How to Structure Permanent Life Insurance to Surpass Buy Term & Invest

Rajiv Rebello

Author

August 29, 2017

Author

Buy term and invest the difference is your best bet when it comes to life insurance—unless you find the right product and fund it properly. For high net worth investors who already invest in U.S. Treasuries as part of their bond portfolio, properly structuring certain permanent life insurance products can yield higher returns with a similar underlying risk.

In the absence of finding a low commission product and funding it properly, buy term and invest the difference is almost universally the way to go. Why is this? Because the high commissions paid to agents for most life insurance products result in low accumulation and surrender values when the policy owner cancels the policy (And 50% of these policy owners will cancel it within 10 years)

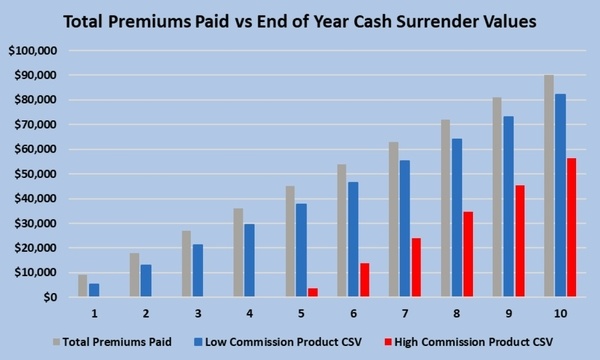

In our previous post post (see here) we noted how paying the same premium into a low commission product vs a high commission product resulted in significantly more cash accumulation and cash surrender value in the low commission product. This makes intuitive sense. The less money the company has to pay to the agent, the more it can afford to give to the policy owner.

However, you may have also noted that while the cash surrender value (CSV) for the low commission product is notably higher than the high commission one, it’s still lower than the total premiums paid into the product through that year.

In the graph above, the high commission product costs substantially more than the 10 year term product. We can see that after 10 years the high commission product would cost the client $33,757 whereas the term would only cost $5,200. This is $28,557 more in premiums being paid for the same result. The low commission product, on the other hand, is only $2,631 more expensive than the term policy after 10 years.

Tens of millions of dollars are lost every year by policy owners who purchase mainly expensive high commission permanent products and then cancel them within 10 years. In fact, 50% of all owners of permanent life insurance policy owners do this.

Clearly the low commission product is significantly better than the high commission product. But it’s still not as valuable as the term product—at least not using the level premium strategy shown above. But if we were to fund the low commission product differently, could we achieve better results than just buying term?

A permanent life insurance product combines insurance costs and investment returns. By minimizing the amount of insurance costs, the policy owner can maximize the investment return on the product.

When a policy owner of a permanent policy dies, the policy owner gets paid a death benefit amount from the life insurance company. However, in exchange the life insurance company gets to keep any cash value in the policy. This reduces the risk for the life insurance company since they get something back for paying out the death benefit amount.

So for example, if a policy owner has a $1M policy and $600,000 in cash value in the policy, then if the insured on the policy dies the life insurance company has to pay him/her the $1M death benefit. However, the insurance company gets to keep the $600,000 in cash value for themselves. This means that the net amount of risk (NAR) for the life insurance company is only $400,000 ($1,000,000 – $600,000) since they are only losing a net of $400,000 upon death of the insured. The company bases its charges for the policy for the current year based on this Net Amount at Risk Amount. The lower the NAR for the life insurance company, then the lower amount of charges are deducted from the policy which allows for better accumulation for the policy owner.

Scenario 1: A policy owner with a $1M policy has $600,000 in cash value. This creates an NAR of $400,000 ($1,000,000 -$600,000).

Scenario 2: The same policy owner has a $1M policy but with only $100,000 in cash value. This creates an NAR of $900,000 ($1,000,000 – $100,000).

Assume that the life insurance company charges 1% of the NAR as a charge for agreeing to pay the death benefit on each of these policies. Well, in scenario 1 that charge is only $4,000 (1% x $400,000) while in scenario 2 that charge is $9,000 (1% x $900,000). In other words, scenario 1 results in $5,000 more in charges being saved on the policy. That is an extra $5,000 that also gets credited with interest every year.

So the policy with the low NAR allows the policy owner to both save in charges and get extra interest credited to the policy every year. This effect compounds year after year in such a way that the investor can realize returns in excess of the underlying investment risk associated with the investment if he/she finds the right product and funds it properly.

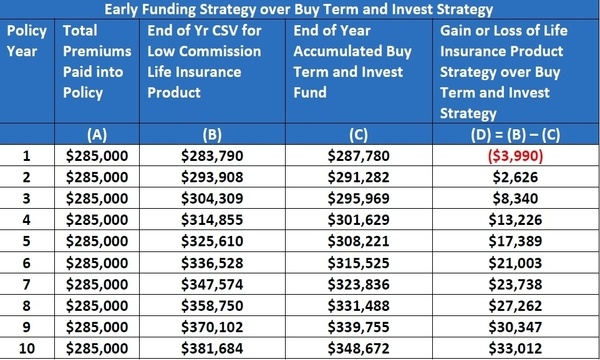

Let’s redo our buy term and invest the difference comparison except by using an asset based strategy for the low commission product. Instead of paying a level premium as in the above example, we’re going to do a single premium dump-in in year 1 of $285,000. The purpose of this large single premium is to decrease the NAR as illustrated above which will reduce the charges and allow for better accumulation and returns for the policy owner.

In order to do an apples-to-apples comparison we’ll compare this early funding strategy using a low commission life insurance product with a buy term and invest the difference strategy in U.S. Treasuries.

Why use the U.S. Treasury Yield-Curve? Well, because that’s what the life insurance product we’ll be comparing invests in with the premium dollars sent to it. If it was an Indexed Universal Life product that was investing in a S&P index, we’d use projections based on expected returns of that index. Of course those returns would also carry significantly more risk than investments in Treasuries.

Whenever you do an investment comparison it’s important to use a benchmark with a similar risk profile. It would be an inequitable comparison to project returns in an equity fund that has high expected returns but also high volatility with a projection invested in bonds that have low expected returns but also low volatility.

Keep in mind that while life insurance carriers are heavily invested in Treasuries, most of the 30 year Treasuries they are invested in are from years ago when interest rates were much higher. So while a 30 year Treasury bond offers coupons at less than 3% today, 20 years ago these coupons were around 7%. Same underlying risk, but different maturity horizon.

As of 6/20/2017 the 10-year Treasury yield rate is 2.21%. The 10-year Treasury yield curve is the following:

US Treasury Yield Curve as of 6/20/2017

This yield curve will form the basis for the “buy term and invest” comparison that we’ll be making below.

Early Funding Strategy vs Buy Term and Invest Strategy:

In the above table $285,000 is paid into a low commission life insurance policy on day 1 with no future premiums paid into the policy. The End of Year Cash Surrender Values are shown in Column B. This is directly comparable to our Buy Term and Invest Strategy End of Year Values in Column C. The values in Column C are determined by investing the $285,000 into U.S. treasuries at the yields shown in the previous table and paying $520/year for a $1M Term policy.

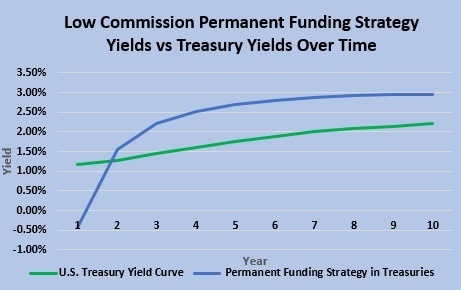

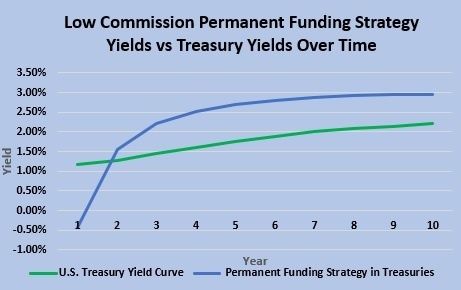

For those who like to compare yields and rates of return, below are the rates of return for our asset-based Permanent Product Funding Strategy in Treasuries vs the Buy Term and Invest in Treasuries Strategy:

Permanent Funding Strategy in Treasuries vs Buy Term and Invest in Treasuries:

With the exception of the first year, the permanent funding strategy results in yields significantly above that of U.S. treasuries. After 4 years the permanent funding strategy has earned 2.52% which is already 0.91% above the treasury curve.

A significant portion of any high net-worth individual’s portfolio will always be in bond-type vehicles. For these investors, gaming some of these permanent life insurance products with low commissions and high liquidity is a great way to take bond-level risk while achieving above bond-level returns. As an added bonus, these investors can get both short and long-term life insurance coverage to cover some of the excess liabilities their estates might have upon death.

Author

Discover how Private Placement Life Insurance transforms charitable remainder trust strategies into powerful wealth replacement tools. Learn tax-efficient approaches that maximize charitable benefits while preserving family wealth for high-net-worth families.

This blog post explores essential PPLI due diligence steps, covering carrier evaluation, regulatory considerations, investment platforms, tax compliance, and advisor expertise to help high-net-worth individuals make informed decisions before implementing this specialized insurance solution.

Discover how PPLI enhances business succession planning through key person insurance and buy-sell funding. Learn private placement life insurance strategies for business owners.

0 Comments