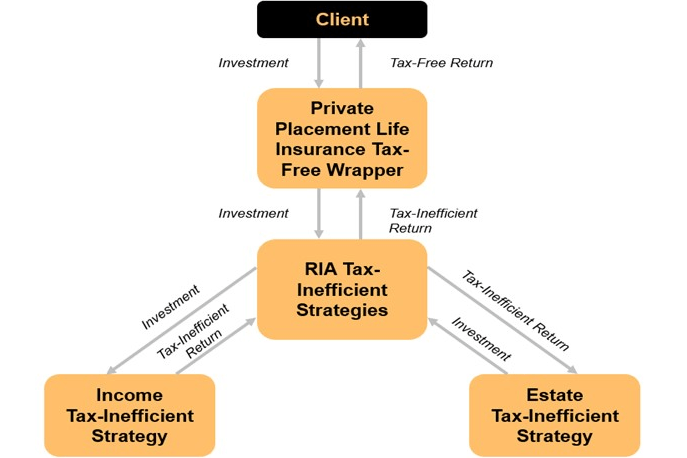

RIAs can utilize PPLI to shelter otherwise tax-inefficient assets from income and estate taxation.

RIAs can utilize PPLI to shelter otherwise tax-inefficient assets from income and estate taxation.

Protecting the client from an estate tax liability only to expose them to a larger tax-drag and income tax liability, can pose more harm than good.

Depreciation allows real estate investors to get a tax deduction every year. The downside with it is that they have to pay back the deductions they took when they sell the property—unless they utilize step-up in basis provisions.

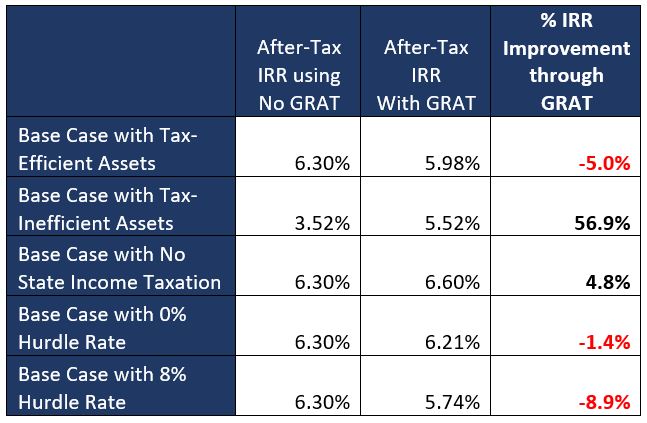

The best way to maximize the value of a GRAT is to utilize the GRAT for assets that are tax-inefficient. This holistic estate and investment approach can be improved further by utilizing the GRAT as a vehicle to invest in private placement life insurance (PPLI) which allows the assets to compound without the tax drag. Doing so essentially turns the tax-inefficient assets into tax-efficient assets by providing the client with the benefits of tax-free growth as well as step-up in basis that would be lost if the client only used the GRAT by itself.

By using gifting strategies in place of contributing to a Roth IRA, high net worth clients can essentially replicate the benefits of a Roth IRA with larger contribution amounts and earlier withdrawal privileges.