How to Get a Depreciation Deduction-and Not Have to Pay it Back

Rajiv Rebello

Author

July 04, 2023

Author

Depreciation allows real estate investors to get a tax deduction every year. The downside with it is that they have to pay back the deductions they took when they sell the property—unless they utilize step-up in basis provisions.

Real estate has a number of tax advantages embedded in it. The most obvious one is depreciation. By taking a depreciation deduction you can get a tax write off every year that will most likely offset the rental income you receive. A downside with the depreciation deduction is that when you sell the property all the depreciation deductions you took are added back to the tax-liability.

Let’s take a look at an actual example:

Example 1:

John and Mary are both 35 years old and have recently bought a new house in the town adjacent to their old house in California. They bought their old house for $700,000 and it is now worth $1,000,000. They plan on renting out this old house as a long-term rental property. Let’s assume the net annual rental income for this house $50,000/year. Both the house appreciation and rent appreciation on the house are expected to increase by 3% per year. They plan on selling the old house in 28 years when they retire. Collectively John and Mary make $400,000/year which puts them in a 41.3% total marginal income tax bracket for ordinary income taxation. Any net income they receive from the rental property is invested for the long-term in a low cost S&P500 Index Fund.

When we look at analyzing rental investments, it’s important to look at net income on an after-tax basis. This is particularly important in states like California that charge high state income tax rates on both ordinary income and capital gains income—which is why John and Mary’s marginal tax rates are so high.

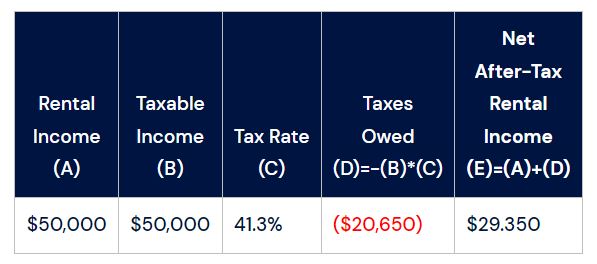

So while they are making $50,000 per year before taxes, when we account for the 41.3% tax-rate, this ends up being only $29,650 after taxes.

Table 1: Calculating After-Tax Rental Income

Without any deductions to reduce the rental income (Column A), the full $50,000 is considered taxable income. |

Depreciation is a tax deduction that helps reduce the tax liability here. Depreciation accounts for wear and tear on a physical property that occurs over time and reduces the value of the property. For example, over time a building will wear down and repairs will need to be made. In the absence of these repairs, the value of the building will decrease. All else being equal a brand new building is worth more than an older building of the same size in the same location.

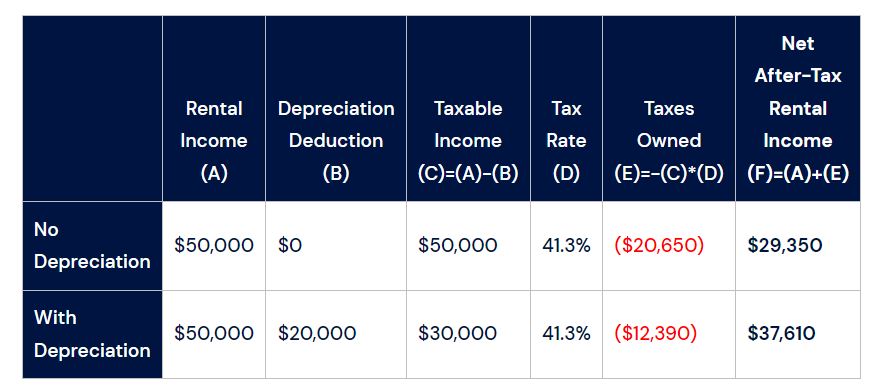

Depreciation allows you to deduct the decrease in the value of the property over time. Only the value of the property can be depreciated and not the value of the land. While there are many ways to utilize depreciation, to simplify this example we’ll be using straight line depreciation where you depreciate the property by a set amount for a number of years. For the sake of this example, we’ll be depreciating the property by $20,000 a year for 28 years.

To understand why this is valuable, we need to go back to our rental example. Without depreciation the client receives $50,000 in rental income and pays taxes on this full amount and is left with $29,650. However, depreciation reduces the amount that is taxable. The client still receives the full $50,000 on income but only pays taxes on the value of the rental income minus the depreciation deduction. In this case the taxable income is only $30,000 since the $20,000 depreciation deduction reduces the $50,000 tax liability to a $30,000 tax liability. Due to this reduction in the tax-liability, John and Mary are able to keep $37,610 after taxes due to depreciation as opposed to $29,650 without depreciation.

Table 2: Depreciation Reduces Taxable Rental Income

Depreciation is a deduction that reduces the taxable income and allows for the investor to keep more of the rental income on an after tax basis. |

However, there is a catch here. And the catch is that while depreciation reduces the tax-liability of the rental income in the years that the investors are receiving rent, it increases the tax-liability when the investor sells the property. This is known as depreciation recapture.

Let’s look at how this works in the above example.

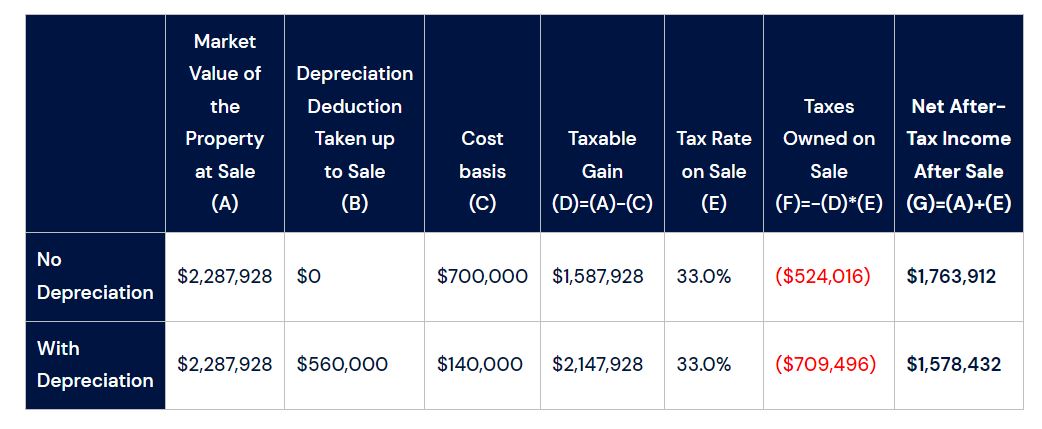

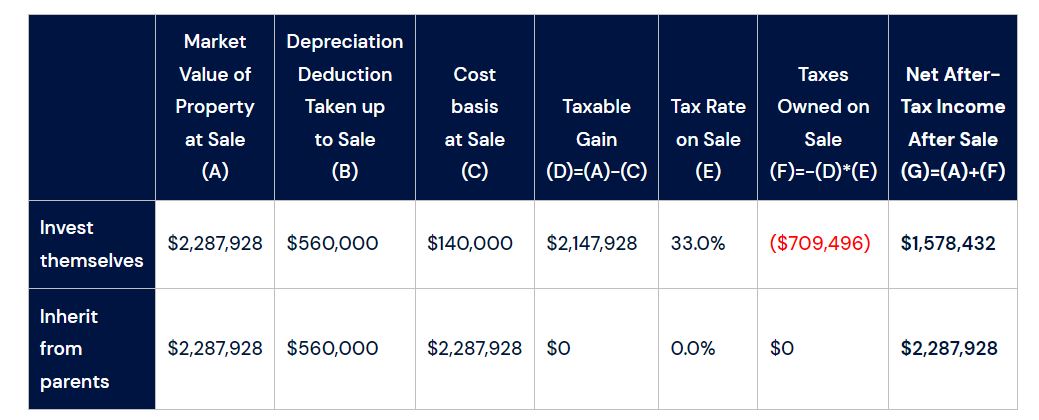

Let’s assume that John and Mary decide to sell the property after 28 years. Let’s assume that the value of the property after 28 years is $2,287,928. As mentioned above, the cost basis here is $700,000. The difference between the cost basis and the value of the property is the taxable gain. So in the absence of depreciation the taxable gain here is $1,587,928 ($2,287,928 – $700,000 = $1,587,928).

However, depreciation reduces the cost basis of the property by the amount the property has been depreciated. Depreciating the property by $20,000 a year for 28 years is a total of $560,000 in depreciation deductions. Which means the cost basis is reduced by $560,000. So instead of a $700,000 cost basis, the cost basis is now $140,000. This means that the taxable gain is increased to $2,147,928 ($2,287,928 – $140,000 = $2,147,928). This of course increases the taxes owed on the sale, and decreases, the net after-tax proceeds available to John and Mary after the sale. It’s especially punitive for John and Mary because they live in California where all of the capital gains are subject to state income tax.

Table 3: Depreciation Increases Capital Gains Taxes on Sale of Property

Depreciation reduces the cost basis of the property (Column C) from $700,000 to $140,000. This increases the taxable gain (Column D) and the taxes owed on the sale (Column F). |

As shown in the table above, depreciation reduces the cost basis of the property (Column C) which increases the taxable gain (Column D) and the taxes owed on the sale (Column F) which reduces the after-tax sale income available to John and Mary (Column G) if depreciation wasn’t used.

So to summarize, depreciation helps you reduce taxes when you are renting the property, but increases taxes when you sell the property.

It’s worth noting that the depreciation recapture at sale is mandatory even if you didn’t take the depreciation deduction. So in the above example, when John and Mary sell the property they will pay taxes on the $560,000 that they could have depreciated even if they forgot to take the depreciation deduction all along. As such, if you’re investing in real estate it’s important to make sure that your accountant is taking this deduction every year. Otherwise when you sell the property your tax liability will be increased even though you didn’t get any benefit from depreciation.

While depreciation has clear benefits when it comes to receiving rental income, it also has a significant drawback when the client sells the property. However, this drawback can be eliminated by using upstream gifting strategies that we described in a previous article here.

Utilizing upstream gifting strategies to eliminate depreciation recapture liabilities

As we mentioned in a previous article, a key benefit of inheriting assets is that you get a step-up in basis of the assets. This means that the generation that inherits it can sell those assets immediately without paying taxes on all the gains up until that point. An added benefit with this is that it eliminates the depreciation recapture element—even if the previous generation used up all the depreciation deductions.

Furthermore, it allows the next generation to start using depreciation deductions again based on the new stepped-up basis—even though the previous generation used up all of it.

Let’s look at how this works in practice by modifying Example 1 by assuming that John and Mary gift the property to John’s parents so that they can inherit it when John’s parents die and benefit from these provisions.

Example 2:

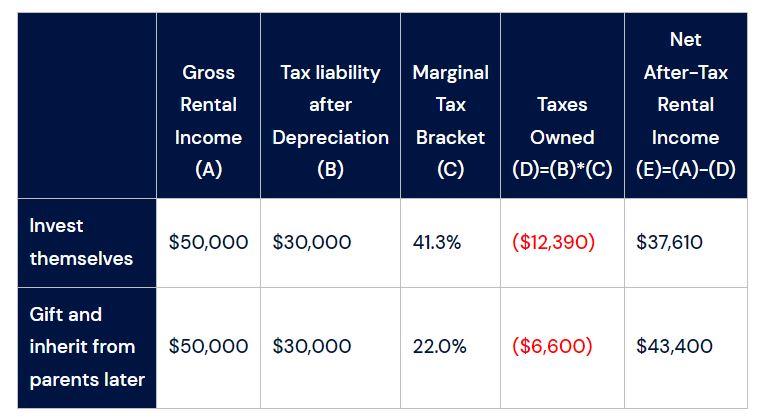

Instead of John and Mary renting out their old house, they decide to gift the property to John’s parents so that they can inherit it when John’s parents pass away and benefit from step-up in basis. This gifting to John’s parents has an added benefit of reducing the tax liability on the rental income since John’s parents are retired in Florida (which has no state income tax) and are at a much lower tax bracket since their income is less in retirement. While John and Mary are at a total 41.3% marginal ordinary income tax bracket in California, John’s parents are only at a 22% total ordinary income bracket in Florida.

First, let’s look at the impact on after-tax income. As we saw above, due to John and Mary’s high tax rate, of the $50,000 in rental income they only get to keep $37,610 after taxes are paid. John’s parents on the other hand get to keep significantly more as shown in the table below.

Table 4: Rental Income Comparison of Investing Directly vs Inheriting

Since John’s parents are in a much lower bracket than John and Mary, by gifting the property to John’s parents, the taxes owed on the rental property is decreased. As a result, the after-tax rental income increases from $37,610 to $43,400. |

As the above table shows, since John’s parents are in a much lower tax bracket gifting them the property results in John’s parents keeping 15% more of the rental income on an after-tax basis than if John and Mary kept the property in their name ($43,400 vs $37,610). This is more income that can be invested in their long-term S&P500 index fund.

Furthermore, when John’s parents pass away, the cost basis of the property is stepped-up to the market value of the property. So John and Mary can sell the property at the time without paying any taxes on the gains. The table below shows the impact of this if John and Mary sell the property after 28 years versus inheriting it in 28 years after John’s parents pass away.

Table 5: After-Tax Sale Comparison of Property from Investing Directly vs Inheriting

Typically when a rental property is sold, the cost basis of the property is reduced by the amount of the depreciation deductions taken. If John and Mary invest directly into the property then their original cost basis of $700,000 is reduced by the $560,000 total depreciation deductions to $140,000. This results in a larger taxable gain.However, if John’s parents invest and take $560,000 in depreciation deductions the cost basis is not reduced. Instead the cost basis is increased to the market value of the property so that there is no taxable gain. |

In the above example we can see that the market value (Column A) and total depreciation deductions (Column B) are the same whether John and Mary invest in the property or whether John’s parents invest in the property.

However, the key difference is the effect on the cost basis (Column C). If John and Mary invest directly in the property then their original cost basis of $700,000 is reduced by the $560,000 depreciation deductions to $140,000. This results in a large taxable gain (Column D) when they sell the property.

However, if John and Mary inherit the property from John’s parents then there is no reduction to the cost basis due to the depreciation deductions. Instead the cost basis is stepped up to the market value of the property at the time of the sale. This means that John and Mary can sell the property after they inherit it without paying any taxes on the gains—even though John’s parents benefited from the full $560,000 depreciation deductions over the past 28 years.

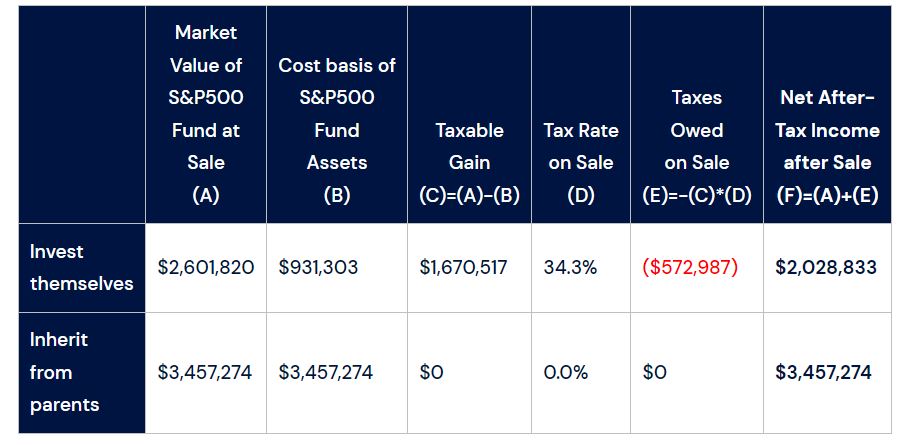

The value of step-up in basis also has a benefit on the after-tax value of the investment assets that John and Mary will have from the rental income. Remember that the rental income that was received from the property was used to in a low-cost index fund. All of this value will be inherited tax-free as well as shown in the table below.

Table 6: After-Tax Sale Comparison of S&P500 Fund Assets from Investing Directly vs Inheriting

Since John’s parents are able to keep more of the rental income due to their lower tax bracket, they are able to invest more which grows to $3,457,274 as opposed to $2,601,820 if John and Mary invest directly. Furthermore, due to step-up in basis, there is no taxable gain if John and Mary inherit the assets and then sell versus if they invest themselves and then sell. |

In the above table the first thing we should notice is that the total market value of the S&P500 Fund (Column A) that John and Mary are able to accumulate after 28 years is significantly less than what John’s parents could accumulate. This is due to the fact that John and Mary have to pay more taxes on the rental income from the property each year and therefore accumulate less wealth with the rental income than John’s parents could.

The next thing that should be noticed is that if John and Mary invest the rental property income directly into an S&P500 fund then there is a large taxable gain (Column C) whereas there is no taxable gain if John’s parents invest the money and John and Mary inherit the assets. This is due to the fact that if John and Mary inherit the assets the cost basis of the assets (Column B) is stepped up to the market value of the assets so that there is no taxable gain (Column C). However, if John and Mary simply invest directly into an S&P500 fund and sell after 28 years then there will be a large taxable gain.

As the table below shows, the total after-tax wealth created by John and Mary inheriting the property and S&P500 fund from John’s parents and then selling all the assets is 59% higher than if John and Mary simply invest in the property themselves and sell after 28 years.

Table 7: Total Value and Returns from Investing Directly vs Inheriting from Parents

By gifting the property to John’s parents and then inheriting all the assets after they pass away, John and Mary are able to increase their wealth by more than $2.1 million (a 59% increase) as opposed to if they were to simply keep the property themselves and sell after 28 years. |

Increased depreciation deduction due to step-up in basis

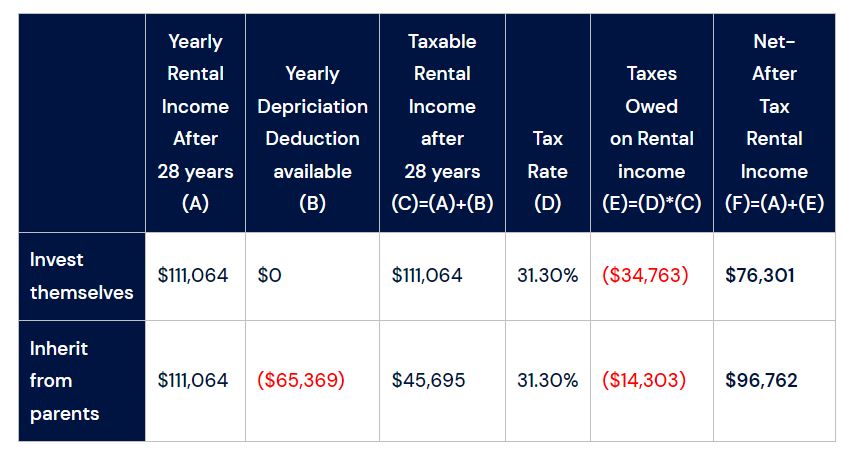

Another large benefit from inheriting rental property versus investing directly in them is that it allows for the depreciation deduction to be reset since the cost basis was stepped up. In Example 1 we saw that the original cost basis was $700,000 and the maximum depreciation of $20,000 a year for 28 years is based on this original cost. After 28 years, no further depreciation can be taken. This means that John and Mary decide to keep the rental property after 28 years they will have a large rental income without any means to offset that income with a depreciation deduction.

However, if John and Mary inherit the property then cost basis is automatically stepped up to the current market value and John and Mary can utilize a depreciation deduction based on this new stepped up cost basis. In the table below we see the difference in after-tax rental income if John and Mary decide to keep the property after 28 years after investing in it themselves or inheriting it from John’s parents.

Table 8: Step-Up in Basis Increases Depreciation Deduction Available

While the rental income is the same in both cases after 28 years, the depreciation deduction is only available if John and Mary inherit the assets. By inheriting the assets and benefitting from the increased depreciation deduction that comes with the new stepped-up basis in the property, John and Mary get to keep more than $20,000 more in rental income on after-tax basis. |

In the above table we can see that the yearly rental income after 28 years (Column A) is the same whether John and Mary invested in the property themselves or inherited it. However, the key difference is the depreciation deduction available. If John and Mary invest in the property directly, then after 28 years they’ve already used up all the depreciation deductions available to them (Column C) and can’t offset their rental income.

However, if John and Mary inherit the property then they get a new depreciation deduction available to them based on the new stepped-up basis of the property. As we can see from Column F, John and Mary will receive more than $20,000 more in after-tax rental income ($96,762 vs $76,301) if they inherit the property versus invest directly.

When John and Mary’s kids inherit the property after John and Mary pass away, they will be able to get a new stepped up basis and new depreciation deduction available to them and repeat the process over again. Utilizing depreciation deductions in combination with a step-up in basis can be a great way to invest in real estate and maximize the wealth passed on to the next generation by minimizing the taxation on the gains.

Author

Learn how to evaluate PPLI carriers by balancing financial strength ratings against investment platform flexibility. Compare fee structures and long-term costs to select the optimal Private Placement Life Insurance carrier for your wealth strategy.

Determining the right death benefit level for your Private Placement Life Insurance (PPLI) policy is one of the most critical decisions that will impact your policy’s performance, costs, and overall effectiveness. This comprehensive guide explores how to balance regulatory requirements, estate planning needs, family protection goals, and investment capacity optimization to find the optimal death benefit level for your unique circumstances.

Master essential best practices for PPLI investment committee governance. Learn to establish effective oversight structures, develop robust policies, and implement risk management frameworks that maximize wealth preservation while ensuring regulatory compliance.

0 Comments