Using Life Insurance to Increase Returns in a High Interest Rate Environment

Rajiv Rebello

Author

February 16, 2022

Author

Summary: The efficient frontier states that the optimal allocation of stocks and bonds in a portfolio optimizes the expected return of a portfolio for a given level of risk. However, the different taxation requirements of these assets can result in a different optimal allocation on an after-tax basis particularly in a high tax/low-yield environment. By properly utilizing tax-advantaged tools like life insurance, advisors can create more diversified portfolios with greater risk-adjusted returns on an after-tax basis.

Traditional asset allocation models have long since consisted of a mixture of stocks and bonds with a heavy allocation to stocks when clients are younger and an increasing allocation to bonds as clients get older.

The idea between this type of portfolio allocation rests on the belief that a loss on the equity portfolio can be offset by gains in the bond portfolio and vice versa. Hence, to maximize the return of a portfolio relative to its risk, there is an optimal allocation of stocks and bonds that maximize the return-to-risk ratio. This is known as the efficient frontier.

However, the ability to use bonds as a diversification tool is dependent on the interest rate environment. A low interest rate environment, like the one we’re in now, poses a significant amount of risk to the ability to use bonds as a hedge against equity volatility for the following reasons:

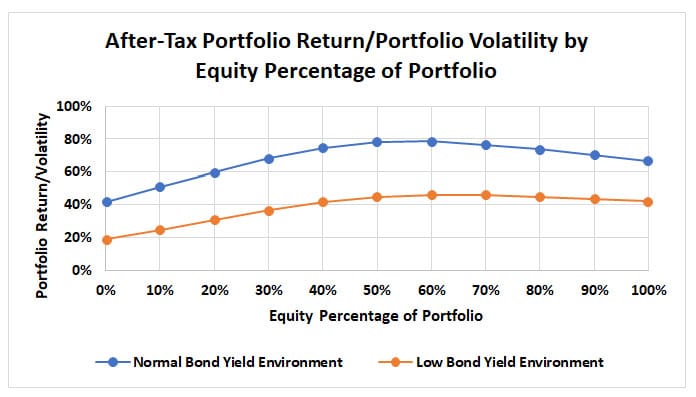

Figure 1: Optimal Asset Allocations in a Normal vs Low Bond Yield Environment on an After-Tax Basis

When equities have higher expected returns than debt, increasing the allocation of a portfolio to equities increases the mean expected return of the portfolio. But doing so also increases the expected volatility of the portfolio. As such, the efficient frontier helps us to determine the optimal equity allocation of a portfolio that maximizes the return of the portfolio relative to the volatility or risk being taken. That’s why in a normal bond yield environment, increasing the equity allocation of a portfolio beyond a certain point results in the return of a portfolio relative to its underlying risk decreasing as evidenced by the “Normal Bond Yield Environment” line (blue line). We can see that in a “normal bond yield” environment that optimal equity allocation to maximize the return/risk ratio is about a 60% equity allocation (the remaining 40% is allocated to bonds).

However, in a low bond yield environment (orange line), increasing the equity allocation results in greater expected return with minimal costs to volatility especially since low bond yields are taxed at a higher rate than equity earnings. Increasing the equity allocation from 60% to 100% in a low yield environment results in a barely noticeable decrease in the return/risk ratio.

Modeling assumptions:

Figure 2: Loss in Price of Bonds after a 1% Increase in Rates

| Bond Term (Years) | Immediate Loss of Market Value of Bond Prices on 1% Increase in Rates from 2% to 3% | Years of investing at higher coupon rate (3%) to recoup initial upfront loss in value | Years of investing at higher coupon rate (3%) to get back to original 2% yield |

|---|---|---|---|

| 10 | -8.53% | 4 | 10 |

| 20 | -14.88% | 6 | 17 |

| 30 | -19.60% | 8 | 23 |

In a low-interest rate environment, bond prices are more sensitive to an increase in rates. As the table above shows, a 1% increase in rates from 2% to 3% creates a large upfront loss that can take clients an extremely long-time to recover from.

The low-yield, interest-rate risk, tax-inefficiency, and correlation issues reduce the viability of using bonds as a traditional hedge against equity risk in this environment. The construction of portfolios going forward therefore needs to both focus on replacing bond allocations in the portfolio with higher risk-adjusted investment opportunities with negative or low correlation and/or focus on reducing the tax-drag of the entire portfolio. Reducing tax-drag can be accomplished through enhanced asset location strategies.

The concept of asset location—placing tax-inefficient assets within structures that minimize the tax-drag—is not a novel one. For decades fee-only financial advisors have been using the tax-advantages of IRA accounts to shield investors from income taxes during their high income earning years or using complicated estate planning strategies like Grantor Annuity Trusts (GRATs) and Intentionally Defective Grantor Trusts (IDGTs) to shield investors from estate taxes.

However, one structure that combines the income tax-saving benefits of retirement accounts with the estate tax-saving benefits of grantor trust strategies—while materially enhancing the tax-savings of both of them—is the use of permanent life insurance.

While long-term bonds offer higher returns than short-term bonds, most wealth managers avoid allocating to long-term bonds in place of shorter term bonds since longer term bonds are exposed to more interest rate risk (See Figure 2). However, life insurance products like universal life insurance, whole life insurance, and fixed annuities offer the ability for clients to invest in long-term bonds through the insurance vehicle without the interest rate risk. In exchange for offering clients access to higher yielding bonds without interest rate risk, the insurance companies earn a spread between what the long-term bond portfolio is earning and what the insurance company is crediting to the client’s account. With whole life insurance, clients receive equity dividends in the later years as well. In the case of universal life insurance and whole life insurance, these returns are also tax-free.

As demonstrated in Figure 1, in a low-yield environment investors can increase the expected return of the portfolio over the long-term with minimal costs to expected long-term volatility by increasing the equity allocation of a portfolio. However, that doesn’t protect against short-term volatility as an increasing equity allocation exposes them to more risk in the short-term. This is particularly risky for older clients in or near retirement as it exposes them to sequence-of-return risk as they start making withdrawals from their portfolios. Increasing the equity allocation for such clients exposes them to increased short-term risk which they may not recover from.

One way to create a greater risk-adjusted profile for the client is to take a portion of the portfolio that would be allocated to short-term bonds (in order to minimize interest rate risk) and allocate it to an indexed annuity or indexed universal life policy. An indexed annuity or indexed universal life insurance policy allows clients the ability to earn equity returns up to a cap while being protected from losses. This type of indexed return with a cap and a floor allows for clients to participate in the higher returns of the equity market without the full volatility. In a low bond-yield environment, this can provide higher risk-adjusted returns than investing directly in short-term bonds.

However, permanent life insurance is rarely utilized as a financial planning tool by fee-only fiduciary advisors for the following reasons:

Since most fee-only RIAs aren’t willing to implement life insurance solutions, if clients see the value of life insurance as part of their financial plan they are forced to look for the solution outside of the confines of their fee-only fiduciary advisor. And this is where the problem starts.

Most permanent life insurance products are sold through life insurance agents who typically receive up to 100% of the first year premium as a commission and a small percent of any premiums clients pay in subsequent years. This is in stark contrast to fee-only fiduciary advisors who receive ~1% of the investment amount for each year that the client keeps their assets with them. So if you give $100,000 to a life insurance company, the agent that sold the policy will receive a $100,000 that first year and very little after that. If you give $100,000 to a fiduciary fee-only financial advisor, that individual will receive $1,000 up front and 1% annually for as long as the client chooses to stay invested with that financial advisor.

The incentives between these two parties are fundamentally different. The life insurance agent is incentivized to get the client to dump as much money in the first year as possible. In the second year that same life insurance agent is incentivized to get clients to dump more money into a new policy that generates a new 100% commission rate as opposed to an existing policy that would earn only a 1%-3% commission rate. There is no incentive for the insurance agent to manage an existing life insurance policy as opposed to trying and sell a new policy to that client even if keeping the older policy would be better for the client.

This is problematic because the life insurance company is selling an investment product with a long investment horizon that needs to be actively managed while incentivizing the sale of it through large short-term commissions. At some point in the long investment horizon of the permanent life insurance product, the client will need someone to help them manage the life insurance risk embedded in the policy. If they don’t, then this life insurance risk will eat up the returns of the policy and negate any tax-savings that the client had hoped to obtain from deciding to purchase the policy in the first place.

In the worst case, improper management of the insurance risk can force clients to cancel the policy at which point they will be hit with huge surrender charges (the insurance company has to make up for the large upfront commission it paid the agent in the first year somehow and this is typically the way they do it). These surrender charges can last for as long as 15-20 years. These large surrender charges can result in clients losing their entire investment. In fact, according to Society of Actuaries lapse studies, nearly 50% of purchasers of permanent life insurance will cancel their policy within the first 10 years—most of whom will be hit with this large surrender charge.

Policy owners that cancel the policy early like this will essentially receive a horrible return on investment and may not even get back their original capital. In such cases policy owners did not acquire a “tax-free long-term investment”, but instead will end up having spent a large amount of money paying for an extremely expensive term life insurance policy that they could have acquired for pennies on the dollar.

In order for policy owners to benefit from the “tax-free” investment benefits, they must both find a way to manage the insurance risk in order to keep the insurance expenses low AND keep the policy for life. In other words, policy owners need a fiduciary financial advisor to help them manage this risk as part of their life long financial and investment plan. But the fiduciary financial advisors aren’t incentivized to help clients do this and are essentially leaving these clients to fend for themselves as they search for help from life insurance agents who are excessively incentivized to sell these clients a bad product that maximizes the agent’s commission at the expense of the client.

Fee-only financial advisors that work with UHNW clients can implement these solutions and charge their fee on the assets in the same way they charge their fee on assets in a tax-advantaged retirement account. This is a win for both the client and their RIA. This will be covered in the article on no-commission annuities as well as the private placement life insurance (PPLI) article. However, for less wealthy clients, there is currently no way for fee-only advisors to get compensated for these solutions even if it is in the best interest of the client. The goal here is simply to demonstrate to the larger financial-advisory community how these products can provide better financial planning solutions than their current strategies with the hopes that by utilizing these strategies fee-only advisors can provide added value to their clients and differentiate themselves from their competitors.

As discussed previously, the concept of asset location is not a new one. The problem is that fiduciary financial advisors aren’t appreciating how they can fully utilize life insurance as a prime asset location tool. This is of increasing importance given that wealthy clients, i.e. the ideal clients for fiduciary financial advisors, are typically limited in their ability to contribute to tax-advantaged retirement plans but could contribute millions of dollars to tax-free life insurance plans.

The ultimate hope is that both the RIA community and life insurance companies will realize that a long-term product like permanent life insurance shouldn’t be sold through a channel that incentivizes short-term sales through large upfront commissions at the expense of the end consumer. Doing so provides no incentive for the distributor of the insurance product (i.e. the life insurance salesman) to provide necessary insurance management over the life of the policy. In fact, all the incentives are aligned for insurance salesman to sell the insurance product with the highest upfront commission—which not coincidentally tends to also have the highest expenses and are therefore worse for the client.

This is exactly why the words “life insurance” or “life insurance agent” invoke negative visceral reactions from the broader financial community. The life insurance salesman’s business model revolves around constantly finding new clients to sell high commission and high expense products to.

The commission-based life insurance salesman doesn’t have a long-term vested interest in the client—whereas an RIA who is charging an ongoing management fee does. The fee-only RIA’s business model revolves around continually trying to provide value to clients so they can continue to charge their fee every year.

This is exactly why life insurance should be utilized by fee-only RIAs as a tax-advantaged financial planning tool and not sold by highly commissioned agents. Furthermore, creating a fee-only RIA product that pays a small fee over the life of the product instead of a large one-time upfront commission is better for the end client. Life insurance products that pay large upfront commissions also have to have high expenses in the early years that drags down long-term returns for clients. A smaller commission over the life of the product would result in significantly lower insurance expenses in the product that would result in greater long-term returns for policyowners.

As we dive into how to utilize life insurance as a financial planning tool over the next few articles, I’m hopeful that the following will happen:

In this series we will discuss how the following life insurance solutions can provide greater after-tax returns for the fixed income portion of a client’s portfolio simply by using life insurance as an investment vehicle to protect the client from interest rate risk and high taxation on the gains:

Life insurance solutions can create greater after-tax fixed income returns by protecting clients from interest rate risk and taxation

| Strategy | Fixed Income Solution | Retirement Account Similarity | Expected Rate of Return | Minimum Holding Period |

|---|---|---|---|---|

| No-Commission Fixed/Indexed Annuities | Tax-deferred long-term bonds without interest rate risk | Traditional IRA | 2%-4% | 5-7 years+ |

| Whole Life Insurance | Tax-free long-term bonds without interest rate risk and with equity dividends | Roth IRA | 4%-4.5% (tax-free) | 15-20 years+ |

| Indexed Universal Life Insurance | Tax-free equity returns with cap and floor | Roth IRA | 4.5%-5.5% (tax-free) | 20 years+ |

| Private Placement Life Insurance | Investing in high earning assets that would otherwise be tax-inefficient in place of fixed income | Roth IRA | 7%+ (tax-free) | 10+ years |

| Life Settlements | Uncorrelated alternative asset in place of long-term bonds | None/Roth IRA with PPLI | 8%-11% (taxable) 8%-11%(tax-free with PPLI) | ~10 years |

Author

Learn how to evaluate PPLI carriers by balancing financial strength ratings against investment platform flexibility. Compare fee structures and long-term costs to select the optimal Private Placement Life Insurance carrier for your wealth strategy.

Determining the right death benefit level for your Private Placement Life Insurance (PPLI) policy is one of the most critical decisions that will impact your policy’s performance, costs, and overall effectiveness. This comprehensive guide explores how to balance regulatory requirements, estate planning needs, family protection goals, and investment capacity optimization to find the optimal death benefit level for your unique circumstances.

Master essential best practices for PPLI investment committee governance. Learn to establish effective oversight structures, develop robust policies, and implement risk management frameworks that maximize wealth preservation while ensuring regulatory compliance.

0 Comments