement, and financial planning benefits of whole life insurance arise because it can provide a high after-tax, risk-adjusted return to those who structure it properly as a financial planning vehicle.

If you are a high income earner living in states with high income taxes like California, New York, New Jersey, etc, then it’s most likely that you are paying more than 40% of your earnings in federal and state income taxes.

Ordinary Income Tax- Rate in 2023 | Ordinary Income Tax-Rate (Federal and State) for State Residents | |

|---|---|---|

| 13.30% | 54.10% | |

| 10.75% | 51.70% | |

D.C. | 10.75% | 51.60% |

| Oregon | 9.90% | 51.60% |

| Minnesota | 9.85% | 50.70% |

| 9.00% | 50.70% | |

| New York | 10.90% | 49.80% |

Certain states assess high marginal tax rates on ordinary income (eg bond dividends)—in addition to the federal tax rate residents pay (top federal rate is 37% +3.8% Net Investment Income Surcharge). This means that high earning individuals in these states can end up paying more than 50% in federal and state taxes on their gains. |

High income earners who earn their income from high salaries or business revenues are often looking for safe places to invest their after-tax earnings since they are already taking significant risk either with their businesses or their equity portfolio.

Such individuals are trusting in their own earning potential, businesses, and equity portfolio to grow their wealth. They understand that while investing in these opportunities comes with significant risk, it also allows them the best opportunity for them to grow their wealth significantly.

But if these individuals are taking significant risk in growing their wealth with these opportunities, what is the best way for them to protect their wealth with the rest of their investments?

| Stocks, Private Businesses, Private Investments | |

| Bonds, Annuities, Whole Life |

Growth assets like stocks and private businesses typically have higher expected returns, but also higher risk, while safe assets have lower returns, but also lower risk. |

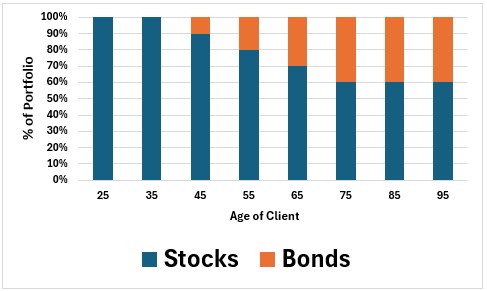

The traditional way for clients to do this is to increase the allocation of their portfolio to bond-like assets that are more stable than the risk they are taking with their other equity investments.

This is the same reason why advisors and target date funds increase the client’s asset allocation towards bonds as clients get older and closer to retirement when they will need the income from their portfolio and can’t take as much risk with their investments.

Over time, advisors and target date funds slowly shift the portfolio allocation from 100% stock allocation to a lower stock allocation and higher bond allocation in order to reduce risk in the portfolio as the client nears retirement. |

The problem with this is that while it’s easier for advisors and target date funds to allocate clients to bonds to reduce risk on a pre-tax basis, it doesn’t really make sense for high net worth clients on an after-tax basis. This is because on an after-tax basis the client is earning very little from the bond allocation and is still subject to large losses if interest rates rise—as evidenced by bond returns in 2022. This is especially pragmatic in retirement when clients are withdrawing funds to meet their income needs.

| 4% | 50% | 2% |

While safe assets like bonds have less risk, they also are exposed to high tax-rates leaving the client with very little on an after-tax basis. |

So the heavy allocation to taxable bonds is a solution that helps advisors and target date funds easily scale their business, but doesn’t actually provide better retirement solutions for high net worth clients.

Whole life insurance is a way for clients to get significantly higher after-tax returns and significantly less volatility by investing in long-term bonds without the heavy tax and interest rate risk exposure.

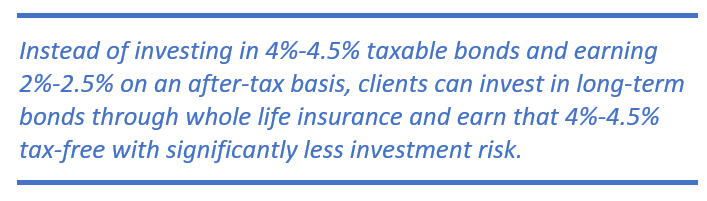

Instead of investing in 4%-4.5% taxable bonds and earning 2%-2.5% on an after-tax basis, clients can invest in long-term bonds through whole life insurance and earn that 4%-4.5% tax-free with significantly less investment risk. However we must remember that whole life is providing life insurance coverage as well. This is a benefit that investing in bonds doesn’t provide. When we subtract the cost of the life insurance coverage from the whole life premium, clients are getting a 5%-5.5% tax-free return on bonds by combining their life insurance coverage with their investment in tax-free bonds.

The key to doing this is to invest for the long-term and structure the investment properly. Doing this allows clients the ability to invest in safer assets that can have a higher after-tax risk-adjusted return than some of the growth assets they are investing in.

| 8% | 50% | 4% | |

| 4% | 0% | 4% |

While safe assets have lower pre-tax returns than growth assets, by protecting these assets from taxes, the assets can have the same after-tax return as growth assets but with significantly less investment risk. |

Whole life insurance is able to provide great after-tax returns with limited investment risk to policyowners who keep the policy due to the fact that not all policyowners are using the policy properly.

In other words, some policyowners get a great after-tax risk-adjusted return from a whole life insurance policy simply because other policyowners get a bad deal due to their poor decision making.

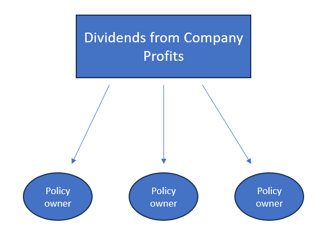

Whole life insurance allows policyowners who keep the policy the ability to invest in long-term bonds tax-free and without interest rate risk while also sharing in the company’s profits via dividend payments in the later years.

Below are the top two reasons why some policyowners who understand how to utilize whole life properly are able to get a great deal from the policy due to other policyowners who make poor decisions.

1) Policyowners who keep the policy for the long-term benefit from those who cancel the policy early

The most important thing for policyowners to realize when they purchase whole life insurance is that for them to benefit from the whole life policy they have to keep it for the long-term.

In fact, with whole life insurance the policyowners who keep the policy for the long-term are actually benefitting as a direct result of all the policyowners who buy the policy and then cancel it shortly thereafter.

What most policyowners don’t realize when they purchase a whole life insurance policy is that most policyowners cancel the policy. In fact, Society of Actuaries’ studies show that almost 50% of policyowners will cancel their policy within 10 years and nearly 70% of policyowners will cancel their policy all together.

Why is this bad for policyowners who cancel the policy?

Well, for starters, life insurance companies charge both heavy early expenses and surrender charges in the early years of the policy. Therefore, unless the policy is structured properly (see point 2 below), if the policy owner cancels the policy within the first 15 years of the policy, they will often lose money on their investment.

This is horrible for the policyowners who cancel the policy. These policyowners will end up spending tens to hundreds of thousands of dollars into an “investment” and walk away with almost nothing—and then die afterwards.

Which of course means that the life insurance company collected tens to hundreds of thousands of dollars in premiums without ever having to pay a death benefit!

While buying a whole life policy and then canceling it is horrible for policyowners who cancel the policy in the early years, this behavior is absolutely necessary for the policyowners who keep the policy in order to maximize the benefit they receive from the policy.

The IRRs of a poorly designed policy are negative for almost the first 15 years of the policy. While this is bad since more than 50% of policyowners will cancel the policy by that time, it is absolutely necessary in order for the policyowners who structure their policy properly to receive great returns in the later years of the policy . |

Why do policyowners who keep the policy for the long-term benefit from those who cancel in the early years?

Well, the reason for this is that mutual life insurance companies share their profits with policyowners who keep the policy in the later years through dividend payments made to policyowners. Since there are very few policyowners left in the later years, these policyowners who keep the policy are reaping ALL of the benefits that otherwise would have to be shared with the other policyowners who bought policies from that carrier.

In the later years, mutual whole life companies share profits with policyowners through the form of dividends. The less policyowners there are remaining, the larger the dividend each policyowner gets. This is why policyowners who keep the policy benefit from other policyowners canceling. |

Since the policyowners who keep the policy don’t have to share these dividend payments with the policyowners who canceled the policy, their returns are boosted at the expense of those who canceled.

The other reason why policyowners who keep the policy need other policyowners to cancel the policy is due to the amount of death benefit that the life insurance company provides to the policyowner if they pass away.

Since the life insurance company knows that ~70% of the policyowners will cancel the policy, they can afford to offer more death benefit relative to premium paid by the policyowner since they know most policyowners won’t keep the policy.

So similar to the dividend payment example I mentioned above, the policyowners who keep the policy don’t have to share the death benefit payouts that would have gone to the other policyowners who canceled the policy.

If all the policyowners kept the life insurance policy, then this wouldn’t be the case. Policyowners who keep the policy are often paying ~50% less in premiums for their policy than they would be required to pay if all of the policyowners kept their policy.

And as you can imagine, if policyowners had to pay twice the amount of premiums for a life insurance policy with a given death benefit, then the life insurance company would sell a lot less policies.

So the life insurance company’s entire distribution strategy is dependent on a large number of policyowners canceling the policy without the life insurance company having to pay a death benefit on these policies.

2) Policyowners who structure the policy to pay less commissions to the agent get a much higher return than those who pay higher commissions

Another critique made of whole life insurance policies is that the return on the policies is low, often in the 2%-3% range. But even this is a high after-tax return for high income policy earners who are paying 40%-50% plus in taxes every year and would otherwise be investing in bonds.

However, most whole life insurance policyowners don’t realize that they can improve the after-tax return of their policy to 4%-4.5% (equivalent to an 8%+ after-tax return for high income earners) simply by minimizing the commissions paid on the policy.

On top of this, whole life insurance is providing clients with death benefit coverage as well. So when we think of whole life insurance, the client is essentially buying long-term life insurance coverage and investing the difference in long-term bonds with downside protection. So if we were to think of whole life insurance as an investment vehicle, we would have to subtract the cost of the life insurance coverage here.

When we subtract the cost of the insurance that whole life insurance is providing, the return on the pure investment piece here is more like 5%-5.5%.

A typical whole life insurance policy pays 80%-100% of the first year premium to the life insurance agent who sold the policy. This is a huge expense for the life insurance company to bear. But the life insurance company has to do this in order to incentivize the insurance agents to sell the policy. As you can imagine, the life insurance company has to make this expense back someway. It does this through high early year expenses in the policy and high surrender charges for policyowners who cancel the policy (as described previously).

Policyowners can improve the return on the policy by reducing the commissions paid to the life insurance agent who sold the policy relative to the premium paid into the policy. They can do this by utilizing paid-up additions instead of traditional whole life insurance as I’ve talked about previously here.

Paid-up additions allow clients to dump large amount of premiums into the policy that have a low commission rate. Instead of 80%-100% of the first year premium amount being used to pay commissions, the commission rate on the paid-up addition portion of the policy is only 3%-5%.

Since the insurance company pays less commissions on the paid-up addition portion of the premiums than on the traditional whole life insurance premiums, the more the policyowner uses paid-up additions instead of traditional whole life insurance the less the expenses in the policy are and the higher the policyowner returns will be.

Maximizing the use of paid-up additions versus traditional whole life insurance premiums is the difference between earning a 2%-3% tax-free return versus a 4%-4.5% tax-free return.

However, very few policyowners use the paid-up additions feature in whole life policies properly.

Whole life insurance offers policyowners the ability to choose between two ideal financial planning scenarios:

1. Maximizing the tax-free IRR

2. Maximizing the tax-free distribution

These two goals are antagonistic to one another; the more you maximize one, the more you minimize the other.

In this section, I’ll show you how to do both depending on your goals.

1. Maximizing the Tax-Free IRR

In order to maximize the tax-free IRR, the client needs to maximize the use of paid-up additions and limit the withdrawals in the policy.

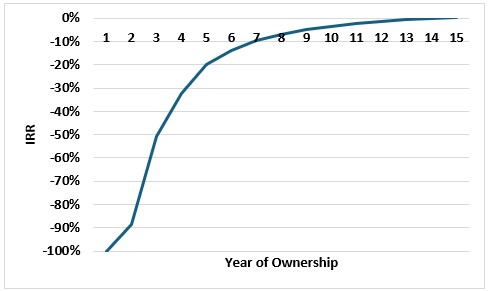

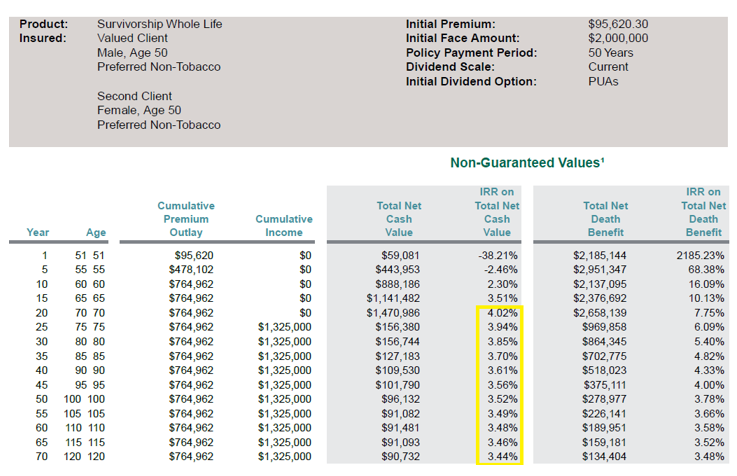

In the image below we can see the IRRs from a whole life policy illustration that is structured properly to earn a 4%-4.5% tax-free IRR on the cash value.

Whole life policy structured to earn 4%-4.5% tax-free

By properly structuring a whole life policy utilizing Paid-Up Additions, clients can earn a long-time tax-free IRR on their cash value of 4%-4.5%. |

The policy illustrated above pays $95,620 for 8 years (total cumulative premium of $764,920) and maximizes the use of paid-up additions which reduces the commissions paid on the policy.

At the end of the 8th year, the client stops paying premiums on the policy by utilizing the reduced paid-up feature. In year 21, the client takes out $375,417 (~26% of the total value of the policy) through a tax-free withdrawal to help with their retirement needs.

Note, however, that if the policyowner cancels the policy before year 5, they will actually lose money on the transaction (-2.30% IRR). Hence, the 4%-4.5% is only actually earned by policyowners who keep the policy for 20+ years.

In the above example we see that the tax-free IRR on Total Net Cash Value is 4.02% after 20 years, and 4.5% after 40 years.

For those wishing to see the full illustration, you can access it here.

Note that the client can take out more of their value in tax-free withdrawals and loans (~90% of their value) if they wish. However, doing so will reduce future returns due to the drag of the loan as well as reduced dividend payments as we’ll see in the following section.

2. Maximizing the Tax-Free Distribution

While maximizing the tax-free IRR may be a goal of the client, another goal may be to maximize the tax-free distributions the client can take out of the policy. This is particularly advantageous if the client is planning for retirement as we’ll see in the next section.

In the illustration below, the client still pays $95,620 for 8 years into the policy (total cumulative premium of $764,920).

However, in year 21 the client takes out 90% of their policy value ($1,325,000) instead of 26% of the policy value in the previous example.

As seen below, the tax-free IRR after 20 years is 4.02% just like it was in the previous example. However, it starts to decrease after that for the reasons mentioned above.

By taking out the maximum tax-free distributions possible, the tax-free IRR drops to 3.61% after 40 years here compared to 4.5% in the previous example. So maximizing the tax-free distributions hurts the client’s IRR in the policy.

Whole life policy structured to utilize Paid-Up Additions with Maximum Distribution

Clients can take out up to 90% of their policy value via tax-free withdrawals and loans. Doing so, however, will diminish future returns. |

So as discussed previously, maximizing the tax-free distribution hurts the IRR of the policy, but does allow for greater tax-efficient retirement planning as we’ll see in the retirement planning section later in this article.

For those wishing to see the full illustration, you can access it here

While one key benefit of whole life insurance for policyowners is that it provides higher after-tax returns than bonds as shown in the previous sections, another large advantage of whole life insurance is that it is less risky than investing in bonds as well.

The reason why whole life insurance has less investment risk than long-term bonds is for the following three reasons:

1. Protection from Interest Rate Risk

Interest rate risk is what adds risk to bond investing. If interest rates rise, then bonds will take heavy losses. The coupon payments of bonds on the other hand are fairly stable as indicated by the table below.

Bond Returns and Standard Deviations from 1928-2022

| Returns | Standard Deviation | |||||

|---|---|---|---|---|---|---|

Return IRR | Return IRR | Return IRR | Return Standard Deviation | Return Standard Deviation | Return Standard Deviation | |

Corporate Bond | 6.68% | -0.11% | 6.80% | 7.75% | 6.65% | 2.93% |

Source: Damodaran, Fed Reserve

Since 1928, the entirety of bond returns have been driven by the dividend return of bonds and not the price return. Furthermore, the price return is significantly more volatile than the dividend return of the bond. |

As the table above shows, the entirety of the bond return over the past 95 years has been driven by the dividend return of bonds (6.80%) as opposed to the price return of bonds (-0.11%). Furthermore it is the price return of the bond that is driving the volatility here (6.65% standard deviation of the price return of the bond as opposed to 2.93% standard deviation of the dividend return).

The point being here is that when advisors talk about using bonds for safety, it’s purely the dividend return that is providing the safety—not the price return. The price return of the bond is actually adding risk here.

In order to capture the safety of the coupon payments of bonds in comparison to the risk associated with the price return of bonds due to rising interest rates, many advisors will invest in bond ladders in which advisors buy and hold bonds of varying maturities. That way they can just hold the bond to maturity and not have to worry about the embedded interest rate risk that comes with investing in bond funds.

The downside of this approach, of course, is that any attempt to exit the investment prior to maturity will expose the client to the same interest rate risk they were trying to avoid. Using bond ladders is truly a long-term retirement approach that requires the investor to have a long-term investment horizon with preplanned liquidity needs. Furthermore, the utility of this bond ladder approach is minimized since the coupon payments are taxed at high ordinary income rates.

The reason why advisors use bond ladders is because they realize the best use of bonds for downside protection in retirement is to capture the safety of the dividend return of bonds while not taking on the risk of the price return portion of bonds.

This is exactly what insurance products like whole life insurance do while providing tax-free benefits and liquidity provisions to policyowners as well. Yes, it requires investors to have a long-term retirement approach, but the use of bond ladders or any other retirement plan requires the same approach.

Whole life insurance allows investors to invest in long-term bonds similar to bond ladders except with more tax-advantageous liquidity provisions and benefits. Remember that when policyowners purchase whole life insurance policies they are essentially investing in the underlying general account of the life insurance company which are primarily invested in long-term bonds with an added bonus of profit sharing in the later years via dividend payments.

Each year that the policyowner makes a premium, the policyowner is essentially buying a part of the insurance company’s general account portfolio which primarily consists of investment grade long-term bonds. Ninety-five percent of these long-term bonds are investment grade.

Percentage Holdings of General Account Portfolio of Life Insurance Company

Source: ACLI

The general account portfolio of a life insurance company primarily consists of long-term bonds. 95% of these are investment grade long-term bonds. Every time a policyowner makes a premium payment, they are making an investment into this long-term bond portfolio so that they can the proceeds tax-free and without taking the interest rate risk that is associated with investing in long-term bonds. |

The insurance company has long-term liabilities, so for the most part are trying to buy long-term buy and hold assets to match these liabilities. Any interest rate risk here is born by the insurance company because they have a long-term horizon and can afford to hold bonds for the long-term whereas the individual investor does not have the same investment horizon.

As we saw in Table 1, the yield rates on long-term bonds have been amazingly stable over the last 100 years. So the pure coupon rate here is very stable over the long-term even if interest rates change over the short term. So even if interest rates change in the short term, the effect of that short-term change on Whole Life returns will be small relative to if the client were invested in the underlying long-term bonds directly since the insurance company is bearing the full weight of the change in market value of the bonds.

This means that if interest rates rise in the short-term, whole life investors will not see a large loss in their long-term whole life returns whereas if they held the bonds directly, these policyowners would see a large upfront loss in market value. The opposite is also true however. If interest rates drop, whole life investors won’t see a large increase in their long-term returns, whereas if they held the bonds directly they would have experienced a large short-term gain in the upfront market value of their investment.

Therefore, investing in long-term bonds via a whole life insurance policy allows the returns to be tax-free and for significantly less volatility in their bond portfolio since the insurance company is the one holding the bonds to maturity while allowing the client to take money out of the investment prior to maturity and keep the coupon payments.

In fact, clients can take out 70%-90% of principal and gains tax-free via a combination of withdrawals and tax-free loans.

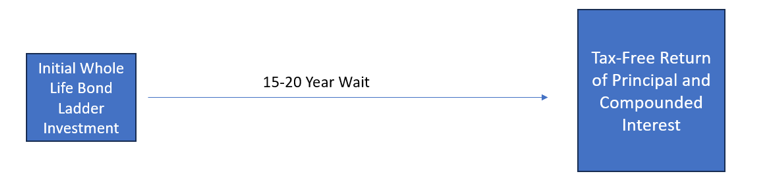

So we can think of investments into a whole life insurance policy similar to a bond ladder strategy.

The key difference here is that instead of a taxable coupon paying bond every 6 months to a year, with whole life you are investing in the equivalent of a zero coupon bond in which you invest via a premium payment to the insurance company during your working years when you’re in a high tax bracket and get the principal and compounded interest tax-free at the end of 15-20 years when you are in retirement.

Traditional Taxable Bond Ladder

With a traditional bond ladder, you make an initial investment, receive yearly or semi-annual coupon payments that are taxable, and at the end of 5-20 years you receive a tax-free return of principal. |

Whole Life Bond Ladder Approach

With Whole Life you are making the initial investment during your working years when you are in a high tax bracket and letting the interest compound tax-free and then waiting 15-20 years to withdraw the principal and interest tax-free |

So whole life insurance is providing reduced volatility versus investing in long-term bonds directly via a bond ladder while also providing higher after-tax returns and more tax-efficient liquidity provisions than would otherwise be possible for a high income tax earner during their working years.

2. Mortality Expectations

Another key driver of whole life returns are mortality expectations versus actual observed mortality. In other words, how many people who purchased whole life insurance policies actually died in a given year versus how many people the insurance company expected to die in a given year.

As you can imagine, if more people die in a given year than the insurance company expected that means the insurance company is losing money.

However, insurance companies and their actuaries are excellent at estimating mortality based on their past experience with these products. In fact, most insurance companies tout actual to expected mortality ratios of 90%+.

So similar to long-term coupon rates, the volatility around mortality is low and rarely sways whole life returns significantly.

3. Lapse Expectations

As discussed previously, the entire mechanism of whole life insurance is dependent on a large amount of people canceling the policy. If less people canceled the policy, then insurance companies would have to increase their reserves so they could pay future death benefits and it would make the product less profitable for the insurance company.

Luckily for the insurance company, policyowners are very consistent in canceling the policy. When an individual policyholder purchases a policy, the insurance company doesn’t know with certainty that that individual policyowner will cancel the policy. But they do know with a high level of confidence that on average a large amount of people will cancel their policies and that amount will be very close to what they expected.

It is the stability of insurance company’s investment, mortality, and lapse expectations that allow actuaries to be able to build these types of life insurance products to begin with. If these expectations were extremely volatile, it would be too difficult to design a profitable product around it without extremely high profit margins that would make the product unsellable.

By building a product around stable assumptions, the insurance company is able to generate a product with stable profits and share some of those profits with policyowners who keep the policy so that they also receive stable long-term after-tax returns.

The only people who are losing in this equation are the large amount of policyowners who cancel the policy or structure it poorly. And unfortunately the people who structure it poorly and/or cancel it end up being people from lower income brackets who don’t understand the product that was sold to them or can’t afford it anymore. On the other hand, wealthy people who buy larger face amount policies tend to be the ones who keep these policies for their investment and estate benefits and benefit from the poorer policyowners who cancel it.

It’s yet another form of income inequality in which wealthy individuals capitalize and benefit from the economic loss experienced by middle class policyowners who are sold products they don’t understand.

But if you’re an advisor to wealthy clients, this is an arbitrage opportunity that can’t be easily replicated in the investment world.

With whole life insurance, clients are getting stable long-term after-tax returns with limited volatility.

With whole life insurance, high net worth clients are getting better risk-adjusted after-tax returns and downside protection than they could get investing directly in taxable bonds.

This is of significant advantage to high net worth individuals who are phased out of contributing to traditional retirement plans and would be forced to invest in bonds via taxable accounts in order to try and protect against downside risk.

In a previous article, we’ve talked about how the rebalancing away from the equity portfolio towards the bond portfolio doesn’t make sense for high net worth clients because the portfolio is being shifted away from higher earning, tax-efficient equity investments into lower-earning, tax-inefficient bonds.

Instead of clients rebalancing away from stocks into bonds as clients get older—thereby experiencing tax drag from the constant buying and selling of assets—clients can slowly increase the percentage allocation of the portfolio into whole life by paying yearly annual premiums into the policy instead of investing in the equity markets in later years.

By the time they retire, instead of a 70% equity/30% bond portfolio, the client will have a 70% equity/30% whole life portfolio. This portfolio will be both higher earning and less risky on an after-tax basis than the 70% equity/30% bond portfolio.

The example above shows a client using a 70% equity/30% whole life portfolio instead of a 70% equity/30% bond portfolio. By using whole life insurance instead of bonds for downside protection, clients can achieve a higher after-tax and risk adjusted return. Instead of rebalancing the portfolio by selling stocks and buying bonds which exposes the client to tax drag, the client can simply slowly start paying the whole life premiums each year as the client gets closer to retirement. This will eventually turn the 100% equity portfolio into a 70% equity/30% whole life insurance portfolio. |

Another huge value of utilizing whole life in retirement is that the tax-free income it provides helps reduce the effective tax-rate that clients would pay on their taxable gains. Since the tax-rate that people pay increases as their income increases, and since whole life distributions are not included in taxable income, retirees can use tax-free whole life distributions in retirement to meet their retirement income goals while also reducing the percentage of their income that retirees are losing to taxes.

Let’s consider the case of a married couple both aged 65 in California who need $200,000 in after-tax retirement income. If this is taxed at ordinary income, then this married couple will have to withdraw $260,000 just to have $200,000 in after-tax income. The client is losing 23.1% of their income to taxes.

However, if the client is able to withdraw $150,000 in tax-free retirement income from their whole life policy, then they will only need an additional $50,000 in after-tax income to meet their $200,000 after-tax retirement income goal. In order to get this after-tax income of $50,000 the client will need $54,000 in taxable income. In otherwords, the client will only lose $4,000 in taxes on this $54,000 of taxable income. In this case the client is only losing 7.4% of their income to taxes.

The client is reducing the percentage of taxable income that is being lost to taxes by 15.7% (23.1% to 7.4%) by using tax-free whole life distributions.

Whole Life | Whole Life | |

Income Needed | $200,000 | $200,000 |

Withdrawals | $0 | $150,000 |

to Meet Retirement Goal | $260,000 | $54,000 |

Taxable Income | ($60,000) | ($4,000) |

| 23.1% | 7.4% |

By utilizing tax-free whole life distributions to partially meet their $200,000 of after-tax income, the retiree is able to reduce the percentage of their taxable income lost to taxes from 23.1% to 7.4% |

1) Reduces the total amount of withdrawals needed from the portfolio:

Reducing the tax-rate on withdrawals from the portfolio means less drag on the portfolio since less has to be withdrawn from the portfolio to pay taxes. This allows for the client to take more in withdrawals each year than would otherwise be possible if the client was at a higher tax-rate.

2) Allows for more financial tax-planning:

Reducing the client’s effective tax-rate and taxable income in retirement via tax-free whole life withdrawals increases the value of financial planning techniques such as Roth conversions as well as the ability to liquidate long-term capital gains at 0% taxation.

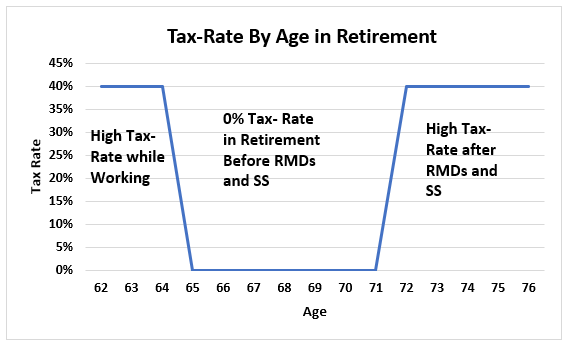

When clients are working their tax-rate is high, but after they retire they have no taxable income and a 0% tax-rate. They can use this window before they start taking Required Minimum Distributions (RMDs) and Social Security (SS) to implement smart financial planning strategies like Roth conversions and liquidating capital gains at 0%. In the above graph, the client is working until age 65 which reduces the clients tax rate to 0%. This creates a financial planning window for the client to implement smart financial planning strategies until age 70 when they start receiving taxable income again through RMDs and Social Security |

In the above chart, we can see that there is a financial planning window where the client is in a 0% tax-bracket in between the time the client retires and in-between the time they start taking required minimum distributions and social security.

By using tax-free whole life distributions during this time, clients can receive the income they need to pay their expenses while maximizing the use of this window to do either Roth conversions or take out income from their investment portfolio at a 0% capital gains tax-rate.

Since whole life makes more quantitative sense for high net worth individuals saving for retirement than taxable bonds, you might wonder why more financial advisors aren’t using it.

Well, there is a huge conflict of interest here.

Advisors who charge an asset under management fee are not going to recommend whole life insurance—even if it is in the best interest of their client—because doing so would take assets away from them which would decrease their fee.

The same goes with advisors who don’t earn an AUM fee, but have no idea how to use whole life as a financial planning and retirement tool and have no incentive to learn.

Advisors who earn a commission instead of an AUM fee are more than happy to sell clients whole life insurance and earn a commission. The problem here is that these advisors are going to sell the high commission whole life insurance product that earns 2% to 3% instead of the low commission whole life product that will earn the client 4%-4.5% on an after-tax basis. And what’s worse, the clients who purchase the product from these advisors will probably end up canceling the product because they were sold it instead of understanding how to use it from an investment and financial planning perspective—thereby defeating any tax benefits the product would have had for them.

Whole life can help provide better diversification, risk-adjusted, and tax-efficient returns than taxable bonds for high net worth clients as well as a wealth of tax-efficient financial planning strategies for those who are planning for retirement

The difficulty is finding an advisor who is willing to work in your best interest to create a solution that benefits you instead of his or her business interests.

Author

Discover how Private Placement Life Insurance transforms charitable remainder trust strategies into powerful wealth replacement tools. Learn tax-efficient approaches that maximize charitable benefits while preserving family wealth for high-net-worth families.

This blog post explores essential PPLI due diligence steps, covering carrier evaluation, regulatory considerations, investment platforms, tax compliance, and advisor expertise to help high-net-worth individuals make informed decisions before implementing this specialized insurance solution.

Discover how PPLI enhances business succession planning through key person insurance and buy-sell funding. Learn private placement life insurance strategies for business owners.

0 Comments