Annuities for Conservative HNW Clients Over Traditional Bond Investing

Rajiv Rebello

Author

August 10, 2018

Author

With equity markets at all-time highs and in the face of increasing interest rates, the current economic environment makes providing financial advice for conservative investors a catch 22 proposition. Should financial advisors recommend that risk-averse clients fearing a market downturn take a more bond-heavy portfolio allocation approach knowing that rising interest rates and subsequent rebalancing will pull the yields of such bond-heavy portfolios down?

This is of particular concern for middle age investors who choose to be less aggressive in their portfolio allocations as they near retirement. Being overly conservative at 55 to 60 years old, however, isn’t the most prudent thing to do. The individual will still have a good 25 to 30 years left to live and the lost opportunity cost by being overly conservative during that time period can be significant. Nevertheless, the psychological desire for that conservative client to protect the retirement nest egg that they have been slowly building over the past 25 to 30 years remains and can be difficult for a financial advisor to overcome with rational advice.

But what alternative options do financial advisors of such clients have than to advocate for a heavier portfolio allocation to bonds–particularly long-term corporate bonds?

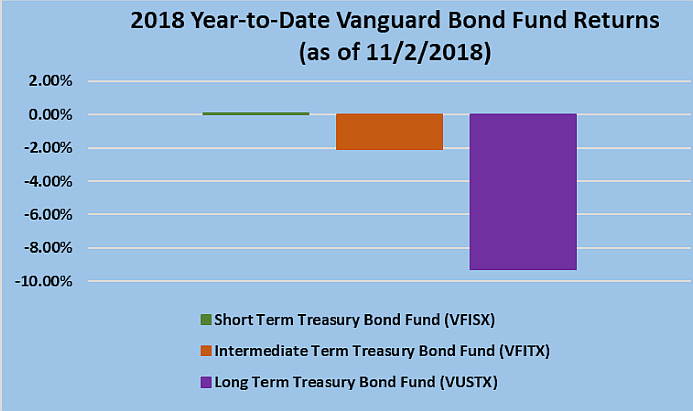

2018 Bond Fund Losses:

While bond funds pay a dividend to investors, the total return on intermediate and long term bond funds have been negative in 2018. This is due to the Fed’s decision to increase interest rates which results in bond funds taking a loss when bonds in the portfolio are sold. Longer duration bond funds (which conservative investors prefer) take the biggest hit in a rising interest rate environment.

As interest rates continue to rise, conservative investors investing in long term bond funds can expect to see similar losses.

Annuities have long been proposed by agents as a means to solve this dilemma of clients who want to grow their retirement nest egg while either protecting principal or providing tax-deferred growth that traditional bond investing won’t provide. Unfortunately annuities have often been associated with high fees that reduce the viability of these products for clients seeking to reduce market or interest rate risk. These high fees (either implicit or explicit) were often a necessity for the insurance companies as a means to counter the high commissions being paid to agents selling these products.

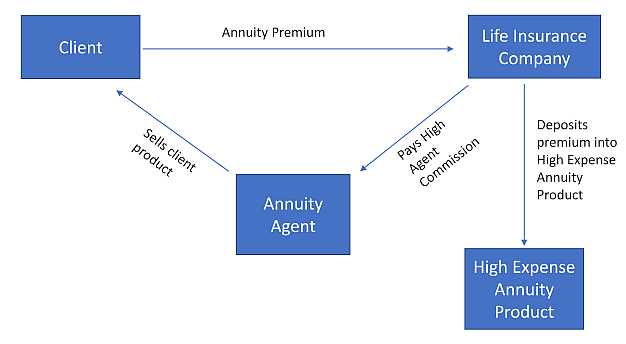

Typical annuity structure:

The typical annuity structure heavily relies on the annuity agent to build networks and relationships with RIAs and clients

The proposed DOL Fiduciary rule aimed to make sellers of these products that were also providing investment advice to clients disclose all conflicts of interest. This of course made it difficult for agents/financial advisors to justify recommending that a client purchase a poor performing annuity product that would earn the agent/financial advisor a high commission.

This forced insurance companies to rethink how they would design and market their products in order to comply with the rule. The idea at the time was that life insurance companies would be forced to reduce or eliminate the commissions they offered to agents to sell their products in order to mitigate sales conflicts, which would have the added benefit of allowing insurance company actuaries the ability to create products that provided better performance (via lower costs) to clients. .

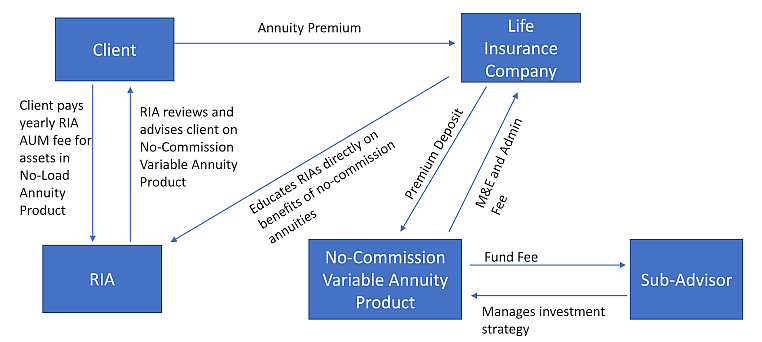

And this, in fact, is largely what has happened. Several insurance companies have created what’s known as “no-commission” or fee-based annuities that pay no commissions on the product. Instead of utilizing high commission individual agents as their distribution channel, insurance companies are either marketing their products directly to RIAs—or using annuity wholesalers to do so at a fraction of the cost of traditional annuity agent commission distribution costs.

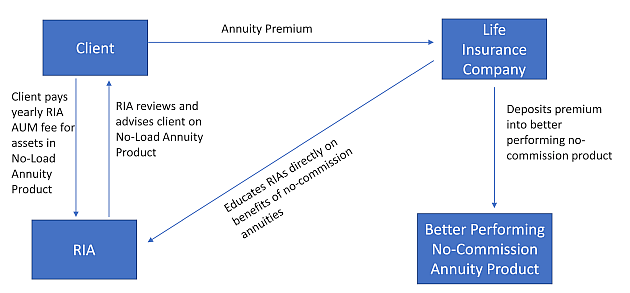

No-Commission Annuity Structure:

By eliminating commissions the no-commission annuity is able to significantly reduce expenses and offer clients better performing products. However this structure bypasses the agent and relies on directly educating RIAs about the value these products offer to both the RIAs and their clients.

This type of model has long term benefits for both the client and the RIA. The first is that the RIA is able to offer their clients a higher performing product that will better match their clients needs. The ancillary benefit is that these RIAs can then include the assets in these no-commission products as part of their overall assets under management and still earn their yearly AUM fee which will grow just as the assets in the better performing product grow.

This type of product fits right in-line with the increasing trend of financial advisors who are limiting or dropping the commission part of their practice for the sake of focusing on building their AUM fee-based model instead.

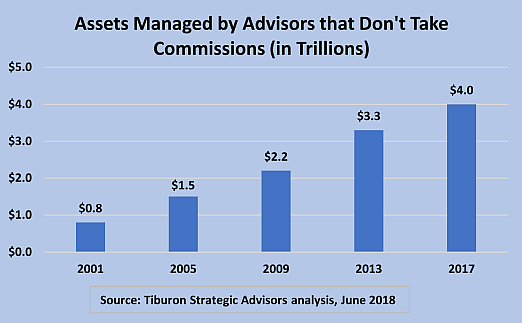

Financial Advisors are increasingly not taking commissions:

Since the early 2000s financial advisors have eschewed commission-based business for the purpose of building up their fee-based business.

From an economic standpoint this makes sense for most advisors. It’s much easier to build up a base of client assets to earn a percentage fee on each year than to build a practice that depends on the advisor finding new clients each year to sell commission-based products to. Advisors that build a fee-based practice can earn a hefty income on existing client assets without the need to find new clients. Advisors that are primarily commission-based on the other hand must find new clients every year to sell products to otherwise their yearly revenue will quickly dry up.

Nevertheless, the shift from a commission-based business to a fee-based financial business presents a predicament for commission-based financial advisors who built up their practice on backs of commission based insurance products like life insurance and annuities and as a result have accrued a wealth of knowledge and understanding of these commission-based products they are now forced to leave behind as they focus on building their fee-based services. However, the introduction of no-commission based products—both life insurance and annuity products—offers a significantly better middle ground for both the former commission-based advisor and his or her clients. The former commission-based advisor gets to continue to utilize his specialized skillset and experience with these products and his clients ultimately get better products and higher returns.

As clients seek more protection at a time of all-time market highs, indexed annuities are expected to see 5% to 10% growth over the next few years with fixed-rate deferred annuities expected to see growth as high as 25% year over year. However, only a fraction of these are no-commission products which would be the best for the consumer. This means that there is an excellent opportunity for fiduciary fee-only financial advisors to educate their clients about these products while getting compensated for their fiduciary expertise. Financial advisors are often weary about utilizing annuities because they feel they will be giving up control of the client’s assets to the insurance company. But the fact is that the no-commission indexed annuities often use the same or similar indices that the advisor is using outside of the annuity and collecting his or her fees on already. The significant difference is that these indices are placed within an annuity for the purpose of the tax-deferral benefit.

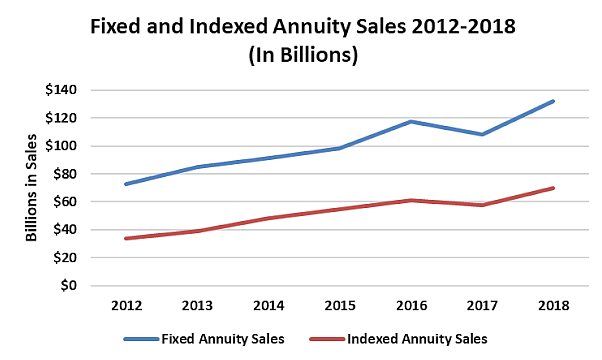

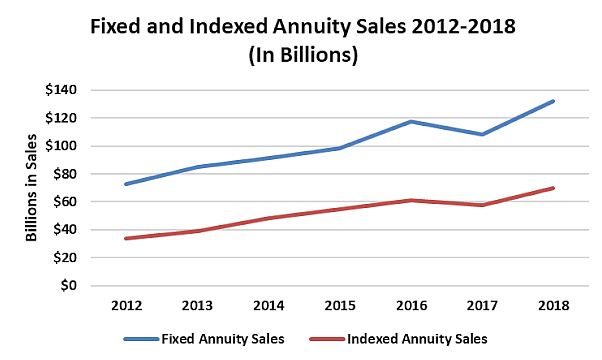

Growth of Fixed and Indexed Annuities:

Over the past few years sales of fixed and indexed annuities have soared as investors seek the comfort of principal protection and potential upside that these products provide. In the face of all-time market highs and worries about volatility this trend will continue with LIMRA projecting that indexed annuities will grow by 40% by 2023. No-commission fixed and indexed annuities therefore afford a unique opportunity for fee-only financial advisors to capture a part of this growing market and increase either their AUM or financial planning fees

While it’s clear that these no-load products would perform better than their high-commission counterparts, do they provide a better alternative to typical bond investing that is highly utilized by financial advisors in recommending portfolio allocations to their more conservative clients?

In this article we will take no-commission fixed annuity, index annuity, and variable annuity products and compare the after-tax results to that of a traditional bond portfolio to see if financial advisors should start to consider utilizing these products as part of their financial practice.

Advisors applying Modern Portfolio Theory use the theory to design portfolios intended to provide the maximum return for a given amount of risk (or the minimum risk for a given level of expected return), as all else being equal, increasing volatility hurts long-term returns (a phenomenon known as volatility drag).

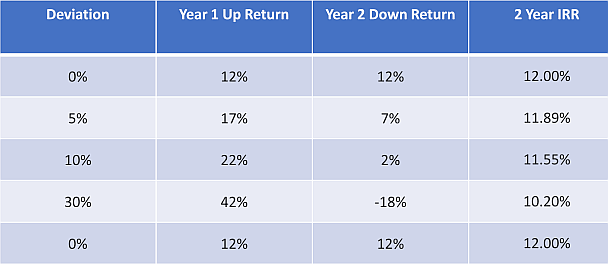

Consider four different funds all having the same expected annual return of 12%, but with 3 different volatilities. One fund has no volatility (12% annual return in all years), the second fund can fluctuate by 5% in any one year, the third can fluctuate by 10% in any one year and the fourth can fluctuate by 30% in any one year. Even though all four funds have the same expected annual return, the long-term compound return is significantly reduced with increasing volatility.

This is why the mean annual return for the S&P 500 is around 12%, but the mean compound long-term return is only around 10%.

Long-term impact of volatility:

As the volatility of yearly returns increase, long-term returns suffer even if the mean annual return is the same

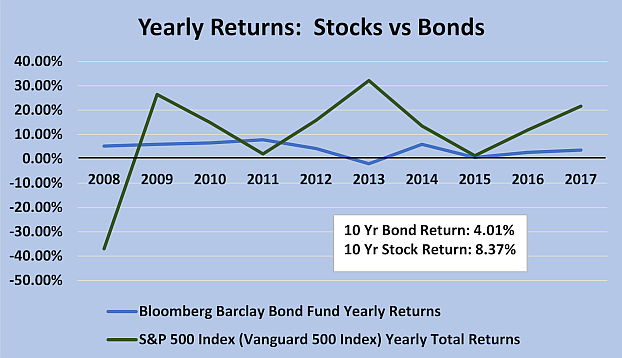

Historically bond investing of intermediate duration has not been nearly as volatile as equity investing. As a result, investors look to reduce volatility often increase their bond allocations even though this often comes with reduced long-term returns. Historical results over the past 10 years have been in alignment with this premise:

2008-2017 Intermediate Duration Bond Funds vs S&P 500 Total Returns:

Stock investing typically involves both higher returns and higher volatility. More conservative investors fearing the up and down swings of the equity market often prefer the lower-earning, but more stable bond portfolio

While bond investing can offer lower returns in exchange for lower volatility, it often also comes with severe tax-disadvantages when compared with equity investing.

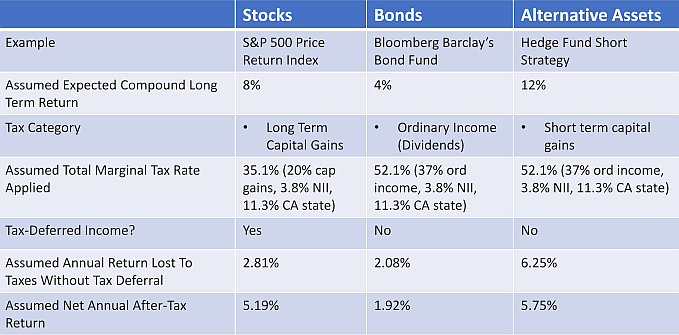

The first key disadvantage of bond investing in relation to stocks is due to the rate that their respective gains are taxed at. Stocks held for over a year are taxed at long-term capital gains rates which have a max federal tax rate of 20% (plus a 3.8% Medicare surtax). Qualified stock dividends are also taxed at a max rate of 20% (plus the 3.8% Medicare surtax). By contrast, bond interest is taxed at a top tax bracket of 37%. (Of course, state income taxes apply on top of both, where applicable.)

The other disadvantage of bonds is that they lack the tax-deferral on gains afforded to stock investing. Stock investors can purchase equities, have the stock appreciate, and only pay capital gains taxes on the appreciation at the time they liquidate and sell the stock. This allows for their investment to grow tax-deferred in the interim. Bonds, on the other hand, typically pay interest every year (taxed again at the ordinary income rates of the bondholder).

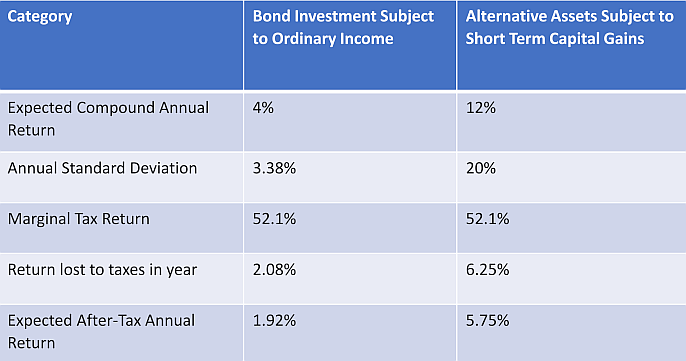

Besides bonds, alternative assets that are not correlated to traditional equity markets are another asset class has been used by financial advisors and their clients as a means to reduce volatility in stock portfolios. However, alternative assets subject to short-term capital gains (hedge fund strategies, commodities trading, etc) suffer from the same tax-inefficiencies that bonds do.

Tax Inefficiencies of Bonds and Alternative Assets in Comparison with Stocks:

While both bonds and uncorrelated alternative assets allow portfolio managers to reduce the overall volatility of an equity only portfolio, they are severely tax-inefficient for high income earners in comparison with the long-term capital gains treatment of stock investments. Bonds have lower expected returns than stocks while also having a larger percent of those returns lost due to taxes. While alternative assets subject to short term capital gains can in theory have higher returns than traditional long-term equity investing, a significant percentage of any additional gain will be lost due to the higher tax treatment of such short-term equity strategies.

Investors looking to diversify their equity portfolio into bonds or alternative assets subject to short term capital gains face significant tax drawbacks for doing so. Are there better options for conservative investors looking to diversify their holdings in order to reduce volatility than to accept these tradeoffs for the sake of attempting to protect principal? For assets that are subject to high taxation, is deferring taxes a better option?

Annuities offer investors the ability to deposit a large amount of money with an insurance company and allow that amount to grow tax-deferred until the investor wants to withdraw the money. While the annuity companies invest these funds in the same long-term investment grade bonds that can be found outside the annuity, fiduciary financial advisors have typically rallied against the use of annuities for a few notable reasons:

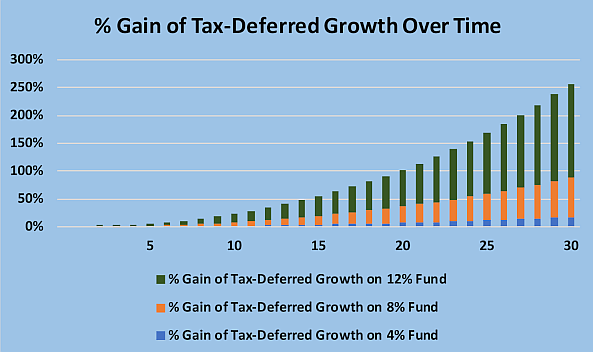

1) The benefits of tax-deferred growth are only valuable over the long-term, and depend heavily on the underlying earning rate of the investment being tax-deferred and the amount of marginal tax rate that is being tax-deferred. In other words, an investor subject to a 50% marginal tax rate and generating a 12%/year return would receive much larger tax-deferred benefits than an investor subject to a 25% marginal tax rate and investing for a 4% return.

Benefits of tax-deferred growth increase with higher yielding assets:

The above graph shows the percent gain of a tax-deferred strategy for three funds with different earning rate assumptions. All three funds are assumed to be taxed at the same 50% marginal tax rate. While tax-deferred growth on a 4% fund offers only a 17% gain after 30 years, tax-deferral on a 12% fund results in more than a 250% gain over that same time period.

2) Any benefits that tax-deferred growth may have conferred were often negated by the high expenses associated with these products.

While historical annuities offered significant expenses and surrender charges—necessitated by the high agent commissions—no-load annuities offer lower surrender charges and more competitive products. But how do these better performing annuities compare to the tried and true method of bond investing for lowering volatility? And how do their expected returns compare?

In order to answer those questions, we first need to look at the value proposition of the three main types of annuities and see how they can be best used by investment advisors.

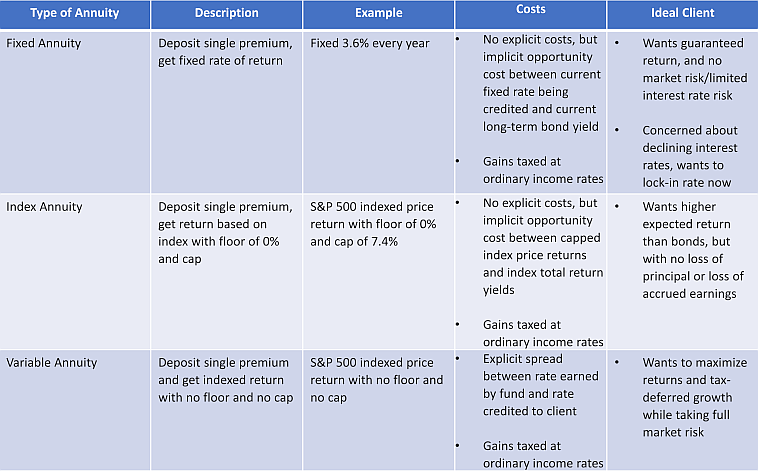

There are three main types of annuities: fixed annuities, index annuities, and variable annuities.

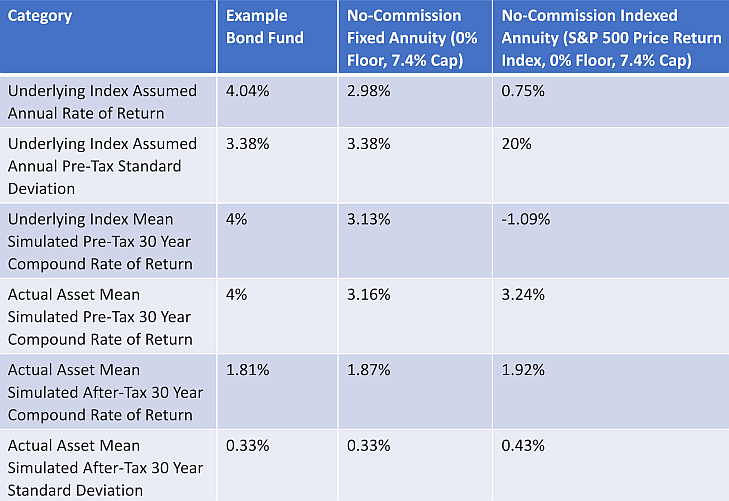

An overview of the three types are shown in the table below. All rates and caps used are examples taken from current no-load annuities.

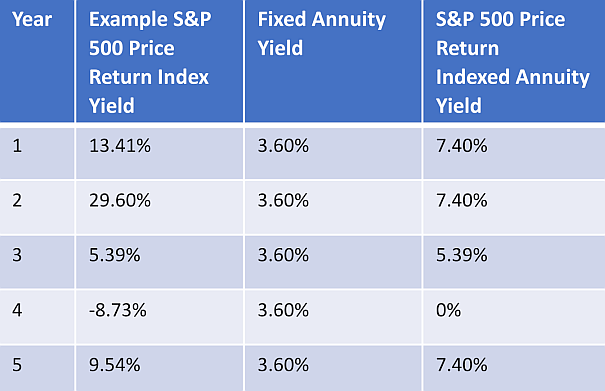

While a fixed annuity is a solid concept for investors that want a fixed return every year with little volatility, an indexed annuity allows clients the ability to have a higher earning potential while still protecting their principal and accrued earnings. With an indexed annuity, the earnings the client receives each year are tied to a particular equity index (eg S&P 500 Price Return). If the index goes down in a year, the client’s principal is protected and they do not share in the losses. If the index goes up in a given year, the client receives the full gain for that year (or a “participation” portion of that gain for some annuities) up to a given cap. In the indexed annuity example given above, and the indexed annuity example that will be used for modeling, the client would receive the full gain up to a cap of 7.4%.

A variable annuity essentially operates like an indexed annuity except without the floor of 0% or any cap. In other words, the client invests in a collection of available funds and takes the full equity risk. With a variable annuity the insurance company makes its profits by charging a spread over what the underlying fund is earning and what is being credited to the client. We’ll discuss variable annuities later on in this article, but for now let’s focus on fixed and indexed annuities. The table below shows an example of what return a client would earn if they were invested in a no-commission fixed annuity earning 3.6% or an S&P 500 Price Return indexed annuity with a floor of 0% and a cap of 7.4%. Hypothetical S&P 500 Price Returns are shown for each of the years below in order to understand how the indexed annuity works. We’ll be using the S&P 500 Price Return Index as that option is found in almost all indexed annuities.

Fixed and Index Annuity vs S&P 500 Index:

While a fixed annuity offers clients a consistent yearly return, the indexed annuity offers the client a larger potential upside while offering downside protection in case the index loses money in a given year.

Annuities offer a number of pros and cons that need to be considered prior to diverting funds away from equity investments or bonds into these products.

Fixed annuities allow clients to share in the life insurance company’s general account returns which are comprised of primarily (~70%) long-term investment grade bonds of the highest quality (Moody’s Aaa or Aa, S&P A- and above). It’s important to note that an annuity invests in the same investment grade bonds that can be found outside the annuity. The annuity company just adds a layer of tax-deferral and reduced volatility to the structure since the bonds in the general account are typically long-term buy and holds as opposed to being subject to constant rebalancing. The fixed annuity crediting rate is thereby just a function of the earned interest rate on this general account minus a small spread. In a low-interest rate environment, a life insurance company’s general account will typically outperform a newly constructed bond portfolio of similar maturity and risk. The reason for this is that the life insurance company’s general account portfolio also includes 30 year bonds from decades ago that were purchased in a higher interest rate environment and so provide significantly higher yields than today’s 30 year bonds. As such, when an insured pays a premium to an annuity company in this low interest rate environment they will get the benefit of sharing in higher risk-adjusted returns. The downside is that when interest rates rise, the life insurance companies’ general account returns will not rise as quickly as newly constructed bond portfolios.

Keep in mind that unlike corporate bonds, insurance companies are required to hold significant reserves to back their liabilities as a result of the annuity and life insurance guarantees they offer. These reserves are generally within 8% and 12% of a company’s revenue and are set aside to account for any temporary fluctuations in cashflows. In order for clients’ investment in these products to be at risk, the entirety of this reserve and any surplus capital the insurance company is holding to back the guarantees would have to be depleted at which point the clients would become general creditors of the insurance company. Also keep in mind that any annuity guarantee provided by an insurance company in the event of complete failure by the insurance company would typically be covered by the state of issue’s guarantee association (typically up to $300k).So when a client invests in a fixed annuity product they are sharing in the life insurance companies general account portfolio while also getting default protection that they wouldn’t receive if they invested directly in corporate bonds themselves. As such, clients that invest in annuity products are taking significantly less risk than typical corporate bonds while earning returns in excess of current long-term Treasury rates. And as we’ll see later on, while pre-tax yields in corporate bond funds will be higher outside the annuity, the after-tax returns will be higher inside the annuity due to the reduction in volatility and the benefits of tax deferral.

Indexed and variable annuities offer clients the ability to invest in an equity index just as they could outside of the product. However, most indexes within an indexed annuity are price return indexes, and not total return indexes. This means that the index returns within the indexed annuity won’t include the benefit of dividends that contribute meaningfully to total return over time (whereas investing in mutual funds or S&P 500 total return indexes outside the annuity product would allow the client to receive and/or reinvest the dividends). In this manner, when an investor chooses to invest in an indexed annuity instead of the same total return index outside of the annuity, they are giving up the benefit (and extra yield) of dividends in exchange for having their investments within the annuity protected from any losses.

While bond gains are taxed at ordinary income tax rates outside of an annuity, long term equity gains outside of an annuity are taxed at much lower long-term capital gains tax rates. However, within an annuity all gains are taxed at ordinary income tax rates. So if the client invests in an equity index within an annuity the gains would be taxed at higher ordinary income tax rates than if the client were to have invested in the same index outside of the annuity. So while tax-deferred annuities can be great vehicles for replacing tax-inefficient bond investments, they are not tax-efficient vehicles for replacing traditional equity investments which will perform much better on an after-tax basis outside an annuity product than within it.

While no-commission variable annuities have no surrender charges, fixed and indexed annuities do. No commission variable annuities are able to eliminate surrender charges because clients are taking the entirety of market risk. With fixed and indexed annuities the insurance company is protecting the client against market or interest rate risk. When a client invests in an annuity they are giving up liquidity in exchange for tax-deferred growth and potentially higher returns. While no-commission annuities allow for limited withdrawals each year during that time without a penalty (~10% of assets can be withdrawn each year), any withdrawals in excess of that are hit with surrender charge penalties. The penalty is typically around 10% in the first year and decline each year afterwards over a 5-7 year period.

Annuities are considered retirement vehicles in the eyes of the IRS. As such, withdrawing any amount from an annuity vehicle before the age of 59 and a half is hit with a 10% tax penalty and this is after any surrender charges are applied. The gains are then taxed at the ordinary income tax rates of the client.

Just like with current crediting rates on life insurance products, the fixed crediting rates and caps on annuity products are subject to change. Usually these rates are locked-in for the first few years, but after that are subject to change depending on the life insurance company’s investment performance. While this might dissuade some investors, it’s important to note that large fluctuations in these rates and caps are unlikely for well established companies. But more risk-averse clients should check to see how long the current rates and caps are guaranteed for and how long that compares with the surrender charge period. Companies with longer guarantees typically will have lower fixed crediting rates and index annuity caps.

It’s also important to note that while bond funds often rebalance their portfolios in response to changing interest rates, life insurance companies typically employ a more buy and hold strategy with regards to the long-term bonds they buy in order to meet their long-term liabilities. As a result, while a changing interest rate environment will have an immediate impact on the market value of a bond fund, there will have to be a sustained change in the interest rate over a long period of time for it to affect the current crediting rates of life insurance companies.

Want to earn CFP continuing education credits for reading this article? Email [email protected] to learn how.

A static set of assumptions can provide us with an expected return for those static assumptions. For example, if a client puts $1,000 in a bank account earning 3% each year at the end of 10 years the client will have $1,344 in his or her account.

But what if the assumptions aren’t static and vary around a mean? While a static set of assumptions might be able to give us an expected return, it won’t tell us anything about how volatile that return is. Monte Carlo simulations on the other hand allow us to test a set of assumptions that vary around a mean and see how volatile the results are. For conservative investors that are concerned with volatility as much as they are about expected return, Monte Carlo simulations can be an invaluable tool.

By doing Monte Carlo simulations of a bond portfolio in comparison to various no-commission annuities using caps and crediting rates from an actual no-commission annuity on the market we can see under what assumptions investors on average would achieve better returns and/or lower volatility over the long-term by investing in no-commission annuities instead of traditional bond portfolios. In the Monte Carlo simulations below we’ll be comparing a bond portfolio versus a fixed annuity and an indexed annuity. Later on in this article we’ll discuss the issues with variable annuities and how to best use them.

Before we simulate results, however we need to set assumptions for the mean returns and expected volatility of the bond and equity portfolio and the fixed annuity. Note that since the indexed annuity will be based on the equity index, the expected returns for the indexed annuity will be simulated.

Modeling assumptions:

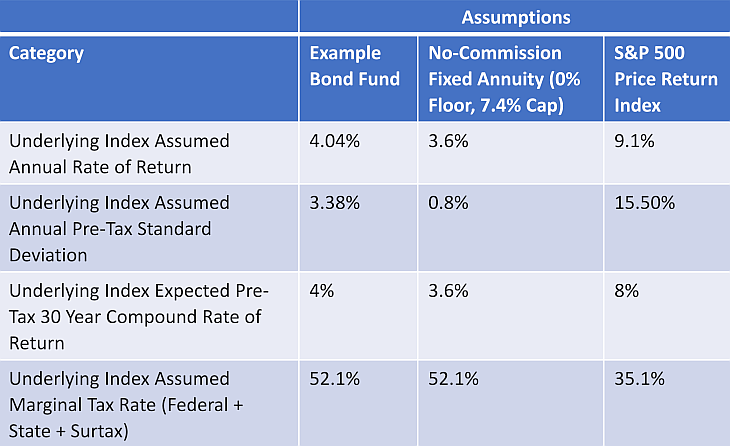

Before doing Monte Carlo Simulations, the assumptions for both the bond portfolio, the fixed annuity rate, and the S&P Price Return must be established. Once those are established the portfolios can be simulated and the after-tax returns and volatility can be compared.

In order to simulate bond, equity, and fixed annuity returns we need to use benchmarks for the bond and equity portfolios. A standard benchmark for bond returns is the Barclay’s bond fund which over the past 15 years has had a long-term return of approximately 4% and an annual standard deviation of 3.38% i For the equity return we’ll be using the S&P 500 Price return which has a long-term return of about 8% and a historical variation of 15.50% over the past 15 years. ii

As we described in an earlier section, note that the expected annual return is not always the same as expected long-term compounded return. The more volatile the underlying index is (i.e. the larger the annual standard deviation is), the more volatility drag reduces the long-term compounded return.

As mentioned previously, the crediting rate on the fixed rate annuity is also subject to change. However, the likelihood and degree to which it will change is small relative to current interest rate changes due to the larger amount of older bonds in the portfolio, the large reserves backing the annuity product, and the overall public relations risk that comes when an insurance company lowers its crediting rate on its products. So while we can safely expect that the volatility will be less than the 3.38% we’ll be using the bond-portfolio, the question is how much less can we expect it to be? In the absence of data we’ll be using a 0.8% assumption for the annual standard deviation and then sensitivity testing the assumption later. Since we’re assuming that the fixed crediting rate will be changing from year to year, we’ve also implemented the same 7.4% cap and the 0% floor that we’ll be using on the indexed annuity side.

Since the indexed annuity is just the S&P 500 Price Return with a floor of 0% and a cap of 7.4%, the performance of the indexed annuity is reliant on the performance of the S&P 500 Index. To determine what the long-term returns and volatilities of these options are, we need to perform Monte Carlo simulations.

Bond and stock portfolios were simulated using an arithmetic mean (which resulted in the desired long-term compounded pre-tax geometric mean) and a corresponding standard deviation described below. Yearly stock results were compiled by first simulating a yield based on the arithmetic mean and annual standard deviation for the stock portfolio. If the yield was negative, the end of year value of the portfolio was brought down accordingly and a capital gain loss was noted. All capital gains losses were accrued and offset against future positive capital gains. If the yield was positive, the end of year value of the portfolio was increased accordingly. If the stock portfolio was outside of an annuity then long-term capital gains taxes were paid only when the portfolio was assumed to be liquidated (for the purpose of calculating end of year after-tax IRRs). If the stock portfolio was inside of an annuity (e.g. indexed annuity or variable annuity), then ordinary income taxes were paid only when the portfolio was assumed to be liquidated.

Bond portfolio returns were also simulated using an arithmetic mean (which resulted in the desired long-term compounded pre-tax geometric mean) and the corresponding standard deviation for the bond portfolio. If the yield was negative, it was assumed that no dividend was paid in that year and that was a loss of base that future yields would be based on. If the yield was positive, it was assumed that a dividend was paid out in accordance with the yield, ordinary income taxes were paid in that year on the dividend and deducted from the gain. The remainder of the gain was then reinvested back into bond portfolio as additional tax-exempt principal.

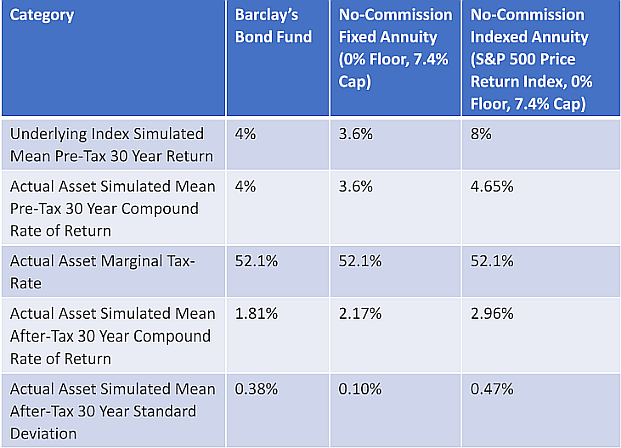

In order to do the Monte Carlo simulations, $1 million was assumed to be initially deposited into an example bond fund, a no-commission fixed annuity, and a no-commission indexed annuity (eg the S&P 500 Price Return with a 0% floor and 7.4% cap). The rates used for both the fixed and indexed annuity were taken from actual no-commission annuities in the market.

These deposits were projected forward for 30 years using Monte Carlo simulations based on the long-term mean and annual volatility of each respective option. One thousand scenarios of these 30 year projections were done so that 30 year after-tax mean returns and volatilities could be determined. The results are shown below.

Monte Carlo Simulations of Bond vs Fixed Annuity and Index Annuity Portfolios:

Both the fixed and index annuity offer higher 30 year after-tax returns than the bond portfolios with the fixed annuity having significantly lower volatility.

While the fixed annuity has a lower 30 year pre-tax return than the bond portfolio, on an after-tax basis the fixed annuity has a nearly 60 basis point increase in the IRR due to reduced volatility and the benefits of tax-deferred growth afforded to the fixed annuity but not to the bond portfolio. We noted in setting the assumptions that the yearly volatility of a fixed annuity is significantly less than that of a bond portfolio due to less fluctuation in the yield of an insurance company’s crediting rate versus that of current bond portfolios that are sensitive to changes interest rates. The 30 year volatility of these returns are even less as a result of the convergence to the mean over time.

The indexed annuity, as expected has both a higher 30 year pre-tax return and after-tax return than the bond portfolio. This obviously is due to the value add that comes from receiving a part of the upside of the S&P 500 Price Return in combination with the downside protection.

Also, as expected the benefits of reduced volatility and tax-deferred growth of both the fixed and indexed annuity increased over-time over the bond-portfolio.

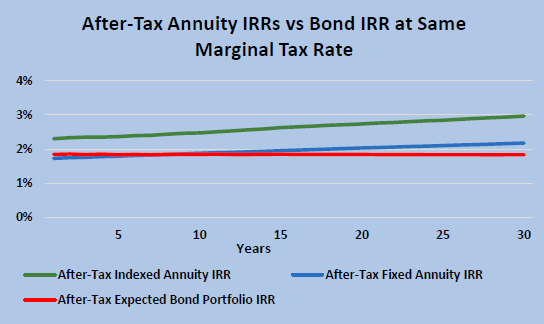

After-Tax Annuity IRRs vs Bond IRRs at the Same Marginal Tax Rate:

While the after-tax return of the bond-portfolio stays constant over time, the tax-deferred growth of the fixed and index annuity helps the IRR of these products grow over time.

Note that the analysis was done assuming that the client’s marginal tax rate stays the same at the time they made the annuity deposit and when they made the withdrawals. For those clients that are in high marginal tax brackets but plan on retiring with lower marginal tax brackets (i.e. by having less annual income or moving to a state with no state income tax) the advantages of the tax-deferral will be even more significant.

As shown in the graphs above, the reduced volatility and tax-deferred growth of the both the fixed and indexed annuity offer superior returns and comparable over the after-tax bond portfolio returns. But an important question investors should be asking is:

What is the break-even point at which investing in a fixed annuity or indexed annuity starts to make more sense than investing in a traditional bond portfolio?

In other words, how much lower can the assumed compounded return on the no-commission fixed or indexed annuity drop and still break-even with the bond portfolio earning 4%?

Sensitivity testing the interest rate assumption—as done in the table below—helps answer that question.

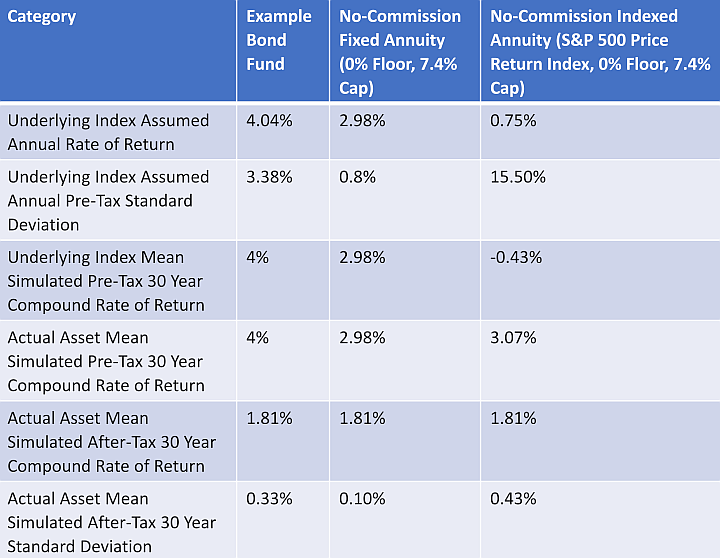

Interest Rate Sensitivity Testing—Determining Break-Even Points:

In order for the after-tax benefits of the no-commission fixed annuity to start to beat that of the bond portfolio, the fixed annuity expected annual rate of return has to be at least 2.98% which is 106 basis points less than the expected annual return of the bond portfolio (4.04%). In order for the after-tax benefits of the indexed annuity to surpass that of the bond-portfolio, the expected annual return of the underlying index of the indexed annuity (the S&P 500 Price Return) has to be at least 0.75% which is 329 basis points less than that of the bond portfolio.

The above sensitivity tests show a clear after-tax advantage of both the no-commission fixed annuity and the no-commission indexed annuity under the given assumptions. As shown in the table above, the no-commission fixed annuity starts to offer a better after-tax advantage once the fixed crediting rate is within 106 basis points of the bond-portfolio. The indexed annuity has a much lower break-even point. As long as the S&P 500 Price Return has an annual expected return of 0.75% or greater, the indexed annuity provides more after-tax benefit than the bond portfolio. From the table we can see that the 0.75% expected annual return results in a mean 30 year expected compound return of -0.43%. On its face, this result is surprising. If the mean long-term return of the underlying index is negative, how is it that the indexed annuity—which is based on that index—can perform better than the bond portfolio?

The answer obviously lies in the fact that the indexed annuity provides a floor of 0%. So even in years in which the index provides a negative return, the client is protected from a loss. However, in the years in which the S&P 500 Price Return is positive the client is able to receive the benefit of that gain up to the cap of 7.4% in that year. For these reasons, the pre-tax long-term return for the client is 3.07% even though the long-term mean return for the index is -0.43%. Keep in mind, however, that if the long-term return on the S&P 500 Price return really started to get close to -0.43% that the insurance company would almost universally lower the cap on the product so that the client would get less of the upside when the market does well.

It’s also important to sensitivity the volatility assumption as well. How would the no-commission fixed and indexed annuities perform if both the interest rate assumption declined AND the volatility increased? The table below helps us answer that question.

Interest Rate and Volatility Testing:

In the table above both the interest rate and the volatility was sensitivity tested. The expected annual interest rate was decreased from the current/assumed crediting rates to 2.98% for the fixed annuity and to 0.75% for the S&P 500 Price Return. The volatility was also increased for both the fixed annuity and the S&P 500 Price Return. The annual volatility for the fixed annuity was increased from 0.8% to 3.38% which is that of the bond portfolio. The S&P 500 Price Return expected annual volatility was increased from 15.5% to 20%.

Increasing the volatility increased the after-tax returns of both the fixed annuity and the indexed annuity in comparison to the sensitivity test in which just the expected annual rate of return was decreased.

The first thing that should be observed by readers is that increasing the volatility actually increased the after-tax returns for both the fixed annuity and the indexed annuity in comparison to when just the expected annual rate of return was lowered. This is particularly notable for the indexed annuity which had a lower pre-tax 30 year return for the S&P 500 Price Return index, but a higher pre-tax return for the indexed annuity (which was based on the S&P 500 Price Return) when compared to when just the expected annual rate of return for the index was lowered. Since we know that volatility hurts long-term returns, how is it that it helps the fixed an indexed annuity?

Well the answer lies in the fact that increasing volatility means that the returns will vary a lot more and go both up and down equally, but to a greater extent than when the volatility is lower. However, the important consideration here is that unlike the bond portfolio or the S&P 500 Price Return, the annuities are flooring the return at 0%. So when volatility hurts the underlying index and brings it below 0%, the annuities don’t reflect any of the negative loss back to the investor. However, when volatility helps the return the investors still are able to benefit from the gain up to the cap of 7.4%. In other words, for investors worried about decreasing rates of return and increasing volatility in the bond market, the no-commission annuities provide both protection and increased return!

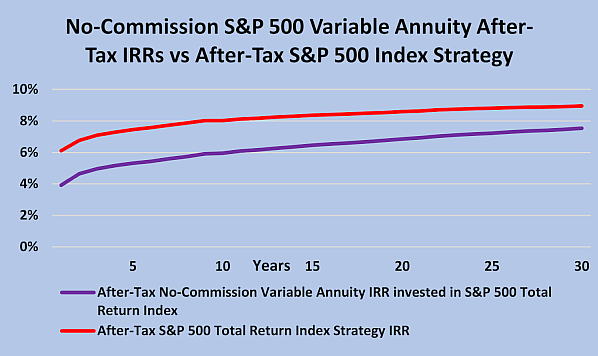

While no-commission fixed annuity and no-commission indexed annuities can offer significant benefits for clients over bond investing, the same cannot be said about no-commission variable annuity products. The reason has nothing to do with the no-load element of the policy—which in general drastically reduces expenses—but rather with the taxable status of the variable annuity. In other words, even for no-load variable annuities that remove the majority of sub-advisor fund fees and insurance company management expenses, the gains within a variable annuity are still taxed at ordinary income tax-rates instead of the long-term capital gains rates that these funds would be taxed at if the client would have invested in these same funds outside the product.

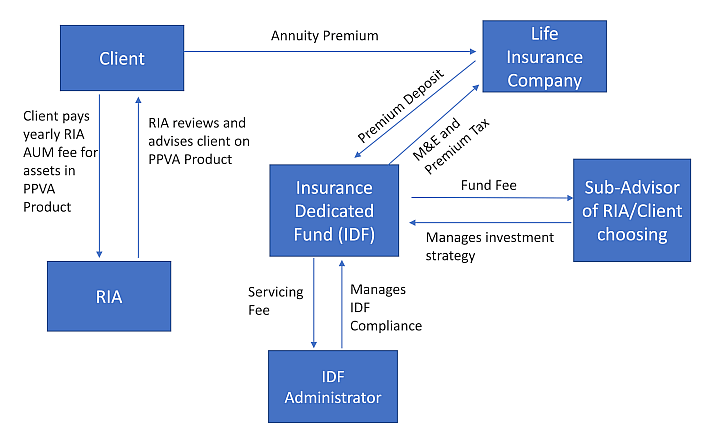

No-commission variable annuity structure:

While no-commission products allow for the fund-fee paid to the sub-advisor and the M&E fee paid to the insurance company to be drastically reduced, all the gains in the product are still subject to higher ordinary income tax-rates

For high-income clients that would be taxed at high marginal income-tax rates, investing in the same funds within a no-commission variable annuity—even one with no sub-advisor or insurance company expenses—results in higher taxes being paid than would otherwise be paid if the client invested in those same funds outside the product.

Investment funds subject to long-term capital gains outside of an annuity are subject to ordinary income tax rates when placed within a variable annuity:

While the no-commission structure allows for the M&E fees paid to the insurance company to be drastically reduced, all the gains in the product are still subject to higher ordinary income tax-rates. The graph above shows the after-tax IRRs of an S&P 500 Total Return fund outside of a variable annuity product versus if that fund was placed with a variable annuity product. There are no expenses associated with either option. The only difference is that the gains inside the variable annuity product are taxed at a 52.1% ordinary income marginal tax rate, while the gains outside the variable annuity product are taxed at a 35.1% long-term capital gains tax rate.

As evidenced in the graph above, even when it is assumed that both the variable annuity product and the outside fund have no expenses, the large difference in tax rates between the ordinary income tax rates and long-term capital gains tax rate makes investing in the fund within the variable annuity product a poor option as opposed to doing so outside of it. Note that in reality, even no-commission variable annuities have expenses within the product (the insurance company and the sub-advisor both typically earn a management fee that collectively can equal 0.5%-1.0%+ of the policy value each year for non-index type funds). The higher these fees are, the lower after-tax returns the client can expect.

Clearly the problem with variable annuities lies in the difference in taxation between long-term capital gains and ordinary income tax rates. However, it’s important to note that not all equity investments are taxed at long-term capital gains rates. Some hedge fund strategies for example are based on short-term transactions (commodities trading, short-selling, option-trading, etc). These short-term capital gain strategies are all taxed at ordinary income tax-rates. So investing in an equity fund that is subject to short-term capital gains within a variable annuity would allow f tax-deferred growth without paying higher marginal tax rates.

Short-term capital gains hurt alternative asset strategies more than bond strategies:

Due to the higher return expectations of short-term equity strategies subject to short-term capital gains, these strategies on an absolute basis lose more to taxes than a lower-yielding, less volatile bond-strategy. As such, high earning and/or highly volatile alternative assets subject to short-term capital gains could benefit even more than bond strategies from a tax-deferred vehicle.

Furthermore, putting alternative equity strategies into a tax-deferred vehicle offers a significantly higher savings potential over putting a bond portfolio into such a vehicle. This is due to the fact that alternative equity strategies tend to have both higher expected return and higher volatility characteristics. Both of these characteristics allow for higher tax-deferred growth. An increasing expected return means that a larger amount is lost to taxes and increasing volatility—as we’ve shown in an earlier section—hurts long-term returns.

As indicated in the previous section, investing in an alternative asset inside of a variable annuity would minimize the large loss due to taxes that would occur outside of the variable annuity. Unfortunately, alternative asset strategies subject to short-term capital gains are actively managed which means that the management fees involved in investing in a short-term capital gains strategy within a traditional variable annuity would be exorbitant, thereby significantly reducing the benefit of the tax-deferred growth.

A private placement variable annuity can remove commissions and a lot of the high insurance and fund-expenses associated with investing in an actively managed alternative-asset strategy within a traditional variable annuity.

Private Placement Variable Annuity allows opportunity for lower management fees and expenses:

By removing commissions, expenses, and the constraints of traditional variable annuities, the private placement variable annuity allows RIAs that design their own short-term capital gain strategies to place their strategies within a tax-deferred vehicle to reduce the drag of high marginal tax-rates.

While the private placement variable annuity can be structured without commissions just like the no-commission variable annuity, there are still insurance company M&E fees and servicing fees that need to be paid to administrator of the Insurance Dedicated Fund (IDF). The cost of both of these is roughly 0.80% combined.

Does the tax-deferral of the private placement variable annuity make the 0.80% cost worthwhile for a high-earning alternative asset subject to short-term capital gains? The graph below definitively answers that question.

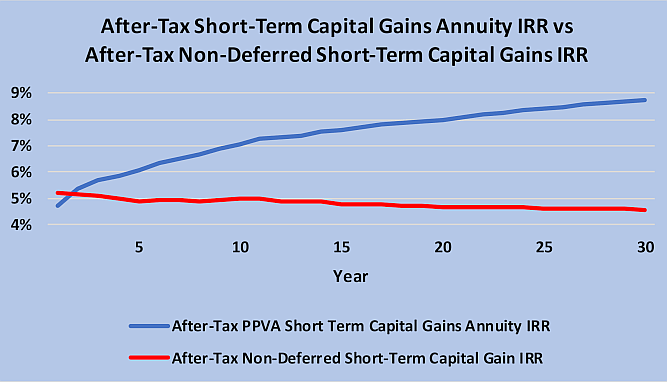

The benefits of tax-deferral for high yield/high volatility assets subject to short-term capital gains:

While both the tax-deferred short-term capital gains annuity and the non-tax deferred short-term capital gains strategy are high-earning/high volatility assets (Long-term expected return of 12% and 20% annual volatility), the different tax-treatment significantly affects after-tax returns.

In the graph above both strategies have a long-term pre-tax expected return of 12% with an annual volatility of 20%. While the 0.80% cost of putting the short-term capital gains asset into the private placement variable annuity hurts the after-tax return in the first year, the benefits of deferring taxes on a such a high-yielding asset with a high tax-burden and high volatility are evident in the following year and continue to grow. You might notice, in comparison, that the after-tax return of the non-tax deferred strategy is actually decreasing over time. This is a result of the heavy friction lost from paying taxes every year which lowers the long-term compound return. After 30 years the after-tax return for the private placement annuity is 8.72% while the after-tax return for the non tax-deferred strategy is only 4.72%.

Annuities providing principal protection or tax-deferred growth clearly meet a client desire. Every year around $200 billion in annuities are sold to clients every year. But the problem with annuities—as it is with most insurance products—is that most of these products are not so much bought by fully knowledgeable clients as they are sold by charismatic annuity salesmen.

And as often is the case when products are sold in this manner, the product the client receives with their investment is not often in their best interests. Many financial advisors have found themselves in the unenviable position of trying to unwind a client from a high-expense ridden variable annuity product that was purchased by the client years ago without the client fully understanding the drag of the expenses that were involved. A 1035 exchange from such high-expense products to no-commission products would not only better the client’s returns but illustrate the value a fiduciary advisor can provide.

The advent of no-commission annuity products and a greater interest in client solutions that meet a fiduciary standard have shifted the value proposition of annuity products from products that benefit agents with high commissions to products that benefit clients with enhanced returns and protection. As I’ve shown in this article, for investors and their clients wanting principal protection against market losses, or wanting to benefit from the tax-deferred gains, no-commission annuities can provide both reduced volatility and higher expected returns when compared to traditional bond portfolios or short-term capital gains strategies.

What these no-commission products are missing, however, are advocates educating financial advisors and clients about the value that such products can have in portfolio management. While ripping out the commissions from the product significantly reduces expenses and provides a better product, it also removes the monetary incentive for agents to market the product to their network. This provides a catch 22 for the industry: create high-commission products and you’ll have a plethora of agents knocking down doors of clients and their financial advisors to sell a poor performing product to. Eliminate commissions and you’ll be able to create better performing products with no one to sell them.

The only way these products can create a significant market share is if financial advisors understand the value these products offer both to clients and themselves and start incorporating them into their financial practice. By doing so the client receives a better performing product that they clearly have a demand for and financial advisors are able to charge an advisory fee or an asset-under-management fee on the assets in the product. Will that advisory/asset-under-management fee ever equal the large upfront commission currently earned by agents/financial advisors for selling the high commission annuity counterparts? Not upfront of course. But earning a 1% AUM fee every year over 20 years of better performance in a no-commission annuity can more than make up for it for both the client and the financial advisor. It’s definitely better than a client diverting funds away from a fiduciary financial advisor to invest in a high-commission, poor performing annuity simply because the commission-based agent is addressing the client’s fears and concerns when the fiduciary financial advisor is not.

Author

This blog post explores essential PPLI due diligence steps, covering carrier evaluation, regulatory considerations, investment platforms, tax compliance, and advisor expertise to help high-net-worth individuals make informed decisions before implementing this specialized insurance solution.

Discover how PPLI enhances business succession planning through key person insurance and buy-sell funding. Learn private placement life insurance strategies for business owners.

Learn how to evaluate PPLI carriers by balancing financial strength ratings against investment platform flexibility. Compare fee structures and long-term costs to select the optimal Private Placement Life Insurance carrier for your wealth strategy.

0 Comments