How Low Commission Life Insurance Products Maximize Returns

Rajiv Rebello

Author

August 28, 2017

Author

By now we all now the problems with permanent life insurance: low returns and high premium costs.

However, these poor returns are largely due to the large commissions paid to agents who sell these policies. In our previous post (see here) we discussed how most life insurance products impose high surrender charges on policy owners if they cancel the policy. They do this in an attempt to recoup the high costs associated with paying the life insurance agent 80% to 100% of the first-year premium. The policy owner ends up paying the price for the agent’s compensation when they cancel the policy and get very little back.

With low commission products on the other hand, the carrier is not obligated to pay the agent such a large amount upfront. As a result, they can afford to reduce/eliminate surrender charges and offer policy owners significantly higher cash accumulation and surrender values. Doing this significantly increases the return on the product as illustrated in the table and chart below.

In our next post we’ll show you how to properly fund the low commission life insurance product to maximize returns.

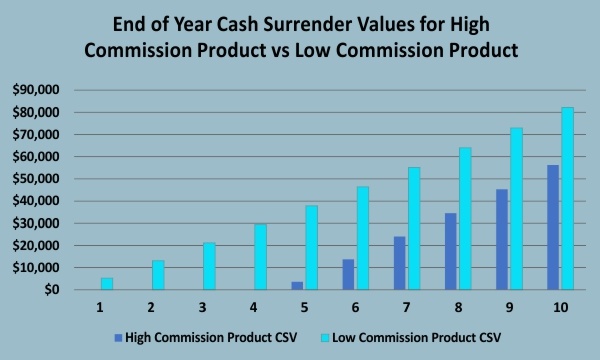

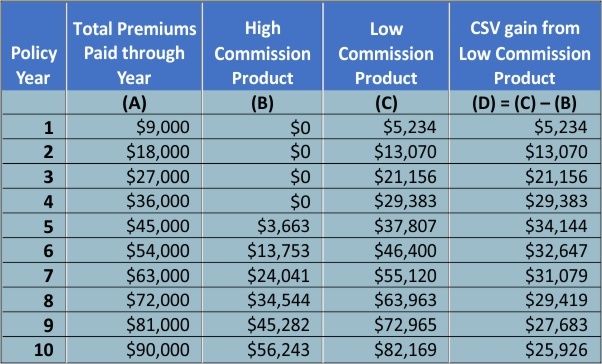

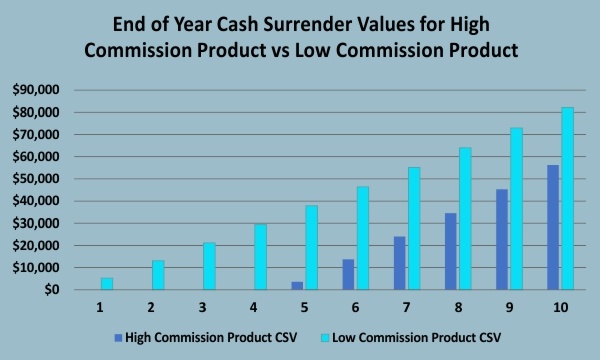

High commission vs low commission product cash surrender values:

The table above compares the end of year cash surrender values for a high commission product vs a low commission product on a 45 year-old male with a $1M death benefit. Both policies pay $9,000 a year into the policy. The high commission product pays the agent 100% of the first year premium while the low commission product pays the agent only 8% of the first year premium as an upfront commission and then pays a small percentage of the cash surrender value in each subsequent year.

By reducing upfront commissions and increasing back-end ones, the low commission product is able to better align incentives between agents and policy owners. With the high commission product, the agent gets paid a high upfront commission in year one that he gets to keep even if the policy owner cancels the policy in subsequent years. In order to recoup their expenses upon cancellation, the life insurance company then has to assess high surrender charges that result in minimal cash surrender values being offered to the policy owner if they cancel the product.

With the low commission product, the agent is incentivized by back-end commissions to sell the product to policy owners who will keep the product for the long-term. And since the upfront commission is low, the life insurance company doesn’t have to charge excessive surrender charges if the policy owner cancels. As a result, the policy owner gets a product with higher cash value accumulation in the product. At the end of 10 years this amounts to a $25,926 gain in cash surrender value for a policy owner who purchases a low commission product as opposed to a high commission one.

Low commission vs high commission CSVs:

The chart above shows the end of year cash surrender values for a $1M policy on a 45 year-old for both a high commission life insurance product and a low commission life insurance product from top rated life insurance companies.

Both products pay $9,000/year into their respective policies. However, the high commission product has to assess high surrender charges in order to recoup the high commissions they paid in the first year to the agent. As a result, the cash surrender values are significantly lower than that of the low commission product. At the end of 10 years, a policy owner who purchases a high commission product over a low commission one will lose $25,926 in cash surrender value.

Author

Learn how to evaluate PPLI carriers by balancing financial strength ratings against investment platform flexibility. Compare fee structures and long-term costs to select the optimal Private Placement Life Insurance carrier for your wealth strategy.

Determining the right death benefit level for your Private Placement Life Insurance (PPLI) policy is one of the most critical decisions that will impact your policy’s performance, costs, and overall effectiveness. This comprehensive guide explores how to balance regulatory requirements, estate planning needs, family protection goals, and investment capacity optimization to find the optimal death benefit level for your unique circumstances.

Master essential best practices for PPLI investment committee governance. Learn to establish effective oversight structures, develop robust policies, and implement risk management frameworks that maximize wealth preservation while ensuring regulatory compliance.

0 Comments