Premium Minimization Services

Rajiv Rebello

Author

November 10, 2020

Author

One of the main concerns of life settlement investors is minimizing the premiums required to keep the policy in force. Colva is a specialist in utilizing actuarial principles to determine the minimum premium to keep a policy in force. Current industry practice attempts to use a one-size-fits all model to determine the minimum premium such that the Cash Surrender Value of the policy is above 0. However, this approach fails to take into account two important considerations

Most of the products sold in the life settlement market are universal life products. A significant percentage of these are “Shadow Account” products. Shadow Account products are universal life policies that allow the policy to remain in force as long as the Shadow Account value is positive. Therefore a policyholder can technically pay a premium to keep the policy in force that is significantly less than that required to keep the regular Cash Value account positive.

The problem with Shadow Account pricing for policyowners is that details of the Shadow Account—like its namesake—are kept in the dark. At no point do the policyowners actually know what the value of the Shadow Account is. If policyowners were to in fact to know how the Shadow Account value worked, they could use it to save tens to hundreds of thousands of dollars in life insurance premiums. Unfortunately, Shadow Accounts design products are created by actuaries with extensive actuarial and insurance understanding that the average policyowner does not have

At Colva, we have both life insurance and life settlement expertise with the ability to perform “reverse engineering” on these Shadow Account policies to determine, on a yearly basis, what the real minimum premium to keep the policy in force.

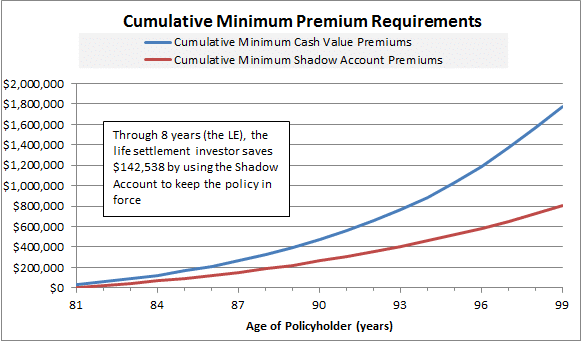

The graph above shows a number of important concepts for a life settlement investor potentially interested in acquiring this policy.

If the investor were to use the premiums required to keep the cash surrender value in force and discount values at a 14% return, the value of the policy would be $95,420. However, with Colva’s actuarial expertise the investor is able to reverse engineer shadow account values and pay the policyholder up to $192,675 for a policy that equates to a 14% priced return for the investor. This means that an investor using the shadow account could pay almost $100k more for the policy and still make a 14% return because the shadow account investor can better reduce premiums than the investor who can only focus on keeping the cash surrender value positive. Furthermore, if the rest of the market is using an industry standard model that does not take shadow account values into consideration, the investor using the shadow account wouldn’t have to offer the full $192,675 price for the policy since everyone else is only offering $95,420. The shadow account investor would only have to beat the $95k price—thereby increasing his expected return to much higher than 14%—since no one else would be competing against him for it.

Colva’s reverse premium engineering abilities are so advanced, it is able to project to the dollar the shadow account and account values and solves for an amount that only leaves a few hundred dollars extra in the respective account values to handle differences between carriers’ monthly interest calculations. Furthermore, Colva actually works with the carrier to provide its investors with an in-force illustration to prove that the values it calculates are in fact the minimum required to keep the policy in force. No other life settlement servicer does this.

Contact us at [email protected] to discuss how an actuary from Colva Actuarial Services can help save your life settlement portfolio hundreds of thousands to millions of dollars in unnecessary premium expenses.

Author

Discover how Private Placement Life Insurance transforms charitable remainder trust strategies into powerful wealth replacement tools. Learn tax-efficient approaches that maximize charitable benefits while preserving family wealth for high-net-worth families.

This blog post explores essential PPLI due diligence steps, covering carrier evaluation, regulatory considerations, investment platforms, tax compliance, and advisor expertise to help high-net-worth individuals make informed decisions before implementing this specialized insurance solution.

Discover how PPLI enhances business succession planning through key person insurance and buy-sell funding. Learn private placement life insurance strategies for business owners.

0 Comments