The Hidden Costs of Permanent Life Insurance

Rajiv Rebello

Author

August 29, 2017

Author

For clients considering purchasing permanent life insurance, the options can be daunting. Life insurance policies address many different client desires. Understanding the many choices available—and the total cost associated with each option—is critical to making a selection that best matches the financial plan and individual risk profile of that particular client.

Unfortunately for the client, the person who understands the most about life insurance is the same person trying to sell it to you. This creates an inherent conflict of interest.

A life insurance agent earns 80 to 100 percent of the first year premium that the policy owner pays into a policy. This means the agent is incentivized to sell as much life insurance as possible—and to encourage the policy owner to pay as much for it as possible. The policy owner, on the other hand, often has very different needs.

Most people start thinking about purchasing life insurance in order to provide replacement income for their families in the case of death. Generally speaking, people have high life insurance needs when they are younger, but lower life insurance needs as they age.

A young family just starting out typically has high current and future liabilities. An example might be a family facing student loan debt, revolving credit debt and a mortgage payment, all while trying to save for their children’s college expenses and their own retirement. In most cases, the family has limited assets to pay for these liabilities in the case of an untimely death. Hence, they have a need for life insurance.

Agents can easily convince a family to purchase permanent life insurance to cover these needs with the promise of providing a solid investment for the future.

However, as time passes, the family’s financial position and needs change. Their children graduate from college to start their own lives and careers. The mortgage gets paid down along with other debts. Household income typically rises as the parents earn higher wages at their respective jobs.

Overall, the family has fewer financial obligations. The family soon comes to realize that they don’t really need as much life insurance as they did when they were younger. Often times they cancel their policy after just a few years of owning it. This is often done at a significant loss to the client.

Chart 1:

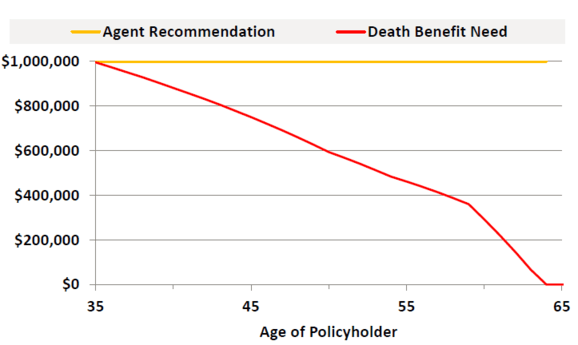

The chart above shows the modeled death benefit needs over time of a married 35 year old with two small children, a mortgage, and outstanding debt. While he has $1M in life insurance needs as of day one, by age 65 he doesn’t need life insurance as he has managed to self-insure his future liabilities by that time.

The agent will often recommend that the policy owner purchase as much life insurance as possible as of day one whether it matches the policy owner’s needs or not. However, nearly 50% of all permanent life insurance policies are canceled within the first 10 years often leading to significant financial losses for the policy owner.

The life insurance agent will recommend the client purchase an amount of insurance (yellow line) that is significantly higher than what the client actually needs (red line).

Approximately 50 percent of all policy owners who purchase permanent life insurance end up canceling the policy within 10 years.

Unfortunately, because life insurance carriers pay so much in commission to the life insurance agent in the first year of the policy, the life insurance company has to assess a heavy cancellation fee (known as a surrender charge) to the policy owner in order to recoup their expenses.

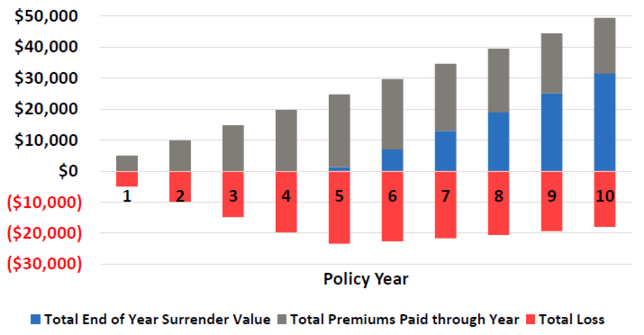

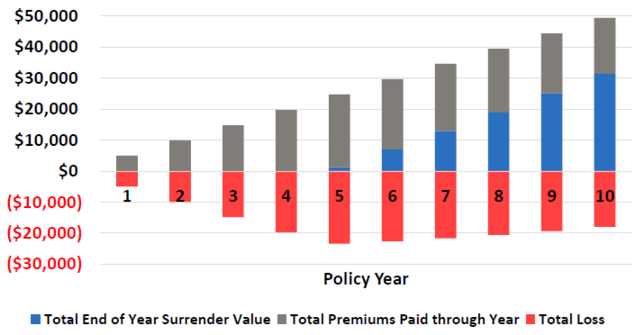

As a result, policy owners often spend a lot more in premiums on the policy than the cash they end up getting back when they cancel it. This results in a very significant financial loss, as evidenced by the red bar of losses in the table below

When a policy owner cancels a policy, the life insurance carrier gets the monetary benefit of having collected premiums on a policy without ever having to pay a death benefit in return.

It’s a great position for the life insurance carrier to be in. Unfortunately, it’s the policy owner who ends up paying the price for the carrier’s good fortune in these cases

Chart 2:

This chart compares the total premiums paid for a $1M policy on a 35 year old from a top life insurance company that holds an AM best A- rating. The table above shows the total premiums paid through a given policy year (gray bar) with the corresponding end of year surrender value (blue bar).

The total loss (difference between paid premiums and surrender value) is shown by the red bar.

For the first five years, the policy owner pays almost $25k in premiums but only receives $1k back if he cancels the policy. Canceling the policy at this point would result in a $24k loss.

For the ten year period this amounts to a $49k premium outlay with only a $31k refund on cancellation of the policy resulting in an $18k loss.

As we’ve stated, nearly 50% of all permanent policies are canceled within 10 years. For reference purposes, a 10 year term policy for $1M would have only cost the policy owner $2k in total premiums.

By buying the permanent policy and canceling it after 10 years the policy owner ends up spending $16k more than if he/she were to just have purchased the 10 year term product instead of the permanent policy.

Policy owners collectively lose hundreds of millions of dollars in assets due to poor financial planning and sales practices of life insurance agents that are often not in their best interests.

In order to ensure that policy owners don’t fall into the pitfalls described above, financial advisors need to help policy owners better understand their needs for liability protection, estate protection, and desired investment return and most importantly how these can change over time.

Important questions to ask during the search for the right insurance product for your client are:

Life insurance is an important part of any financial plan. But just as it in can save clients from tens to hundreds of thousands in unforeseen losses, it can just as easily be the cause of those losses if not managed, reviewed, and invested in properly.

As an investment adviser/attorney/CPA you have the opportunity to build a mutually beneficial relationship with your clients based on trust and solid information.

For a flat fee, Colva will analyze the life insurance product under consideration (or already in force) to help avoid these pitfalls. At Colva we want to help your client work proactively with their life insurance sales team to find a product that best meets the needs of the client—and not the agent’s commission goals.

Author

Learn how to evaluate PPLI carriers by balancing financial strength ratings against investment platform flexibility. Compare fee structures and long-term costs to select the optimal Private Placement Life Insurance carrier for your wealth strategy.

Determining the right death benefit level for your Private Placement Life Insurance (PPLI) policy is one of the most critical decisions that will impact your policy’s performance, costs, and overall effectiveness. This comprehensive guide explores how to balance regulatory requirements, estate planning needs, family protection goals, and investment capacity optimization to find the optimal death benefit level for your unique circumstances.

Master essential best practices for PPLI investment committee governance. Learn to establish effective oversight structures, develop robust policies, and implement risk management frameworks that maximize wealth preservation while ensuring regulatory compliance.

0 Comments