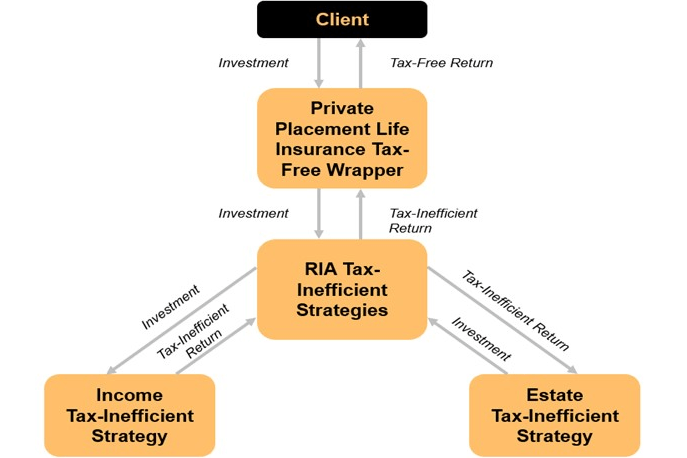

RIAs can utilize PPLI to shelter otherwise tax-inefficient assets from income and estate taxation.

RIAs can utilize PPLI to shelter otherwise tax-inefficient assets from income and estate taxation.

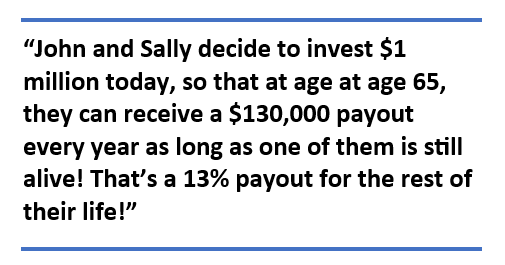

With interest rates near 20 year highs, wouldn’t it be great if you could lock-in these high rates for the rest of your life? Luckily for you, there is a way to do that and that’s through purchasing a guaranteed lifetime income product. By locking in rates today, you...

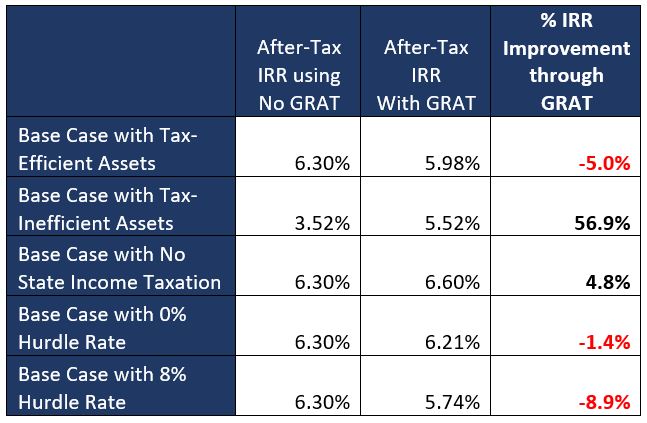

Protecting the client from an estate tax liability only to expose them to a larger tax-drag and income tax liability, can pose more harm than good.

The best way to maximize the value of a GRAT is to utilize the GRAT for assets that are tax-inefficient. This holistic estate and investment approach can be improved further by utilizing the GRAT as a vehicle to invest in private placement life insurance (PPLI) which allows the assets to compound without the tax drag. Doing so essentially turns the tax-inefficient assets into tax-efficient assets by providing the client with the benefits of tax-free growth as well as step-up in basis that would be lost if the client only used the GRAT by itself.

In order for fee-only advisors to truly be fiduciaries they need to utilize life insurance products that are in the best interests of the clients.

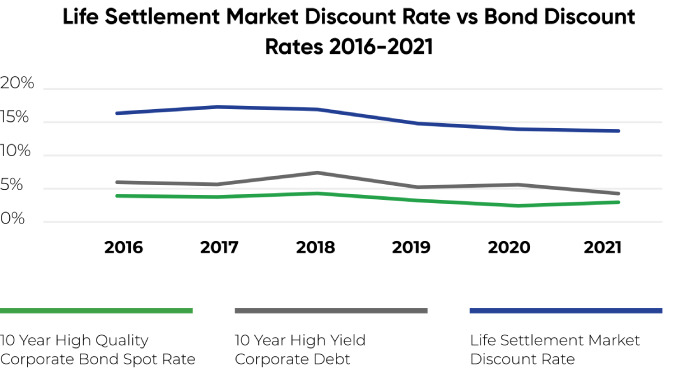

Investing in uncorrelated assets like life settlements can provide greater portfolio diversification and returns than using low-yielding bonds in a rising interest rate environment.

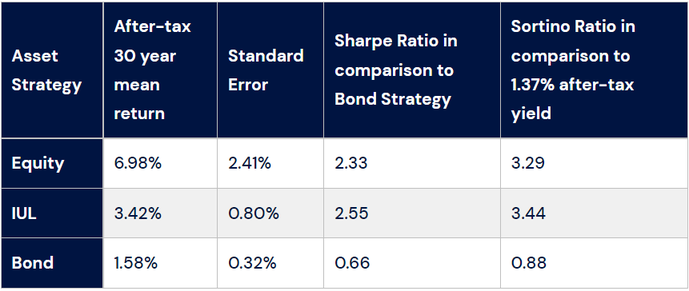

How IUL policies allow portfolios to increase after-tax returns through increasing the equity allocation of the portfolio while minimizing volatility.

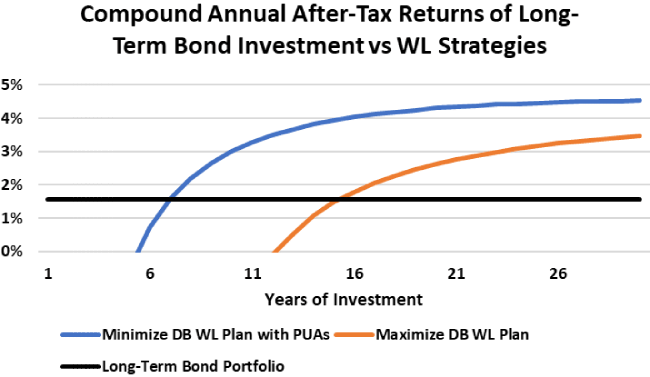

Investing in tax-free long-term bonds with equity dividends and no interest rate risk through whole life insurance.

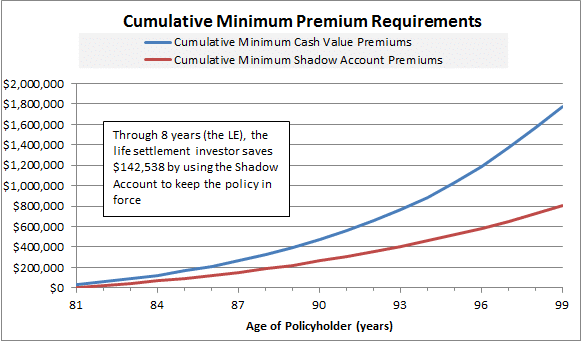

One of the main concerns of life settlement investors is minimizing the premiums required to keep the policy in force. Colva is a specialist in utilizing actuarial principles to determine the minimum premium to keep a policy in force. Current industry practice...

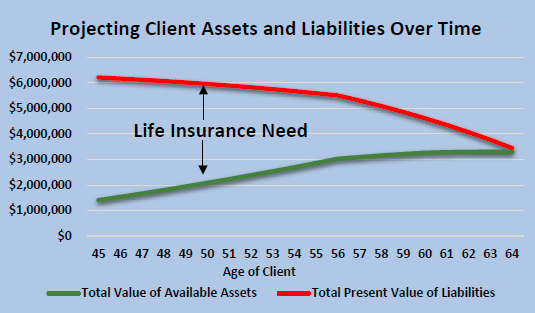

The goal of any comprehensive financial advisor is to help protect the financial situation of their clients and their families as the client ages. The financial advisor wants to ensure that when the client retires the client and their families are fully taken care of....

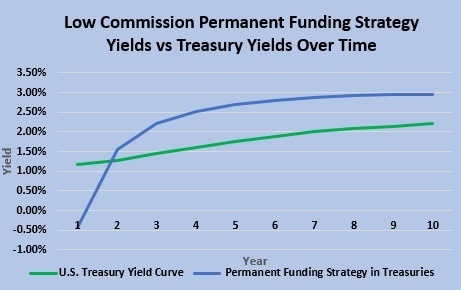

Buy term and invest the difference is your best bet when it comes to life insurance—unless you find the right product and fund it properly. For high net worth investors who already invest in U.S. Treasuries as part of their bond portfolio, properly structuring certain...

As an actuary who helped to price and analyze policies for a large life insurance carrier, I quickly saw how policy owners end up getting the worst end of the deal. While agents can earn 80% to 100% of the first year premium that policy owners pay for a permanent life...