Life Insurance: Are Clients Spending More Than They Need to?

Rajiv Rebello

Author

February 08, 2018

Author

The goal of any comprehensive financial advisor is to help protect the financial situation of their clients and their families as the client ages. The financial advisor wants to ensure that when the client retires the client and their families are fully taken care of. Life insurance is an important part of this long term financial plan—even for high net worth individuals. It covers the gap between the liabilities their family would face in the case of their death and the assets they currently have.

Clients and their financial advisors understand that clients’ financial needs change over time. Unfortunately, they often don’t understand how clients’ life insurance needs change over time as well and fail to account for this in their planning. As a result, many clients spend hundreds of thousands of dollars on life insurance coverage that they won’t fully need as they get older and closer to retirement. The lack of need for life insurance as one gets older is a major reason why a close look at actuarial studies show that over 75% of all life insurance policies are cancelled—often at a great loss to the policy owners.

If financial advisors better understood how to structure life insurance within their clients’ long-term financial plan, they could save their clients thousands of dollars that are unnecessarily spent on life insurance with limited added benefit. These assets could then be put into other strategies the financial advisor has created that provide more growth and protection for their clients retirement needs. As an added benefit for financial advisors who charge a percentage of assets under management fee, by putting these assets into their own strategies they would then get compensated on the additional assets that are under their care.

When it comes to life insurance two of the most important questions are:

Picking the wrong product can have significant financial consequences particularly for those policy owners who cancel their policies early. It’s no wonder then that when you take a close look at Society of Actuaries’ lapse studies that we can see that 50% of all life insurance policies are cancelled within 10 years. Furthermore, more than 75% of all life insurance policies are cancelled before the coverage period ends.

The table above shows the 10 year costs for two term products and one permanent life insurance product. As one would expect, the 30 year term product is significantly more expensive over the first 10 years in comparison to the 10 year term product. The 30 year term product is charging the policy owner an expensive premium based on the policy owner keeping the policy a longer period of time. The permanent life insurance product is even more expensive than this. Picking a more expensive product that doesn’t meet the changing needs of the insured over time—or which the client can no longer afford—increases the chance of the policy being cancelled.

There are two main types of life insurance available to high net worth clients: Permanent life insurance or term life insurance.

Term insurance provides a level amount of coverage for a set period of time (10, 20, or 30 years). The insured pays a level premium amount each year for that period and if the insured dies within the term of the policy, the beneficiaries of the policy get the stated death benefit amount. If the policy is cancelled, the policy owner does not receive anything back.

Permanent life insurance—as the name implies—lasts for the lifetime of the insured as long as the insured pays the level premium each year. In addition, permanent life insurance has a savings component. Part of the premium being paid for the policy go towards a savings account that accrues with interest over time. If the insured decides to cancel the policy at any time, they can walk away with the amount that has accrued in the savings component.

The problem with most permanent insurance policies is that the premium is significantly more expensive than term policies and most permanent policies have very poor returns on the savings component. Unless the right policy is chosen, the policy owner is better off purchasing a term policy and investing the difference elsewhere. In the past, permanent insurance was a great way to help avoid estate taxes for high net worth individuals. However, with the estate tax exemption now being raised to $22.4 million for married couples, there’s only a select few individuals who would benefit from using permanent life insurance to avoid estate taxes. Permanent life insurance should only be used in cases in which the true return on the savings account is greater than the returns the client could earn elsewhere.

Term insurance provides coverage for only a set period of time while permanent life insurance coverage can provide coverage for the lifetime of the insured and a savings account component. The problem with permanent life insurance is that the premiums required to keep the policy in force are significantly more expensive than the premiums for term insurance. Generally the internal rate of return on the savings portion of the permanent life insurance product is too low for the permanent life insurance product to be a better fit than a comparable term policy.

In this case example, unless the investor is earning less than 3.33% on his or her long-term investments, the client should not purchase a permanent life insurance product as the client would be better off purchasing a much cheaper term policy and investing the difference in higher earning strategies that the financial advisor can create.

As one might expect, younger adults typically have high liabilities, but limited assets to match them. Mortgage payments, future college expenses for dependent children, and unfunded retirement plans are serious risks that need to be taken care of in the event of an untimely death for a younger adult with a family depending on his income.

However, as that adult ages his or her financial situation changes. Usually that individual is making more in salary or investment income and mortgage debts get paid down while more money is put into retirement vehicles to provide for future income needs. In addition, children grow up and are no longer dependent on their parents to provide for them. In other words, the clients’ assets increase over time while their liabilities decrease. Ideally at retirement, the client’s future liabilities are fully taken care of by the asset strategy the financial advisor has created.

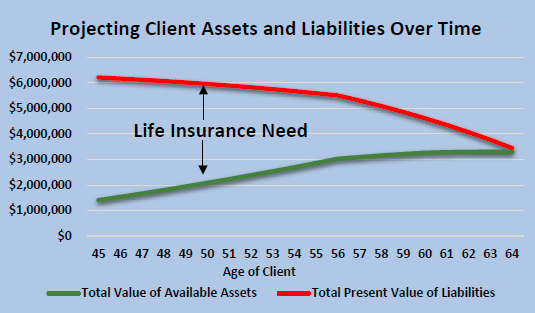

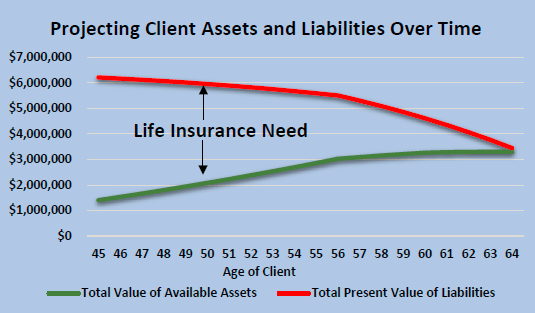

In this case example, a high net worth 45 year old man has over $6.2 million in liabilities that his family would need if he were to die at age 45 but only $1.4M in available assets to pay for them. This deficit of $4.8M is his life insurance need. As he gets older, his liabilities decrease and his available assets increase. As a result, his family needs less life insurance protection as he gets older. If the financial advisor has done a good job in growing and protecting the client’s assets, at age 65 when the client wants to retire there should be no need for life insurance as his assets at that point will cover all future liabilities.

The problem with how life insurance is sold is that life insurance agents are incentivized to get clients to buy as much life insurance as possible—whether they need it or not. What ends up happening is that the life insurance policy the client purchases doesn’t match the client’s changing need. As a result, over 75% of all life insurance policies end up cancelling the expensive policy they purchased—often at a great loss.

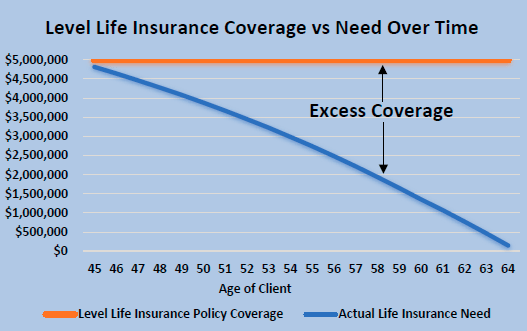

ISince the client’s life insurance needs are decreasing over time, a level $5M policy provides excess coverage as the client gets older. As the client gets older and needs less life insurance, he is more likely to cancel the entire policy. This results in a significant loss to the client as he would have paid expensive long-term premiums while only getting short term coverage.

Well how should a financial advisor avoid the problem of getting a long-term level life insurance policy that will no longer match the client’s needs as he or she ages?

The answer is to get multiple policies with different terms that better match the client’s long term needs than to settle for purchasing one that doesn’t. This results in paying significantly less in premiums and getting the client a product that better matches their needs—and which they are less likely to cancel and suffer a loss.

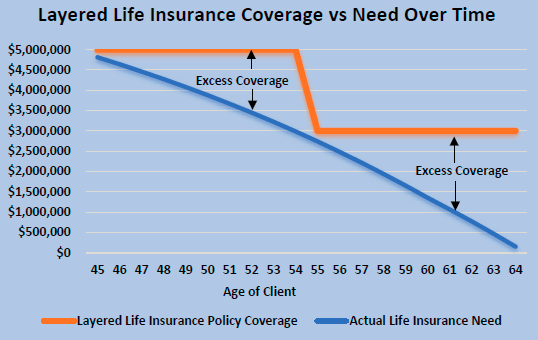

In the previous graph we saw that the getting one $5M term life insurance policy for 30 years provides excess coverage that the client doesn’t need. A better idea is to get separate life insurance policies that are layered and decrease over time. For example instead of a $5M policy for 30 years, the client could get a $2M policy for 10 years and a $3M for 20 years. This would provide $5M of life insurance coverage for the first 10 years, and then $3M for the next 10. In other words, the life insurance coverage drops over time just like the client’s needs.

A $2M policy with a 10 year term when combined with a $3M policy with a 20 year term provides a life insurance solution that better matches the client’s life insurance needs. After 10 years the $5M coverage drops to $3M. This drop in coverage significantly reduces the excess coverage that a level $5M policy would provide. As a result, the client saves significantly in premiums and doesn’t have to cancel his entire life insurance solution since he has the flexibility to cancel just one piece. The client can save even more in premiums by being more aggressive in reducing the excess coverage.

As you can imagine, structuring a life insurance solution like this has numerous benefits. The first benefit comes from the large amount of premiums that are saved through utilizing a layered coverage solution as opposed to a level one. Instead of purchasing expensive policies and coverage that the client doesn’t need, this type of solution allows the client to save money in unnecessary premiums that could be invested elsewhere. The second benefit is flexibility. If a client purchases one policy and decides he doesn’t want that much life insurance coverage his only option is to cancel the entire policy. By purchasing multiple policies the client can choose to cancel only the part of his coverage that no longer matches his needs.

A $2M policy with a 10 year term when combined with a $3M policy with a 20 year term provides a life insurance solution that better matches the client’s life insurance needs. After 10 years the $5M coverage drops to $3M. This drop in coverage significantly reduces the excess coverage that a level $5M policy would provide. As a result, the client saves significantly in premiuA layered life insurance coverage solution provides substantial savings in premiums over a level life insurance solution. In this example, a policy owner would spend $180,000 over 20 years for the level life insurance coverage but only $72,000 for the layered life insurance coverage. This amounts to over a $100,000 in savings that the financial advisor can help the client invest elsewhere. For older age clients in worse health and/or larger life insurance needs, the savings will be much higher.

Due to the conflict of interest between agents who sell life insurance and the clients who need them, its important that financial advisors acting as fiduciaries to their clients first determine how much life insurance the client needs over time. The next step is to make sure that the client is being offered the best deal possible from the agent he or she is working with. Here are some resources and tips to do that.

For financial advisors wanting to check if the life insurance agent is getting the best rates possible, Term4Sale allows a user to quickly put in an age, death benefit amount, and get rates from multiple carriers.

Many clients don’t like applying for life insurance because of the bloodwork and extensive underwriting process that can take over a month to complete. For those that want a more simplified process, several companies have emerged to meet this need. LadderLife, HavenLife, and EthosLife are a few of the companies that provide simplified issue policies that can be obtained within minutes. The downside of these policies are that they are more expensive than traditional life insurance policies since limited underwriting is done. So if your client is in great health or is looking to purchase a large amount of life insurance, the client would be much better going the traditional life insurance route and getting fully underwritten.

As described previously, permanent life insurance is only really suited for a small segment of the population that needs it for long term protection or estate tax protection needs. But for those that need it, there are a number of areas that should be considered.

Permanent life insurance has both a life insurance protection element and a savings/investment account component. The key to evaluating how well the product is performing is to evaluate the yield being earned on just the savings component of the permanent life insurance product. In other words, if we take the life insurance protection component out of the permanent insurance vehicle, what yield is just the savings portion of the permanent life insurance product making?

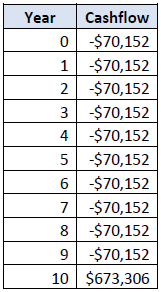

For example, let’s say a client is considering a 30 year $5M term product with a premium of $9,085/year versus a $5M WL life product with a premium of $79,237/year. We can easily see that the difference in premium between the two is the amount that is essentially being invested into the savings component of the permanent life insurance product. We can then compare the invested amount with the end of year value in the savings account that can be withdrawn to determine what the yield on the savings account portion of the permanent product is for each year if the policy owner were to cancel the policy and walk away from it. Below is an example of the cashflows used to determine the 10 year IRR on the investment.

A permanent life insurance product on a 45M requires a premium payment of $79,237. If we compare this against a 30 year term premium which only costs $9,085, then the net investment cost is the difference between these two amounts ($70,152). At the end of each year the savings account has a cash surrender value that the policy owner can walk away with. By comparing the investment cost with the cash surrender value at the end of a respective year, we can determine the investment yield for that time period. For example, after 10 years the cash surrender value is $673,306. This amounts to a 10 year IRR of -0.75%.

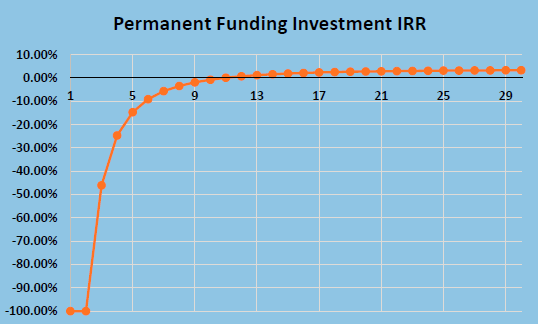

By doing a similar calculation to the one above for 30 years, we can develop a yield curve for the investment/savings component of the permanent life insurance product.

The investment yield on the savings component of this permanent insurance product is highly negative in the early years and then increases in the later years

As you can readily see in the graph above, the early year yields on the permanent life insurance product are negative. It doesn’t even break-even until year 11. In fact, if the client were to walk away from the policy after two years, the client would have spent $158,474 into the product but receive nothing back.

The main reason why the yields are so low are due to the large commissions being paid on permanent life insurance products. Remember that life insurance companies generally pay life insurance agents ~100% of the first year premium that the client pays into the policy. If the policy owner cancels the policy early, the life insurance company will not have had enough time to make the money back. In order to avoid taking a large loss, the life insurance company charges the policy owner a huge surrender charge. This means that the policy owner can pay hundreds of thousands into a policy and get almost nothing back if they cancel the policy early.

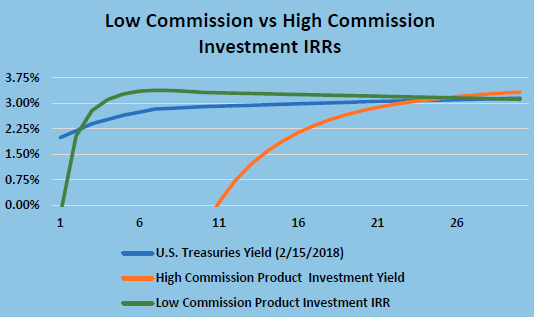

With policies that pay such a large upfront commission, actuaries have no choice but to incorporate large back-end surrender fees. When the policies are cancelled, the life insurance company recoups the large amount they’ve already paid to the agent. Policies that pay low-upfront commissions don’t have this same problem. They’re able to provide better early year returns to the policy owner—especially when funded properly.

Products that offer low commissions offer much better early year returns than high commission products do. Using the treasury curve as a benchmark, we can see that in the early years the low commission permanent life insurance product performs better than the treasury curve. If the permanent insurance product was invested in a higher-earning and riskier strategy, it would be important to measure it against that benchmark. While a permanent insurance product like whole life can offer good yields in the later years, very few policy owners keep it that long to benefit from it.

As discussed, permanent life insurance is only for a select few individuals who either have long-term life insurance needs, have a long investment horizon, or who know how to structure low commission products to maximize returns. For those that fall into those categories, here are a couple of tips to keep in mind.

As discussed above it’s important to separate the savings/investment component of the product from the pure life insurance protection component and compare the yield versus other long-term investments the client is making.

The death benefit on the life insurance component is tax exempt. However, any gains in the product over the premiums paid into the policy is taxable as ordinary income once the policy is cancelled. Some permanent insurance products like Universal Life and Variable Universal Life allow the policy owner to invest in higher-earning/riskier equity assets. While gains on these assets within a permanent life insurance are tax deferred, they are subject to much higher ordinary income tax rates. Outside of a permanent life insurance product these gains would only be taxed at the much lower long term capital gains rate.

Since treasury/bond dividends outside of a permanent life insurance product are taxed at ordinary income rates anyways, it’s much wiser to invest the portion of the client’s portfolio that otherwise be invested in treasuries or other bonds outside the permanent life insurance product into a permanent life insurance product invested in treasuries. This way the policy owner benefits from tax deferred growth without paying a much higher tax rate on the gains.

Most life insurance companies will recommend that you pay a level premium each year. They might recommend that you pay a level premium to age 100. However, if the insured only lives to age 90, you will have paid more premiums into the policy than you needed to. For policies that allow flexible premiums each year, it might be better off for the insured to pay a smaller amount now and risk paying a larger amount in the later years when there is a smaller chance of the insured still being alive and having to pay the larger premiums. Doing so would minimize the expected premiums to be paid on the policy. This is why it’s important to review the funding strategy of the permanent insurance policy every few years and adjust it according to the life expectancy of the insured and the minimum amount of premium that has to be paid each year.

Life insurance is an important component of any financial advisor’s plan for their client. Unfortunately it’s also a complicated component. But as fiduciaries, it’s important that advisors understand the significant financial ramifications that come with their clients making the wrong choices. In the absence of a financial advisor acting as fiduciary in this capacity, the client’s only source of guidance comes from the agent whose incentives aren’t exactly aligned with the client.

Author

Learn how to evaluate PPLI carriers by balancing financial strength ratings against investment platform flexibility. Compare fee structures and long-term costs to select the optimal Private Placement Life Insurance carrier for your wealth strategy.

Determining the right death benefit level for your Private Placement Life Insurance (PPLI) policy is one of the most critical decisions that will impact your policy’s performance, costs, and overall effectiveness. This comprehensive guide explores how to balance regulatory requirements, estate planning needs, family protection goals, and investment capacity optimization to find the optimal death benefit level for your unique circumstances.

Master essential best practices for PPLI investment committee governance. Learn to establish effective oversight structures, develop robust policies, and implement risk management frameworks that maximize wealth preservation while ensuring regulatory compliance.

0 Comments